Osaka Gas Co., Ltd. is Japan’s second-largest city-gas utility, the Kansai-region counterpart to Tokyo Gas, and the most internationally vertically integrated of the country’s three big gas houses. In 2020 it bought Sabine Oil & Gas, a Houston-based independent producer with acreage across the East Texas and North Louisiana shale plays, for roughly six hundred and ten million dollars — a deal that took Osaka Gas from being a customer of US LNG to being an upstream owner of the molecules. It also co-owns a stake in the Freeport LNG export terminal on the Texas Gulf Coast alongside JERA and Sempra Infrastructure, takes offtake from Cameron LNG in Louisiana, and runs one of the most diversified non-gas portfolios of any Japanese utility through Osaka Gas Chemicals. For energy buyers, LNG traders, and industrial materials customers, Osaka Gas is increasingly a counterparty whose business lives well beyond the pipes under Osaka.

From Meiji-era city gas to a vertically integrated energy group

Osaka Gas was founded in April 1897, two decades after Tokyo Gas, as a private company chartered to supply manufactured gas — initially produced from coal — to lighting and industrial customers across the rapidly industrialising city of Osaka. Through the twentieth century it grew along the same trajectory as its Tokyo counterpart: city-scale infrastructure laid through prefectural capitals, conversion to natural gas as the country pivoted in the 1970s, and the construction of LNG receiving terminals as Japan became the world’s largest LNG importer following the 1973 oil shock.

The company’s Senboku LNG receiving terminal in Sakai, on the southern edge of Osaka Bay, came online in stages from 1972 and remains one of the largest receiving facilities in Japan. The Himeji LNG terminal in Hyogo Prefecture was added later. Together those complexes anchor the utility’s import position and feed roughly seven million customer accounts across the Kansai region — Osaka, Hyogo, Kyoto, and parts of Shiga, Wakayama, and Nara. Headquarters sit in the Chuo ward of Osaka, the company is listed on the Tokyo Stock Exchange under ticker 9532, and consolidated employment runs to approximately twenty-one thousand. Masayuki Sahara took over as president in 2024, succeeding Takehiro Honjo.

The Kansai franchise, and what it means structurally

City-gas in Japan is a regional business. Each of the three big city-gas utilities — Tokyo Gas, Osaka Gas, and the smaller Toho Gas based in Nagoya — operates a near-monopoly distribution network within its franchise region, regulated by the Ministry of Economy, Trade and Industry. Pipelines are not contestable infrastructure in any meaningful sense; nobody is going to lay a competing gas grid under Osaka. The regulated rate base and the structural demand from industrial, commercial, and residential customers give each utility a stable annuity inside its home region. What differs is what each utility does with that annuity. Tokyo Gas, the larger by gas volume and the more financially conservative, has historically reinvested in domestic gas-system expansion, electricity retail post-deregulation, and selective overseas LNG offtake. Osaka Gas has been the more aggressive international diversifier — taking equity positions in US shale upstream, co-owning LNG liquefaction trains in the Gulf of Mexico, and building out a specialty-chemicals business that now operates more like an industrial-materials company than a utility subsidiary.

| Dimension | Tokyo Gas (9531) | Osaka Gas (9532) | Toho Gas (9533) |

|---|---|---|---|

| Founded | 1885 | 1897 | 1922 |

| Franchise region | Greater Tokyo / Kanto | Kansai (Osaka / Hyogo / Kyoto) | Chubu (Nagoya / Aichi) |

| Customers (approx.) | ~12 million | ~7 million | ~2.6 million |

| Main LNG terminals | Negishi, Sodegaura, Ohgishima | Senboku I/II, Himeji LNG | Yokkaichi (with partners) |

| US upstream ownership | Selective shale stakes (Barnett, Eagle Ford) | Sabine Oil & Gas (full ownership, 2020) | Limited |

| US LNG export equity | Cove Point (offtake), other | Freeport LNG, Cameron LNG (offtake/equity) | Freeport (smaller share) |

| Specialty-materials subsidiary | Modest | Osaka Gas Chemicals (significant) | Modest |

| Electricity retail (post-2016) | Tokyo Gas Electricity | Osaka Gas Electricity | Toho Gas Electricity |

The summary line is that Osaka Gas runs the smaller franchise but the more international and more industrially diversified business. Where Tokyo Gas looks like a regulated utility with overseas hedges, Osaka Gas increasingly looks like an integrated energy and materials group with a Kansai utility at its core.

Sabine Oil & Gas, and why a Japanese utility bought a Texas driller

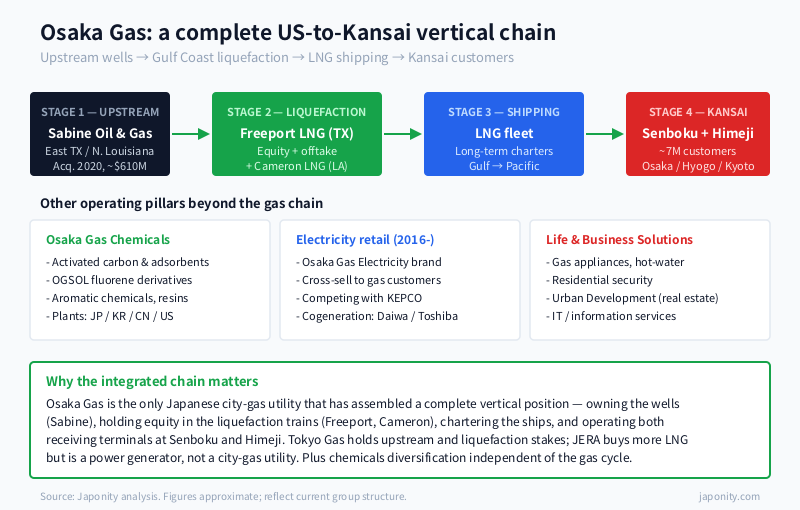

The Sabine deal in 2020 was unusual. Japanese utilities had taken minority equity in US shale plays before — Tokyo Gas in the Barnett Shale, Osaka Gas itself in earlier Eagle Ford investments, JERA in various positions — but those were almost always non-operated working interests structured to provide commodity exposure without operational control. The Sabine acquisition was different. Osaka Gas took the entire company, including its operating organisation, its acreage in the Cotton Valley and Haynesville shale formations across East Texas and North Louisiana, and its existing production base. The price was approximately six hundred and ten million dollars.

The strategic logic was vertical integration. By owning upstream production directly, Osaka Gas could feed its US LNG offtake — particularly from Freeport LNG, where it has equity in Train 1 alongside JERA and others — with molecules from its own wells, capturing the producer margin as well as the liquefaction and shipping margin. In a world where US LNG had become the swing supplier to Asia and where spot LNG prices spiked dramatically through 2021-2022, owning the upstream piece moved Osaka Gas closer to a fully integrated commodity position than any other Japanese city-gas utility. Sabine operates as a wholly owned US subsidiary and has continued to develop its Cotton Valley and Haynesville positions. The Haynesville exposure in particular matters: it is one of the lowest-cost dry-gas plays in North America and sits within reasonable pipeline distance of the Gulf Coast LNG export complex.

Freeport LNG and the Gulf Coast equity stack

Osaka Gas’s position in Freeport LNG, the Quintana Island, Texas liquefaction and export terminal majority-owned by Freeport LNG Holdings with Sempra Infrastructure as a major equity partner, is the centrepiece of its US LNG strategy. Freeport’s three liquefaction trains came online sequentially through 2019-2020 with combined nameplate capacity of approximately fifteen million tonnes per year. JERA, Osaka Gas, and other Japanese and global counterparties hold equity and offtake positions across the trains, structuring the project as a multi-buyer toll-style facility rather than a single-owner project. Offtake from Freeport, supplemented by additional offtake from Cameron LNG in Hackberry, Louisiana — a Sempra-led project where Osaka Gas is a foundational customer alongside Mitsui and Mitsubishi — gives the utility a US Gulf Coast supply base of roughly two million tonnes per year of contracted LNG.

With Sabine Oil & Gas providing upstream feedstock at the wellhead, the vertical chain is now: Sabine wells in East Texas / North Louisiana, through US pipeline transport, into Freeport and Cameron liquefaction, onto LNG shipping under long-term charter, into Senboku and Himeji regasification, and out into the Kansai customer base. That is a complete integrated chain, and very few utilities anywhere in the world own all the links. Among Japanese utilities, only Osaka Gas has assembled it in its current form. Tokyo Gas owns equity in upstream and in liquefaction but has not made a Sabine-style full-ownership upstream acquisition. JERA, the joint power-generation utility owned by TEPCO and Chubu Electric, is the larger LNG buyer globally but is a power generator rather than a city-gas utility, with a different downstream profile.

Osaka Gas Chemicals: the part of the company that doesn’t sell gas

Osaka Gas Chemicals Co., Ltd. is the group’s specialty-chemicals and materials subsidiary, headquartered in Osaka and operating plants across Japan, Korea, China, and the United States. The business grew historically out of by-products of the manufactured-gas era — coke oven gas, tar, and the chemical streams produced when coal is gasified — and has been progressively reshaped into a portfolio that has very little to do with the rest of the group’s energy operations. Activated carbon and adsorbents for water purification, semiconductor manufacturing, and environmental remediation are a substantial line. Fluorene-based fine chemicals — particularly OGSOL fluorene derivatives used in high-refractive-index optical films, semiconductor photoresists, and advanced display materials — are a high-margin niche where the subsidiary has effectively built a global category position. Aromatic chemicals, carbon black, specialty resins, wood-preservation chemicals, and concrete admixtures round out the portfolio.

The strategic significance is that the subsidiary operates at the materials-supplier end of several growth industries — semiconductors, displays, batteries, environmental treatment — that are largely independent of the gas-utility business cycle. For a regulated utility, having a meaningful chunk of group earnings derived from B2B materials that move with electronics demand and environmental capex, rather than with city-gas tariffs, is genuine diversification of operating exposure.

Deregulation, electricity retail, and the cross-sell into Kansai homes

Japan deregulated retail electricity in April 2016, allowing city-gas utilities and other non-incumbent suppliers to compete with the regional electricity monopolies for residential and small-commercial accounts. For Osaka Gas, this was a major strategic opening. The dominant incumbent in the Kansai region is Kansai Electric Power — KEPCO — which had run electricity retail in the region as a regulated monopoly since the 1950s.

Osaka Gas entered electricity retail in 2016 under the Osaka Gas Electricity brand, leveraging its existing customer relationships across roughly seven million city-gas accounts to cross-sell electricity service. The proposition was simple: bundled gas and electricity billing, modest pricing advantages, and a single customer-service relationship instead of two. By the early 2020s the utility had built up an electricity retail book in the millions of accounts, drawn predominantly from KEPCO’s incumbent base. The strategy mirrors what Tokyo Gas has done against TEPCO in Kanto.

Generation capacity to back the electricity retail business has been built out through power purchase agreements with independent power producers, equity in gas-fired generation projects, and cogeneration partnerships. Notable among the latter is the joint venture with Daiwa House and Toshiba on cogeneration systems for housing and commercial buildings — Osaka Gas’s bet that distributed cogeneration, particularly fuel-cell-based combined heat and power, is a long-run technology platform for the utility’s customer base.

The Life & Business Solutions stack, and why it matters

Outside the energy and chemicals operations, Osaka Gas operates what it calls Life & Business Solutions — a portfolio of consumer-facing and B2B services built around the utility’s customer base. The mix includes home equipment (gas appliances, hot-water systems, kitchen units, air conditioners), residential security through partnerships, real estate development through Osaka Gas Urban Development, and information-services and IT subsidiaries. The dollars are smaller than energy or chemicals, but the logic is the long-tail monetisation of the seven-million-account customer relationship — a customer book whose acquisition cost within the franchise is effectively zero, and into which water heaters, fuel-cell systems, home renovations, and security monitoring can be sold at incremental margin.

Decarbonisation, e-methane, and the long-run question

The largest strategic uncertainty for Osaka Gas — and for every city-gas utility globally — is what happens to natural gas demand in a decarbonising economy. The utility’s public communications point toward several technology pathways: e-methane, produced synthetically from green hydrogen and captured CO2 and injected into the existing gas grid; biomethane from organic waste; hydrogen blending and eventually direct hydrogen distribution; and carbon capture, utilisation, and storage attached to gas-fired generation and industrial processes. None of these technology pathways is yet at the cost or scale required to maintain the gas business at its current size in a 2050 net-zero scenario. Osaka Gas’s strategy, in practice, is to remain a credible commodity buyer and integrated supplier through the 2030s and 2040s — extracting full value from its US upstream and LNG positions — while progressively trialling e-methane and hydrogen blending at scale. The Sabine acquisition fits within that framing: a long-dated upstream position can be a thirty-year asset if the molecules continue to flow, and Haynesville gas blended progressively with green molecules at the destination can extend the life of the existing infrastructure.

Why Osaka Gas matters to non-Japanese counterparties

For LNG suppliers and traders, Osaka Gas is a top-five Japanese LNG buyer with an integrated upstream-to-burner-tip position. For US oil-and-gas operators, the Sabine subsidiary is now a routine industry counterparty in the Haynesville and Cotton Valley plays. For specialty-chemicals buyers in semiconductors, displays, batteries, and environmental treatment, Osaka Gas Chemicals is a global supplier in several niche product categories with established customer relationships across Asia, North America, and Europe. For real estate, residential security, and home-services partners, the utility’s customer-facing brand is one of the strongest in the Kansai region.

What distinguishes Osaka Gas from its larger Tokyo counterpart is not the size of the franchise. It is the extent of vertical integration internationally, the depth of the chemicals diversification, and the willingness to take operating control of foreign upstream assets rather than holding passive minority stakes. Those things compound, and they show up in how the utility approaches LNG procurement, how it staffs its Houston-based subsidiary, and how it underwrites long-dated capital commitments in materials and electricity. For a foreign company looking at the Japanese energy and industrial markets, Osaka Gas is a Kansai-anchored counterparty whose business is quietly more international than the name suggests.

FAQ

Who owns Osaka Gas?

Osaka Gas Co., Ltd. is a publicly listed company on the Tokyo Stock Exchange under ticker 9532. Ownership is broadly distributed across Japanese trust banks acting on behalf of institutional investors, global asset managers, and individual shareholders. There is no controlling shareholder, no founding family block, and no state ownership stake. Cross-shareholdings with selected Kansai-region partners exist but are modest. The company has been continuously listed and has never undergone a state-led restructuring or capital reset.

Why did Osaka Gas buy Sabine Oil & Gas in 2020?

The acquisition, valued at approximately six hundred and ten million dollars, gave Osaka Gas full ownership of a Houston-based independent producer with acreage in the Cotton Valley and Haynesville shale plays across East Texas and North Louisiana. The strategic logic was vertical integration: by owning upstream production directly, Osaka Gas could feed its US LNG offtake from Freeport and Cameron with molecules from its own wells, capturing producer margin alongside the liquefaction and shipping margin. It also gave the utility operating control of a US upstream organisation, rather than the non-operated minority positions Japanese utilities had historically taken. Sabine continues to operate as a wholly owned US subsidiary.

What is Osaka Gas’s relationship with Freeport LNG?

Osaka Gas holds an equity stake and offtake position in the Freeport LNG export terminal on Quintana Island, Texas, alongside JERA, Sempra Infrastructure as the major equity partner, and other Japanese and international counterparties. Freeport’s three liquefaction trains came online through 2019-2020 with combined nameplate capacity of approximately fifteen million tonnes per year. Osaka Gas’s Freeport position, combined with offtake from the Sempra-led Cameron LNG project in Hackberry, Louisiana, gives the utility a US Gulf Coast supply base of roughly two million tonnes per year of contracted LNG, with optionality to lift additional cargoes as market conditions allow.

How does Osaka Gas compare with Tokyo Gas?

Tokyo Gas is the larger of the two by customer base and gas volume — approximately twelve million customers against Osaka Gas’s seven million — and operates a larger LNG terminal complex serving the Kanto region. Osaka Gas is the more internationally vertically integrated of the two, owning the full Sabine Oil & Gas upstream organisation and holding meaningful equity in US LNG liquefaction. Osaka Gas Chemicals is also a substantially larger specialty-materials business than its Tokyo Gas equivalent. Both utilities have entered electricity retail since the 2016 deregulation and run cross-selling strategies against their respective regional electricity incumbents.

What does Osaka Gas Chemicals actually make?

Osaka Gas Chemicals operates several specialty-chemicals product lines including activated carbon and adsorbents for water purification and semiconductor manufacturing, fluorene-based fine chemicals — notably OGSOL fluorene derivatives used in high-refractive-index optical films, semiconductor photoresists, and advanced display materials — aromatic chemicals, carbon black, specialty resins, wood-preservation chemicals, and concrete admixtures. The business operates plants across Japan, Korea, China, and the United States and sells globally to semiconductor, display, battery, environmental-treatment, and construction customers. It functions effectively as an industrial-materials company that happens to be owned by a Japanese city-gas utility.

Working with Osaka Gas

For LNG suppliers and traders, the practical entry point to Osaka Gas is through the company’s LNG procurement organisation in Osaka and its US subsidiaries in Houston, with negotiated long-term and spot offtake contracts, joint development opportunities on liquefaction projects, and shipping and trading partnerships. For US upstream and midstream counterparties, Sabine Oil & Gas operates as a routine industry participant in the East Texas / North Louisiana plays and is a credible counterparty for acreage trades, joint operating agreements, and midstream partnerships. For specialty-chemicals buyers, Osaka Gas Chemicals handles direct sales and technical support through regional offices in Japan, Korea, China, and the United States across activated carbon, fluorene fine chemicals, and aromatic chemical product lines.

Beyond the energy and chemicals operations, the broader Osaka Gas group ecosystem — Osaka Gas Urban Development for real estate, Osaka Gas Information System Research Institute and IT subsidiaries, the Life & Business Solutions home-equipment and services portfolio — represents a substantial set of additional commercial relationships that foreign suppliers can pursue independently of the utility itself.

If your company provides LNG supply, upstream oil and gas services, midstream infrastructure, specialty chemicals and materials, decarbonisation technology, residential energy products, or real estate and digital services relevant to Osaka Gas — or if you are evaluating Kansai-region energy and industrial markets as part of a Japan strategy — Japonity’s business matching service can help structure a credible first conversation with the right counterparty inside the Osaka Gas group.

Related from Japonity — Japan’s electric & gas utilities

- TEPCO Holdings — Japan’s largest utility, still rebuilding from Fukushima

- Kansai Electric Power — Japan’s most nuclear-dependent utility

- Chubu Electric Power — Toyota’s home-region utility and the JERA LNG empire

- Tokyo Gas — Japan’s largest gas utility — and an LNG arbitrageur

Want to source Japanese products beyond these company profiles? Japonity also runs a Japan Sourcing Hub — a research-grade catalogue of 1,185 verified Japanese food products and 200+ overseas EC stores, ready for B2B procurement.

Interested in Japanese business opportunities?

Whether you're looking for technology partners, engineering talent, or market insights — we can help connect you with the right Japanese organizations.

Get in Touch →