Mitsui O.S.K. Lines — known throughout the industry simply as MOL, and listed on the Tokyo Stock Exchange under code 9104 — is Japan’s second-largest shipping company by fleet size, sitting between Nippon Yusen (NYK) at number one and Kawasaki Kisen (K Line) at number three. But headline rankings understate what makes MOL strategically distinct. The company operates the world’s largest fleet of liquefied natural gas carriers, with roughly ninety-five LNG vessels in operation or on order as of the mid-2020s — more than any other shipowner globally, and more than NYK and K Line combined. In a decade defined by Europe’s scramble to replace Russian pipeline gas, by the build-out of new LNG export capacity in Qatar and on the United States Gulf Coast, and by Japan’s own dependence on imported LNG for power generation, MOL’s specialisation has become a source of structural earnings rather than a niche. The July 2017 decision to fold the container divisions of MOL, NYK and K Line into a single joint venture — Ocean Network Express, or ONE — simplified MOL’s portfolio in a different way: it removed the most volatile segment from MOL’s standalone balance sheet and let management concentrate capital on the businesses where it actually had a defensible advantage. This is the story of how a 1964 merger between two of Japan’s oldest shipping houses produced, six decades later, an LNG carrier specialist with differentiated exposure to global energy security.

A 1964 merger of two nineteenth-century shipping houses

MOL in its current form dates only to April 1964, when two long-established Japanese shipping companies — Mitsui Steamship Company and Osaka Shosen Kaisha (OSK Line) — merged to form what was then called Mitsui O.S.K. Lines. But the constituent histories reach back to the late nineteenth century, which is why MOL’s official corporate history begins not in 1964 but in 1884, the founding year of OSK.

Osaka Shosen Kaisha was incorporated in May 1884 as a merger of fifty-five smaller shipping operators in the Osaka and Inland Sea region, consolidating a fragmented domestic trade into a single carrier. OSK grew through the late Meiji and Taisho periods into one of Japan’s most internationally oriented shipping companies, building out routes to Korea, Taiwan, China, Southeast Asia and, eventually, the Americas. Mitsui Steamship — the other parent — was spun out of Mitsui Bussan, the trading arm of the Mitsui zaibatsu, in 1942, formalising what had until then been an in-house shipping function. Where OSK’s identity was that of a route operator with deep Pacific trade relationships, Mitsui Steamship was built around the cargo flows of the Mitsui group’s commodity and manufacturing businesses.

The 1964 merger was driven by post-war industrial policy. The Ministry of Transport encouraged consolidation across the shipping sector in the early 1960s to rebuild Japanese-flagged tonnage and restore international competitiveness. Six core groups emerged from that exercise, and today’s MOL — headquartered in Toranomon, Tokyo, with around eight hundred vessels under operation across its consolidated group — is the direct corporate descendant of the Mitsui-OSK combination.

The three-way structure of Japanese shipping

To understand MOL’s position, it helps to map it against its two domestic rivals. Japan’s deep-sea shipping industry is a three-way oligopoly, with each player traceable to a distinct industrial root and each carrying a different segment mix.

| Company | Founded | TSE Code | Approx. Fleet | Distinctive Strength |

|---|---|---|---|---|

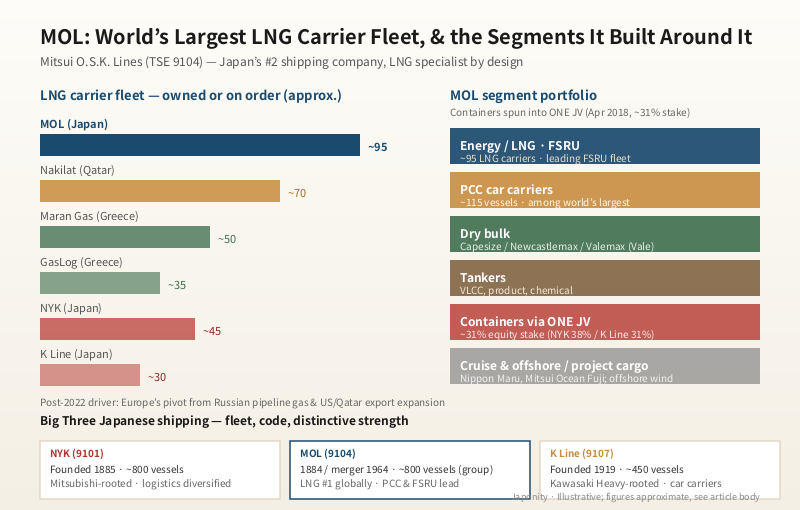

| Nippon Yusen (NYK) | 1885 | 9101 | ~800 vessels | Largest; Mitsubishi-rooted; air cargo & logistics diversification |

| Mitsui O.S.K. Lines (MOL) | 1884 / merger 1964 | 9104 | ~800 vessels (group) | #2 by tonnage; world’s largest LNG carrier fleet; PCC and FSRU specialisation |

| Kawasaki Kisen (K Line) | 1919 | 9107 | ~450 vessels | #3; Kawasaki Heavy-rooted; concentrated in car carriers |

The gap between NYK and MOL is narrower than the gap between MOL and K Line, and on certain measures — notably LNG carrier ownership and FSRU (Floating Storage and Regasification Unit) capacity — MOL leads NYK comfortably. The cultural difference is subtler. NYK, founded out of Mitsubishi, has diversified earliest beyond shipping — air cargo, terminal logistics, supply chain services. MOL has concentrated capital within ocean transport, on the segments where Japanese counterparty relationships and technical operating capability give it a defensible position. LNG is the clearest expression of that strategy.

Why LNG carriers became MOL’s signature business

LNG shipping is not a commodity business in the way that container or dry bulk shipping can become at the spot end of the market. LNG carriers are technically demanding vessels — cryogenic containment, boil-off gas management, membrane or Moss-type tank systems — and the contracts that underwrite them are typically long-term, project-linked, and counterparty-specific. A new LNG export terminal in Qatar or the United States Gulf Coast does not buy carrier capacity from a spot market; it tenders for ten- to twenty-year time charters from a shortlist of shipowners with the balance sheet, operational track record and shipyard relationships to deliver.

MOL entered LNG shipping in the early 1980s, building the first generation of Japanese LNG carriers to serve the trade between Indonesia, Malaysia, Brunei and the Japanese utilities that anchored Japan’s switch from oil-fired to gas-fired power generation. The relationships built in that first decade — with Tokyo Gas, Osaka Gas, the major Japanese power utilities, and with project sponsors in Southeast Asia and Australia — became the foundation on which MOL has compounded the business for forty years. Each new LNG export project worldwide creates carrier demand; MOL’s incumbent operating record and Japanese-keiretsu relationships mean it has consistently won an outsized share of the awarded charters.

By the mid-2020s, the fleet position is the clearest in global shipping: MOL owns or has on order approximately ninety-five LNG carriers, materially more than any other operator. The runners-up — Greek shipowners such as Maran Gas and GasLog, Qatar’s national carrier Nakilat, and NYK — operate fleets in the forty-to-seventy range. The structural demand backdrop is also more favourable than it has been for a generation. Europe’s pivot away from Russian pipeline gas, formalised after February 2022, accelerated long-term LNG contracting; the United States Gulf Coast and Qatar are both building substantial new export capacity through the late 2020s; and Asian importers — Japan, Korea, China, increasingly Vietnam and the Philippines — remain structurally short of domestic gas. Carrier capacity is the binding constraint, and MOL is the largest deliverer of it.

July 2017: the ONE consolidation and the segments that stayed

In October 2016, MOL, NYK and K Line jointly announced that they would combine their container shipping divisions into a single joint venture incorporated in Singapore. Operations began in April 2018 under the name Ocean Network Express, with ownership split roughly thirty-eight percent NYK, thirty-one percent MOL and thirty-one percent K Line. ONE was, at launch, the world’s sixth-largest container operator with approximately two hundred and forty vessels.

For MOL, the ONE consolidation was less existential than it was for K Line — MOL had not been bleeding capital into containers in the same way — but it was strategically clarifying. Container shipping is the most cyclical and most capital-intensive segment in ocean transport, and removing it from MOL’s standalone balance sheet meant that the company’s reported financials would, from 2018 onward, reflect the segments where MOL actually had differentiated capability: LNG, tankers, car carriers, dry bulk, and the project-cargo businesses linked to offshore energy. Container exposure remained — equity-accounted at thirty-one percent of ONE — but it became a line item rather than a defining segment.

The timing turned out to be fortunate. The container super-cycle of 2021 to 2022 delivered unprecedented profits at ONE, which flowed through to MOL’s earnings via equity-method consolidation. In the fiscal year ended March 2022, MOL reported the largest net profit in its history. But unlike at K Line, where the ONE windfall was the dominant story of the cycle, MOL’s standalone segments — particularly car carriers and LNG — were also performing strongly, so the earnings quality was more diversified.

Pure car carriers: the second pillar

Outside LNG, MOL’s most distinctive standalone segment is its pure car and truck carrier fleet, which operates approximately one hundred and fifteen vessels — the largest PCC fleet in the world by hull count, and a fleet that competes with NYK’s affiliate and Norway’s Wallenius Wilhelmsen for the title of largest global operator depending on the measure used.

Car carrier economics differ from containers in important ways. The customer base is concentrated — Toyota, Nissan, Honda, Hyundai, Stellantis, Volkswagen and the Chinese EV exporters account for most volume — contracts are typically multi-year, and the global PCC fleet is structurally tight because vessel orderbooks have lagged the post-pandemic export recovery. When Chinese EV exports surged from roughly one million vehicles in 2022 to over five million by 2024, the immediate constraint was not assembly capacity but seaborne capacity to move the vehicles to Europe, the Middle East and Southeast Asia. PCC charter rates reached historic highs through 2023 and 2024, and MOL’s segment results reflected the move directly.

The strategic question for the PCC segment in the second half of the 2020s is whether new vessels ordered during the 2023 rate peak will arrive in 2026 and 2027 to soften the market. MOL’s approach has been to invest in LNG-fuelled and ammonia-ready PCCs that match decarbonisation requirements at major automotive customers and reduce future regulatory exposure.

Dry bulk, tankers and the FSRU specialty

MOL’s dry bulk business is built around the largest vessel classes — Capesize, Newcastlemax and Valemax — which carry iron ore from Brazil and Australia to steelmaking customers in China, Japan and Korea. The Valemax class, in particular, was developed in partnership with Brazilian miner Vale to carry iron ore on the Brazil-China route at the lowest unit cost in the industry; MOL is one of the principal operators of Valemax vessels under long-term contracts of affreightment with Vale. Newcastlemax and Capesize hulls serve broader Pacific iron ore and coal trades and remain exposed to Chinese steel demand and the Baltic Capesize Index.

The tanker business spans crude oil VLCCs, product carriers and chemical tankers, sized to a customer base anchored in Japanese refiners and major Asian importers. Smaller than the LNG fleet but operationally adjacent, tankers contribute steady cash flow rather than the structural growth that defines the LNG segment.

The most distinctive of MOL’s smaller specialisms is the FSRU business. An FSRU — Floating Storage and Regasification Unit — is essentially an LNG carrier modified to receive imported LNG, regasify it onboard, and feed natural gas directly into an onshore pipeline network. FSRUs allow countries to add gas import capacity in months rather than the years required to build a fixed onshore terminal, and demand for them surged after 2022 as European utilities raced to replace Russian pipeline supply with seaborne LNG. MOL operates one of the largest FSRU fleets globally, with charters to European, South American and South Asian counterparties, and the segment has become a meaningful component of energy-transition revenue.

Cruise, offshore and the adjacencies

MOL’s portfolio extends beyond pure ocean-cargo transport in two further directions. The first is ocean cruise: through its Mitsui O.S.K. Passenger Line subsidiary, MOL operates the Nippon Maru and the new-build Mitsui Ocean Fuji, serving the premium Japanese cruise market. The segment is small in revenue but distinctive — neither NYK nor K Line maintains a comparable passenger business — and gives MOL a consumer-facing brand presence that complements the largely B2B core.

The second is offshore energy and project cargo. MOL participates in the transportation and installation of offshore wind components, in heavy-lift project cargo for petrochemical and infrastructure projects, and in the offshore support vessel market through joint ventures. Together these form an energy-transition portfolio that gives MOL exposure to renewables and gas infrastructure simultaneously — a hedge across the medium-term decarbonisation path that few pure shipping companies can match.

Leadership, governance and the capital-allocation question

MOL is led, as of the mid-2020s, by Chairman Takeshi Hashimoto and President Junichiro Ikeda, with executive succession patterns characteristic of the major Japanese shipping companies — long internal careers, segment rotation through dry bulk, energy and corporate functions, and presidential terms typically running four to six years. The board has progressively added independent directors and English-language investor communication has expanded materially since 2020, reflecting the increased weight of international institutional shareholders on the register.

The capital-allocation question facing MOL in the second half of the 2020s is, in some respects, the inverse of K Line’s. Where K Line spent the 2010s under leverage stress and the early 2020s deleveraging, MOL has emerged from the same period with a balance sheet that is materially stronger and a portfolio that compounds cash flow from LNG, PCC and FSRU contracts on a structural rather than cyclical basis. The question is not whether to invest, but where: in additional LNG newbuilds against the late-2020s export wave, in ammonia and methanol-fuelled vessels for the next decarbonisation cycle, in offshore wind installation capacity, or in returns to shareholders through dividends and buybacks. Management’s stated framework — disciplined fleet renewal, balanced shareholder returns and selective adjacency investment — describes the direction; the specific mix will define MOL’s profile through to 2030.

FAQ

What is Mitsui O.S.K. Lines and how does it rank among Japanese shipping companies?

Mitsui O.S.K. Lines, commonly known as MOL, is Japan’s second-largest shipping company by fleet size and is listed on the Tokyo Stock Exchange under code 9104. It sits between Nippon Yusen (NYK) at number one and Kawasaki Kisen (K Line) at number three. By certain measures — notably LNG carrier ownership and FSRU operations — MOL leads NYK.

When was MOL founded?

MOL in its current form was created in April 1964 through the merger of Mitsui Steamship Company and Osaka Shosen Kaisha (OSK Line). OSK was founded in May 1884, which is the year MOL’s official corporate history takes as its origin. Mitsui Steamship was spun out of Mitsui Bussan in 1942.

Why does MOL operate the world’s largest LNG carrier fleet?

MOL entered LNG shipping in the early 1980s to serve Japanese utility imports from Indonesia, Malaysia, Brunei and Australia, and has compounded that position over four decades through long-term project-linked time charters with global LNG exporters. As of the mid-2020s, MOL owns or has on order approximately ninety-five LNG carriers — materially more than any other shipowner globally.

What is ONE and what is MOL’s stake?

Ocean Network Express (ONE) is a Singapore-incorporated container shipping joint venture launched in April 2018, combining the container divisions of NYK, MOL and K Line. MOL holds approximately thirty-one percent of ONE, accounted for under the equity method. ONE is one of the world’s largest container operators by fleet capacity.

What is an FSRU and why does it matter for MOL?

An FSRU — Floating Storage and Regasification Unit — is an LNG carrier modified to receive, store and regasify LNG offshore, feeding gas directly into onshore pipeline networks. FSRUs allow countries to add gas import capacity in months rather than years, and demand surged after 2022 as European utilities replaced Russian pipeline gas with seaborne LNG. MOL operates one of the largest FSRU fleets in the world.

Working with MOL

For LNG project sponsors, FSRU charterers, automotive exporters, iron ore producers, energy infrastructure developers and logistics partners considering Japanese ocean-freight relationships, MOL offers a counterparty with the world’s largest LNG carrier fleet, one of the world’s largest PCC fleets, leading FSRU capacity and a balance sheet that supports long-tenor commitments. If you are exploring partnerships with Japanese shipping companies — whether for LNG transportation, automotive seaborne logistics, dry bulk contracts of affreightment, FSRU charters or container slots via ONE — Japonity supports international counterparties through our business matching service.

Related from Japonity — Japan’s deep-sea shipping

- NYK Line — Japan’s oldest shipping company and the auto-carrier king

- Kawasaki Kisen (K Line) — Japan’s #3 shipping company and the leverage-restructuring story

Want to source Japanese products beyond these company profiles? Japonity also runs a Japan Sourcing Hub — a research-grade catalogue of 1,185 verified Japanese food products and 200+ overseas EC stores, ready for B2B procurement.

Interested in Japanese business opportunities?

Whether you're looking for technology partners, engineering talent, or market insights — we can help connect you with the right Japanese organizations.

Get in Touch →