In the early hours of 11 February 2024, two of Japan’s most recognisable corporate names — KDDI Corporation, the country’s second-largest mobile carrier, and Mitsubishi Corporation, the largest of the five general trading houses — announced that they would jointly take Lawson, the third-largest convenience-store chain, private at a valuation of roughly 600 billion yen, or approximately 3.5 billion dollars at then-prevailing rates. The tender offer closed later that year, ending Lawson’s three-decade run as a Tokyo Stock Exchange-listed company and producing one of the most unusual ownership structures in Japanese corporate history: a fifty-fifty split between a sogo shosha and a telco. For KDDI, with its approximately 60 million au-brand mobile subscribers, its 5.7-trillion-yen annual revenue base, its UQ Mobile sub-brand, its povo low-cost line, its au PAY mobile wallet, its enterprise data-centre franchise and its 2022 partnership with SpaceX to bring Starlink to Japan, the Lawson deal was the boldest expression yet of a strategy that has slowly stretched the definition of “telecom company” beyond recognition.

A merger of three histories

KDDI in its current form is younger than it looks. The corporation was created in October 2000 from the simultaneous merger of three telecom firms whose origins span almost half a century of Japanese communications policy. KDD — Kokusai Denshin Denwa — was founded in 1953 as the country’s monopoly international carrier, spun out of the postwar Nippon Telegraph and Telephone Public Corporation to handle overseas calls and cable traffic. DDI Corporation, more formally Daini Denden, was launched in 1984 by Kazuo Inamori, the founder of Kyocera, as one of the first private challengers to the newly privatised NTT, riding the wave of telecom deregulation that defined late-Showa industrial policy. IDO — Nippon Idou Tsushin — was a regional mobile carrier serving the Kanto and Tokai areas, backed by Toyota and a constellation of central-Japan industrial firms. The three companies had complementary footprints, overlapping shareholders and a common adversary in NTT. Their merger created the only Japanese carrier capable of competing with NTT across international, fixed-line and mobile services simultaneously.

The “au” brand, launched alongside the merger, became the operational face of the new group’s mobile business. Within a few years au had pulled even with NTT DoCoMo on technology — KDDI was the first carrier in Japan to introduce CDMA2000 1xEV-DO, the first to launch a serious mobile-music store with LISMO, and an early mover on LTE. By the time the smartphone era arrived, KDDI had positioned au as the design-conscious, family-friendly alternative to the engineering-led DoCoMo and the disruptive SoftBank, the latter having burst onto the scene by acquiring Vodafone Japan in 2006 and securing the original iPhone exclusive in 2008.

The four-carrier market, in numbers

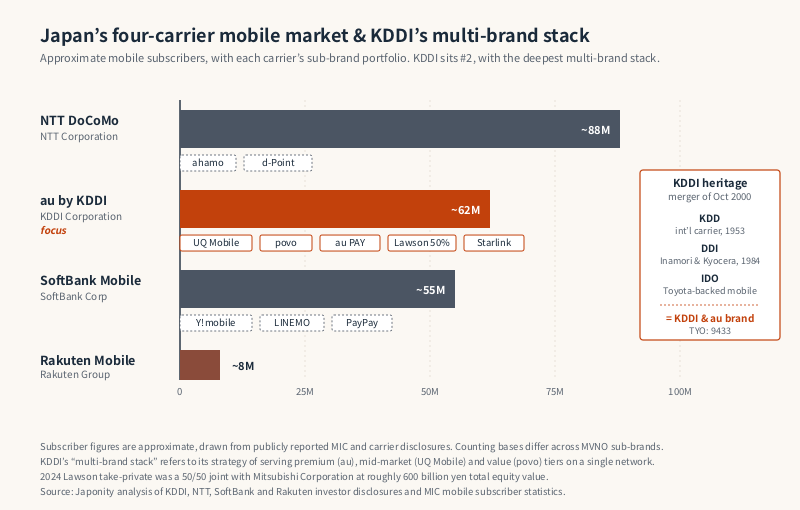

The Japanese mobile market settled into a long oligopoly during the 2010s. After Rakuten Mobile’s commercial launch in April 2020 as the country’s fourth full mobile network operator, the structure became a four-way contest, although Rakuten’s subscriber base remains a small fraction of the three incumbents. The table below sketches the contemporary picture using publicly reported figures, with the usual caveat that subscriber counts are reported on subtly different bases by each carrier and across MVNO sub-brands.

| Carrier | Parent | Approx. mobile subscribers | Signature sub-brand or play |

|---|---|---|---|

| NTT DoCoMo | NTT Corporation | ~88 million | ahamo low-cost line, d-Point ecosystem |

| au by KDDI | KDDI Corporation | ~62 million | UQ Mobile, povo, au PAY, Lawson tie-up |

| SoftBank Mobile | SoftBank Corp | ~55 million | Y!mobile, LINEMO, PayPay ecosystem |

| Rakuten Mobile | Rakuten Group | ~8 million | Open RAN network, Rakuten Points loop |

The numbers tell only part of the story. Japanese carriers have for two decades cross-subsidised handsets, bundled fixed-line broadband and television into mobile plans, and woven loyalty-point economies — d-Points, Pontas, PayPay points, Rakuten Points — into household financial flows. The 2020 administrative pressure from then-prime-minister Yoshihide Suga to cut mobile tariffs by around 40 percent forced all four carriers to launch online-only discount brands within roughly six months: DoCoMo’s ahamo, KDDI’s povo, SoftBank’s LINEMO. The price reset compressed margins industry-wide and accelerated the search for non-telecom revenue, which is the context for everything KDDI has done since.

From pipe to platform: the segment portfolio

KDDI’s annual reports group activities under five operating headings, and the relative weighting tells the strategic story. The Personal Services segment — au, UQ Mobile, povo and consumer broadband — remains the revenue anchor, accounting for the majority of group sales. Business Services covers enterprise mobile, fixed-line, network integration and the rapidly growing IoT and data-centre franchises. Lifestyle Design wraps the financial businesses (au Jibun Bank, au Kabucom Securities, au Asset Management), au PAY, the energy reseller au Denki, and now the Lawson stake. Global Business runs the Telehouse-branded international data-centre operation, Myanmar joint ventures, and Asian and US subsidiaries. Other includes group-internal services.

The shift away from the traditional carrier income statement is most visible in Lifestyle Design. A decade ago this segment did not meaningfully exist; today it is one of the principal vectors for management’s “Satellite Growth Strategy,” in which the carrier-platform core is surrounded by adjacent businesses that monetise the customer relationship beyond the monthly mobile bill. au PAY, launched in 2019 in response to PayPay’s explosive growth, is the consumer payment layer. au Jibun Bank is the deposit and lending balance sheet. au Kabucom is the securities account. Together they form a financial-services stack that competes directly with the platforms built by SoftBank around PayPay and by Rakuten around Rakuten Bank and Rakuten Card.

The Lawson take-private, examined

To understand why KDDI partnered with Mitsubishi Corporation to take Lawson private rather than buying its own convenience-store chain, it helps to recall how Lawson came to be controlled by Mitsubishi in the first place. Lawson originated as a US-licensed chain brought to Japan by Daiei in the 1970s. After Daiei’s collapse in the early 2000s, Mitsubishi Corporation acquired the controlling interest and gradually lifted its stake, treating Lawson as the consumer-distribution anchor of the trading house’s domestic strategy. By 2024 Mitsubishi held just over 50 percent, the public float was modest, and the strategic logic of full ownership had been visible for years. What was new in 2024 was the partner.

KDDI’s purchase of half of Lawson — at an offer price of 10,360 yen per share, financing roughly half of the take-private’s equity bill — bought it three things that a telco cannot easily build organically. The first was a physical retail network of approximately 14,600 Lawson stores across Japan, each one a potential pickup point for au-related services, a distribution outlet for KDDI’s MVNOs, an installation site for self-service technology and a node in the household-finance fabric. The second was access to roughly ten million daily Ponta-card customer interactions, which when combined with au PAY transaction data give KDDI a depth of consumer behavioural information rivalled in Japan only by SoftBank-PayPay and Rakuten. The third, less tangible, was a strategic alliance with the most globally connected sogo shosha — a relationship that opens doors in food, energy, mobility and overseas markets that pure-play telcos rarely walk through.

Whether the financial returns will justify the price is a separate question. Convenience-store growth in Japan is mature, labour costs are climbing, and the unit economics of small-format retail are under pressure from inflation and from the relentless expansion of Seven-Eleven, the segment leader by a wide margin. KDDI’s bet is that the value comes not from Lawson’s standalone operating profit but from the data, distribution and customer-relationship synergies — a thesis whose payoff will be measured in years rather than quarters.

UQ Mobile, povo and the multi-brand stack

KDDI’s response to the 2020 price war was structurally distinct from its peers. Rather than create a single online-only brand — DoCoMo’s choice with ahamo, SoftBank’s choice with LINEMO — KDDI deployed a three-layered portfolio. au remained the premium-branded carrier service sold through stores. UQ Mobile, the brand inherited from the WiMAX 2.1 mobile data business and converted into an MVNO sub-brand running on the au network, served the value-conscious mid-market with physical-store distribution and family discounts. povo, launched in 2021 as a fully digital, contract-free, pay-as-you-go service, served the price-driven and feature-flexible younger market.

The three brands share KDDI’s spectrum and infrastructure but are positioned to capture different consumer segments without cannibalising the core au margins as aggressively as a single-brand price cut would. The trade-off is operational complexity — three product roadmaps, three customer-service organisations, three marketing budgets — but the structural elegance is that KDDI now has a brand to compete at almost any price-feature point in the market. For foreign B2B players, the multi-brand stack matters because the procurement channel for, say, mobile applications, network services or fintech products differs by brand. A partnership announced for au may not extend to povo, and vice versa.

Telehouse, data centres and the global B2B layer

Less visible to consumers but increasingly central to KDDI’s enterprise story is Telehouse, the international data-centre brand that the company has built up through more than three decades of acquisition and organic expansion. Telehouse operates carrier-neutral colocation facilities in London, Paris, Frankfurt, New York, Los Angeles, Singapore, Hong Kong, Bangkok, Jakarta and other major hubs, alongside a substantial Japanese footprint. The brand carries unusual weight in the network industry because its London Docklands campus is one of the principal interconnection points between European internet networks, a role accumulated through the carrier-neutral peering economy of the 1990s and never relinquished.

For KDDI the Telehouse business performs two functions. It is a meaningful operating profit contributor to the Global segment, with the AI-driven data-centre demand cycle now pushing colocation pricing power higher across major hubs. And it is a relationship layer: enterprises that contract with Telehouse for international network connectivity become natural customers for KDDI’s domestic Japan enterprise services, IoT platforms, cloud-integration practice and increasingly its security business. For foreign companies entering Japan that already use Telehouse outside the country, the KDDI enterprise sales motion is the obvious next step — a fact that the company’s account teams have learned to exploit.

Starlink Japan and the satellite frontier

In 2022 KDDI announced an exclusive partnership with SpaceX to bring Starlink, the low-earth-orbit satellite broadband service, to Japan. The deal made KDDI the country’s distribution partner for Starlink business and consumer services, integrated Starlink backhaul into KDDI’s mobile base-station planning for remote areas, and positioned the carrier as the operator of choice for satellite-to-mobile direct services as those become commercially available. Subsequent agreements expanded the partnership to include direct-to-cell capability — the ability for ordinary au smartphones to connect to Starlink satellites in areas without terrestrial coverage — and rolled the service out to remote islands, mountain regions and disaster scenarios where terrestrial networks fail.

The Starlink relationship is strategically important for two reasons beyond its immediate revenue contribution. It positions KDDI ahead of DoCoMo and SoftBank in the satellite-mobile convergence that several analysts expect to reshape the rural and disaster-resilient connectivity business. And it gives the company a credentialed relationship with the most influential private space company in the world, in a country where space industry policy is now strategically important to both economic security and US-Japan technology cooperation.

Leadership, capital and the Inamori shadow

Makoto Takahashi has served as president and chief executive of KDDI since 2018, succeeding Takashi Tanaka and continuing the lineage of operationally focused leaders the company has favoured throughout its post-merger history. Takahashi has steered the firm through the 2020 price reset, the launch of povo, the Lawson take-private and the deepening of the Lifestyle Design segment, and his investor communications increasingly frame KDDI not as a mobile carrier with adjacencies but as a “Life Transformation” platform — an awkward English phrase whose Japanese equivalent, “Tsumugu,” captures the idea of weaving telecom, finance, retail, energy and lifestyle services into a single customer relationship.

The cultural backdrop is still recognisably the legacy of Kazuo Inamori, who died in 2022 and whose Kyocera-rooted management philosophy — amoeba management, the pursuit of “doing the right thing as a human being,” the disciplined return-on-sales focus — pervaded DDI from its founding and remained influential at KDDI long after the merger. KDDI’s relatively conservative balance sheet, its insistence on through-cycle dividend growth and its bias for organic capacity-building over splashy acquisition all bear Inamori’s fingerprints. The Lawson take-private was a partial departure from that pattern, and how KDDI integrates its half of the deal will reveal whether the Inamori-influenced disciplines still bind.

FAQ

Is KDDI larger than DoCoMo?

No. NTT DoCoMo remains Japan’s largest mobile carrier by subscribers, with roughly 88 million users against KDDI’s au-group total of approximately 62 million. KDDI is the second-largest carrier and the second-largest Japanese telecom group by revenue after NTT, which through DoCoMo and its fixed-line and enterprise units operates at a substantially larger scale.

Why did KDDI buy half of Lawson?

The 2024 take-private with Mitsubishi Corporation gave KDDI access to approximately 14,600 retail outlets, roughly ten million daily Ponta-card customer interactions and a strategic alliance with the largest Japanese trading house. The economic thesis is that data, distribution and cross-selling synergies — feeding au PAY, KDDI’s financial services, and enterprise capabilities — will generate returns beyond Lawson’s standalone operating profit, although the payoff will be measured in years.

What is the difference between au, UQ Mobile and povo?

All three run on KDDI’s network. au is the premium retail brand sold through stores with full handset financing and family bundles. UQ Mobile is the mid-market sub-brand, originally a WiMAX 2.1 mobile data business, now an MVNO-style line emphasising value and store distribution. povo, launched in 2021, is the fully digital, contract-free, pay-as-you-go offering targeted at price-sensitive younger users. The multi-brand portfolio lets KDDI compete at multiple price-feature points without cannibalising au margins as aggressively as a single-brand price cut would.

Is KDDI partnered with SpaceX?

Yes. KDDI announced a Starlink partnership with SpaceX in 2022, becoming the Japanese distribution partner for Starlink business and consumer services and integrating satellite backhaul into au base-station planning. Subsequent agreements extended the partnership to direct-to-cell satellite-to-smartphone capability, positioning au users to connect via Starlink satellites in areas without terrestrial coverage.

How does KDDI fit into the Mitsubishi keiretsu?

KDDI is not formally part of the historical Mitsubishi keiretsu in the way Mitsubishi Heavy Industries or Mitsubishi UFJ Financial Group are. However, the 2024 Lawson take-private with Mitsubishi Corporation created an unusually deep operational tie between the two firms, and Toyota Group entities have historically held significant stakes in KDDI dating back to the IDO heritage. The most accurate description is that KDDI sits at an intersection of relationships — closer to Mitsubishi via Lawson, closer to Toyota via legacy IDO shareholdings — without belonging exclusively to either group.

Working with KDDI

For foreign B2B telecom, fintech, mobility and enterprise-technology companies, KDDI is one of the most accessible counterparties in Japanese corporate life: an English-fluent international division, the Telehouse global enterprise franchise, a multi-brand mobile portfolio that opens different distribution channels, a fintech stack hungry for adjacent products, and now a 14,600-store retail surface through Lawson. Engagement typically begins through enterprise-sales contacts in Tokyo, the Telehouse account teams in your home market, or the corporate development office for partnership and equity discussions.

Japonity helps overseas companies prepare partnership approaches to KDDI and the broader Japanese telecom-fintech-retail cluster, with a focus on understanding which brand, which segment and which decision-maker matters for a given proposition. Companies interested in introductions can begin via /business-matching/.

Related from Japonity — Japan’s telecom & digital ecosystems

- SoftBank Group — From PHS reseller to Arm + Stargate AI infrastructure giant

- Rakuten Group — The points-economy empire and the mobile bet that almost broke it

- LY Corporation (LINE Yahoo) — Japan’s super-app holding company — SoftBank + Naver under government pressure

- DeNA — From Mobage to BayStars to Pococha to MaaS — Japan’s most under-appreciated reinvention

- NTT Corporation — Japan’s $140B telecom giant and the IOWN photonic-network bet

Want to source Japanese products beyond these company profiles? Japonity also runs a Japan Sourcing Hub — a research-grade catalogue of 1,185 verified Japanese food products and 200+ overseas EC stores, ready for B2B procurement.

Interested in Japanese business opportunities?

Whether you're looking for technology partners, engineering talent, or market insights — we can help connect you with the right Japanese organizations.

Get in Touch →