In January 2004, two of Japan’s oldest life insurers — Meiji Life (founded 1881, Mitsubishi-affiliated) and Yasuda Life (founded 1880, of the former Yasuda zaibatsu lineage) — combined to form Meiji Yasuda Life Insurance Company. Twelve years later, in 2016, the merged group paid approximately five billion US dollars for StanCorp Financial Group of Portland, Oregon, planting the Japanese insurer in the US group long-term disability market in one of the largest cross-border insurance acquisitions of the decade. Today Meiji Yasuda holds approximately forty trillion yen in total assets, ranks as Japan’s third-largest life insurer behind Nippon Life and Dai-ichi Life, and — alongside Nippon Life and Sumitomo Life — remains one of the three large mutual life insurers (相互会社) that have declined to demutualize and list on the Tokyo Stock Exchange. That structural choice, more than any product line, defines how foreign reinsurers, asset managers, and capital-markets partners can — and cannot — engage with the company.

A merger of two zaibatsu-era institutions

The 2004 combination joined two firms whose roots reach back more than a century. Meiji Life Insurance, established in 1881 under what would later become the Mitsubishi group of companies, was Japan’s first modern life insurer. Yasuda Life Insurance, founded the year before in 1880, was the insurance arm of the Yasuda zaibatsu — the financial conglomerate built by Zenjiro Yasuda that, after postwar dissolution, scattered into what is now broadly identified as the Fuyo Group, with Mizuho Bank as its banking nucleus.

Both insurers had survived the Meiji-era founding wave, two world wars, the SCAP-era zaibatsu dissolution, the high-growth period, and the prolonged life-insurance industry stress of the late 1990s and early 2000s — during which several mid-sized Japanese life insurers failed. By 2003, with the domestic life market shrinking on demographics and yield-starved by ultra-low JGB rates, scale and balance-sheet strength were no longer optional. The combined Meiji Yasuda Life launched on 1 January 2004 with the merged headquarters in the Marunouchi district of central Tokyo, immediately becoming one of Japan’s “Big Four” life insurers by assets and premium income.

The “Big Four” mutual life insurers — and the holdouts

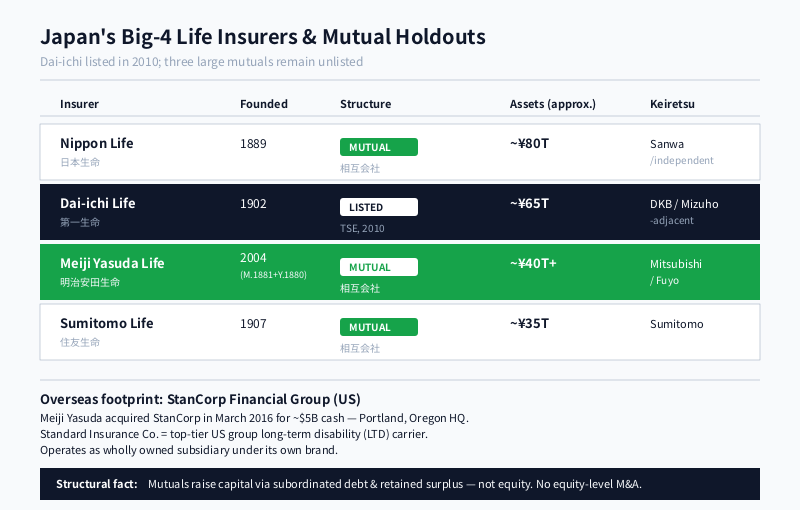

Japan’s life insurance sector is unusual among developed-market peers in that its largest carriers are not joint-stock corporations but mutuals — entities owned, in legal theory, by their policyholders. Three of the country’s four largest life insurers remain so structured. Dai-ichi Life broke ranks in 2010, demutualizing and listing on the Tokyo Stock Exchange; the other three large mutuals have, so far, opted to remain private.

| Insurer | Founded | Structure | Approx. total assets | Keiretsu / lineage |

|---|---|---|---|---|

| Nippon Life | 1889 | Mutual (相互会社) | ~¥80T | Sanwa / independent |

| Dai-ichi Life | 1902 | Joint-stock (TSE-listed, 2010) | ~¥65T | DKB / Mizuho-adjacent |

| Meiji Yasuda Life | 2004 (Meiji 1881 + Yasuda 1880) | Mutual (相互会社) | ~¥40T+ | Mitsubishi / Fuyo |

| Sumitomo Life | 1907 | Mutual (相互会社) | ~¥35T | Sumitomo |

For foreign counterparties, the mutual-versus-listed distinction is not cosmetic. Listed life insurers — Dai-ichi at home, Prudential Financial, MetLife, AIA Group abroad — operate under continuous public-market discipline, with quarterly investor calls, equity-financed M&A, and management compensation tilted to total shareholder return. Mutuals do not. Capital is raised primarily through subordinated debt and retained surplus; “shareholders” are policyholders who vote, in principle, through a representative assembly. Decision cycles are longer, dividend policy is replaced by policyholder dividend (配当), and the firm’s strategic horizon can run a decade or more without market-cap pressure.

This is the structural fact that frames every conversation a foreign partner will have with Meiji Yasuda Life. The firm cannot issue equity to fund an acquisition. It will not be approached by an activist. It will not be acquired. What it can do — and has done — is deploy its own surplus capital, plus subordinated debt, into wholly owned subsidiaries overseas.

StanCorp Financial Group: the US disability bet

The clearest expression of that capacity is the StanCorp Financial Group acquisition, completed in March 2016 for approximately five billion US dollars in cash. StanCorp, headquartered in Portland, Oregon, was a mid-cap US insurance holding company best known as the parent of Standard Insurance Company — a top-tier provider of group long-term disability (LTD) insurance to US employers, with a smaller life and retirement-plan recordkeeping business attached.

For Meiji Yasuda, the rationale was not opportunistic. Domestic Japanese life premiums had been declining or flat for the better part of a decade; the population was aging; ultra-low JGB yields were compressing the spread between credited rates and investment returns. Group disability insurance in the US offered three things the Japanese book could not: a benefit type virtually absent from the Japanese individual-life market, a regulated US dollar–denominated asset base, and access to the deep US fixed-income market for asset-liability matching. StanCorp was not a turnaround target; it was a stable mid-cap US carrier that could keep operating as a wholly owned subsidiary with its existing management and brand.

Roughly ten years on, StanCorp continues to operate from Portland under its own name in the US distribution market. Meiji Yasuda has subsequently added smaller US asset-management and insurance positions, but StanCorp remains the cornerstone of its overseas insurance footprint by a wide margin.

The structural lesson of the StanCorp deal is worth underlining for any foreign carrier evaluating a Japanese counterparty. Meiji Yasuda did not look for a control stake in a publicly traded US life insurer with overlapping product lines; it acquired a mid-cap specialist whose dominant product — group LTD — was complementary rather than competitive with its Japanese book, and whose management team could be retained without integration friction. That template — wholly owned, specialist-complementary, brand-preserved — is the most likely shape of any future overseas acquisition by a Japanese mutual life insurer, including Meiji Yasuda itself.

Bancassurance, group life, and the Mitsubishi connection

Domestically, Meiji Yasuda Life sits inside two overlapping distribution architectures. The first is its own captive sales-representative channel — the “life planner” model that all major Japanese life insurers operate, with tens of thousands of agents (営業職員) calling on individual and small-business customers. The second is bancassurance: insurance products distributed through retail bank branches, an arrangement liberalized in Japan in stages between 2001 and 2007.

Meiji Yasuda’s bancassurance partnerships extend across most of Japan’s major retail banks, but the Mitsubishi lineage — Meiji Life’s pre-merger affiliation with what is now Mitsubishi UFJ Financial Group — has historically given the firm a privileged shelf position with MUFG-affiliated channels. The Yasuda side of the merger brings a corresponding connection to the broader Fuyo / Mizuho orbit. For foreign asset managers seeking sub-advisory mandates, or foreign reinsurers seeking ceded-business relationships, those keiretsu adjacencies still matter — not as exclusivity, but as introductions.

The firm’s group-life and group-pension business — selling life insurance and corporate pension products to Japanese employers — is one of the largest in the country and a significant institutional channel into Japan’s defined-benefit and defined-contribution corporate retirement market.

The investment portfolio: ~¥40T of liabilities to match

Approximately forty trillion yen in total assets — the rough scale of Meiji Yasuda’s general account — has to be invested somewhere. The composition is broadly similar to peers: a heavy allocation to Japanese government bonds (JGBs) for asset-liability matching against long-duration life liabilities, a meaningful allocation to foreign bonds (predominantly US treasuries and high-grade credit, hedged or unhedged depending on yield differentials), domestic and foreign equities, and a growing allocation to alternatives — private equity, private credit, real estate, and infrastructure.

For foreign asset managers, this is the most accessible commercial entry point. Japanese mutual life insurers are among the most coveted limited-partner relationships globally: long-dated capital, low redemption pressure, and ticket sizes that make a difference to a fund’s close. Competition for those mandates is intense, gatekeeper requirements are strict (long track records, audited returns, ESG documentation, Japanese-language reporting where applicable), and the relationship arc is measured in years rather than quarters. But the door is open in a way that, say, an M&A approach to the holding company itself is not.

The yen-hedging cost on foreign-bond holdings — driven by the gap between USD and JPY policy rates — has been the dominant tactical variable for Japanese life insurer general accounts for several years. Periods of elevated hedge cost push allocations toward unhedged foreign bonds, domestic credit, or alternatives; periods of compressed hedge cost reverse the flow. Foreign managers pitching to Meiji Yasuda and its peers should expect the conversation to include not just track-record diligence but a detailed view on how the strategy fares under different yen-hedge regimes.

J.League sponsorship and brand visibility

Outside financial circles, Meiji Yasuda Life’s most visible presence in Japan is sport. Since 2015 the company has been the title sponsor of the country’s top professional football competition — branded “Meiji Yasuda Life J.League” — across J1, J2, and J3. The sponsorship was renewed in subsequent multi-year cycles and remains in force through the 2024 season and beyond, making Meiji Yasuda one of the most recognized B2C insurance brands in Japan among consumers who would otherwise have little reason to compare life insurers.

This matters more than it sounds. In a mutual-company structure with no equity ticker and limited consumer brand differentiation among the Big Four, mass-market visibility is one of the few levers available for top-of-funnel brand equity that supports the captive sales channel. The J.League partnership has effectively become a cornerstone of that strategy.

Leadership and governance

Meiji Yasuda Life is led by President Yusuke Hibino, who succeeded Akio Negishi (now chairman) as the firm’s chief executive in recent years. Governance follows the standard Japanese mutual structure: a representative assembly of policyholders (総代会) elects directors, who in turn appoint the executive team. The board includes outside directors in line with the corporate-governance code applied to large mutuals.

The result is a governance system that is, by design, slower-moving and more consensus-oriented than that of a listed insurer — but also more insulated from quarterly noise. Foreign counterparties evaluating Meiji Yasuda as a partner should plan for relationship-led, multi-year engagement cycles rather than transactional pitches.

What it means for foreign partners

For a foreign reinsurer, asset manager, distribution partner, or technology vendor evaluating Meiji Yasuda Life, three structural realities frame everything else.

First, the firm is a mutual and will remain so for the foreseeable future. Equity-level transactions — minority stakes, joint-venture equity, public-market financing — are not on the menu. Commercial relationships are.

Second, capital deployment overseas runs through wholly owned subsidiaries (StanCorp being the model) rather than minority partnerships. A foreign insurer hoping to be acquired by Meiji Yasuda is in a different conversation from one hoping to reinsure its business.

Third, the firm’s keiretsu lineage — Mitsubishi on the Meiji side, Fuyo / Mizuho on the Yasuda side — still matters for introductions, distribution, and asset-management mandates, even if it no longer dictates exclusivity. The relationship architecture of Japanese finance has loosened, but it has not disappeared.

Within those constraints, Meiji Yasuda Life is one of the most consequential institutional capital pools in Japan, with an established track record of cross-border execution and a long planning horizon that rewards partners willing to invest in the relationship.

FAQ

When was Meiji Yasuda Life formed, and from which companies?

Meiji Yasuda Life Insurance Company was formed on 1 January 2004 from the merger of Meiji Life Insurance (founded 1881, Mitsubishi-affiliated) and Yasuda Life Insurance (founded 1880, of the former Yasuda zaibatsu lineage). The headquarters is in Marunouchi, Tokyo.

Is Meiji Yasuda Life publicly listed?

No. Meiji Yasuda Life remains a mutual company (相互会社), legally owned by its policyholders rather than by shareholders. It is one of three large Japanese life insurers — alongside Nippon Life and Sumitomo Life — that have declined to demutualize. Dai-ichi Life is the only one of Japan’s “Big Four” life insurers to have listed (in 2010).

What is the StanCorp Financial Group acquisition?

In March 2016, Meiji Yasuda Life completed the acquisition of StanCorp Financial Group, a Portland, Oregon–based US insurance holding company, for approximately five billion US dollars in cash. StanCorp’s primary business is group long-term disability (LTD) insurance through Standard Insurance Company, sold to US employers. StanCorp continues to operate under its own brand as a wholly owned subsidiary.

How large is Meiji Yasuda Life by assets?

Meiji Yasuda Life holds approximately forty trillion yen in total assets, ranking it the third-largest life insurer in Japan behind Nippon Life and Dai-ichi Life, and ahead of Sumitomo Life. Figures vary by reporting period and accounting basis; approximate values are appropriate for partner-screening purposes.

How can a foreign company partner with Meiji Yasuda Life?

The most accessible commercial channels for foreign counterparties are asset-management mandates (sub-advisory and direct allocations from the general account), reinsurance and retrocession on group and individual life books, and technology / service provision to the firm’s insurance operations. Equity-level transactions with the holding company are not available given its mutual structure.

Working with Meiji Yasuda Life

Japonity helps foreign reinsurers, asset managers, and capital-markets counterparties navigate Japan’s three remaining large mutual life insurers — Meiji Yasuda Life among them — where keiretsu lineage, mutual-company structure, and multi-year relationship cycles shape every commercial conversation. If your firm is evaluating a Japanese institutional relationship, visit our business matching page to be introduced to the right counterparties.

Related from Japonity — Japan’s life insurers

- Dai-ichi Life Holdings — Japan’s largest listed life insurer — Protective Life US, TAL Australia

- Nippon Life Insurance — Japan’s largest life insurer — the unlisted mutual giant

- Sumitomo Life Insurance — Japan’s #4 life insurer — the third mutual holdout + Symetra US

Want to source Japanese products beyond these company profiles? Japonity also runs a Japan Sourcing Hub — a research-grade catalogue of 1,185 verified Japanese food products and 200+ overseas EC stores, ready for B2B procurement.

Interested in Japanese business opportunities?

Whether you're looking for technology partners, engineering talent, or market insights — we can help connect you with the right Japanese organizations.

Get in Touch →