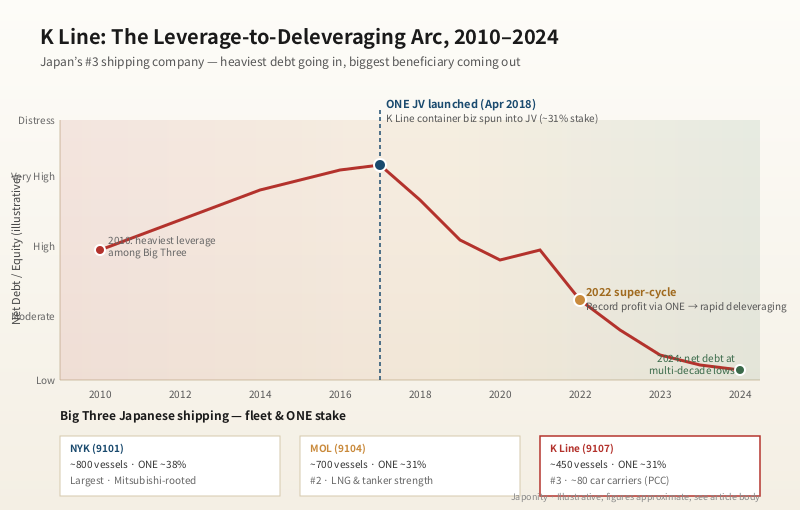

Kawasaki Kisen Kaisha — better known as K Line — is the smallest of Japan’s “Big Three” shipping companies, perpetually trailing Nippon Yusen (NYK) and Mitsui O.S.K. Lines (MOL) in fleet size, revenue, and balance-sheet strength. For most of the 2010s that ranking looked like a slow-motion catastrophe: K Line entered the decade with the heaviest leverage of the three, the thinnest equity cushion, and the most exposure to a container-shipping market that was bleeding cash. Then came July 2017, when the three rivals folded their container divisions into a single joint venture called Ocean Network Express (ONE). K Line took roughly a 31 percent stake — and effectively spun off the business that was eating its capital. What looked like a managed retreat became, by 2022, one of the most remarkable balance-sheet turnarounds in Japanese industrial history. This is the story of how the weakest of the three became, briefly, the most leveraged beneficiary of a once-in-a-generation shipping super-cycle.

A spin-off from Kawasaki Heavy Industries, born in the post-WWI boom

K Line was founded in April 1919 as Kawasaki Kisen Kabushiki Kaisha, a spin-off from the shipbuilding division of Kawasaki Heavy Industries (then Kawasaki Dockyard) in Kobe. The timing was deliberate: Japan’s shipping industry had boomed during the First World War as European fleets were diverted to wartime convoys, and Japanese yards — Kawasaki foremost among them — had a backlog of vessels with no operator. Spinning off a shipping company solved two problems at once: it gave Kawasaki Dockyard a captive customer for its hulls, and it gave the new K Line a fleet at founding scale.

The model — shipbuilder plus shipping operator under common origin — was common in early-20th-century Japan, and it shaped K Line’s identity for the rest of the century. Where NYK grew out of Mitsubishi’s diversified zaibatsu and MOL out of the Mitsui shipping network, K Line was always closer to its engineering parent, with a culture that prized technical operations over financial sophistication. That distinction would matter, decades later, when the industry’s economics shifted from operations to capital allocation.

Headquartered in Toranomon, Tokyo, and listed on the Tokyo Stock Exchange under code 9107, K Line today operates approximately 450 vessels across five segments: containerships (via the ONE joint venture), dry bulk carriers, car carriers (PCCs), energy transportation (LNG and tankers), and logistics. Of those, the segment that defines K Line’s reputation in global trade is its car carrier fleet — roughly 80 pure car and truck carriers — which makes it one of the three largest operators of vehicle-shipping vessels in the world.

The three-way structure of Japanese shipping

To understand K Line’s position, it helps to see the Japanese shipping industry as a three-way oligopoly with clear hierarchy.

| Company | Founded | TSE Code | Approx. Fleet | Position |

|---|---|---|---|---|

| Nippon Yusen (NYK) | 1885 | 9101 | ~800 vessels | Largest; Mitsubishi-rooted; diversified into air cargo and logistics |

| Mitsui O.S.K. Lines (MOL) | 1884 (merger 1964) | 9104 | ~700 vessels | #2; Mitsui-rooted; strongest in LNG and tankers |

| Kawasaki Kisen (K Line) | 1919 | 9107 | ~450 vessels | #3; Kawasaki Heavy-rooted; strongest in car carriers relative to size |

The numerical gap is not the whole story. NYK and MOL both trace their origins to the 1880s and to two of Japan’s largest zaibatsu, which historically gave them deeper relationships with the trading houses, banks, and industrial conglomerates that book most of the cargo. K Line, founded a generation later and tied to a more narrowly engineering-focused parent, has spent its corporate life as the challenger — smaller, more specialised, and structurally more exposed to whichever shipping segment was performing worst at any given moment.

In the 2010s, that segment was containers.

The container problem: why K Line entered the decade with the wrong balance sheet

Container shipping spent most of the 2010s in a state of structural oversupply. Carriers had ordered ultra-large vessels — 18,000 TEU and beyond — in anticipation of continued Chinese export growth, but the post-2008 trade recovery never matched the order book. Spot rates collapsed; the Drewry World Container Index spent years bouncing along break-even or below; and one major carrier, Hanjin Shipping of South Korea, filed for receivership in 2016, stranding cargo around the world.

All three Japanese carriers were exposed, but K Line was the most exposed in relative terms. Its container division accounted for a larger share of revenue than at NYK or MOL, its equity base was thinner, and its debt-to-equity ratio entered the 2010s already at the upper end of the peer group. By the mid-2010s, K Line was reporting consecutive years of operating losses in containers, and the financial markets had begun to price in distress: the share price, which had traded above ¥500 in 2010, fell below ¥200 at points in 2016, and Japanese credit analysts were openly comparing K Line’s leverage profile unfavourably with NYK’s.

The strategic problem was straightforward but politically difficult. None of the three Japanese carriers had the scale, on its own, to compete with the global container giants — Maersk, MSC, CMA CGM, COSCO — whose combined fleets dwarfed any single Japanese operator. But each of the three was also, individually, too proud and too institutionally distinct to surrender its container business to a foreign acquirer. The only consolidation path that preserved Japanese ownership was internal: merge the three container divisions into one.

July 2017: Ocean Network Express and the restructuring that saved K Line

In October 2016, the three companies announced what had been rumoured for years: a binding agreement to combine their container divisions into a new joint venture, to be incorporated in Singapore. The new entity, Ocean Network Express (ONE), began operations in April 2018 after a transition year, with ownership split roughly 38 percent NYK, 31 percent MOL, and 31 percent K Line. The combined fleet — approximately 240 vessels at launch — made ONE the world’s sixth-largest container operator and gave each of the three Japanese parents a stake in a business of globally competitive scale, without any one of them having to fund the consolidation alone.

For K Line, the implications went beyond operational consolidation. By contributing its container business to ONE and accounting for the stake under equity-method consolidation rather than as a wholly owned segment, K Line effectively removed the most capital-intensive and most loss-making part of its balance sheet from its standalone financials. Container vessels, container terminals, and the working-capital intensity that came with global liner operations were all transferred into ONE. K Line’s own balance sheet — leaner, focused on bulk, car carriers, and energy — became immediately more legible to investors.

The first two years of ONE were difficult. The merger integration was slower than projected, ONE reported initial losses, and the share prices of all three Japanese parents drifted. By 2019, ONE had reached operational stability but had not yet demonstrated that the consolidation logic would deliver returns above cost of capital. Then came the pandemic.

The 2022 super-cycle: a leveraged balance sheet becomes an asset

The container-shipping super-cycle of 2021–2022 is now well documented. Supply-chain disruption, container shortages, port congestion, and a surge in goods consumption pushed spot rates on the Shanghai–Los Angeles route from roughly $1,500 per FEU in early 2020 to over $15,000 by mid-2021 — a ten-fold increase. Carriers that had been bleeding cash for a decade suddenly reported profits that exceeded the cumulative losses of the prior cycle. ONE was no exception: in the fiscal year ended March 2022, ONE reported net income of approximately $16.8 billion — a number that, equity-accounted at 31 percent to K Line, flowed through K Line’s P&L as the largest profit in the company’s 100-year history.

For K Line specifically, the timing was extraordinary. The company entered the super-cycle still carrying the leveraged balance sheet of the 2010s — and as the ONE windfall arrived, that leverage worked in reverse. Debt that had looked oppressive in 2018 became trivially serviceable in 2022. K Line used the cash flow to pay down debt aggressively, repurchase shares, and increase dividends to levels not seen in a generation. The share price, which had hovered around ¥200 in 2016 and ¥300 in early 2021, broke through ¥2,500 in 2023 — more than a ten-fold appreciation from the trough.

Of the three Japanese carriers, K Line was the most leveraged going into the cycle, which meant it was the most leveraged beneficiary coming out. NYK and MOL also delivered exceptional results, but neither saw the same percentage transformation in balance-sheet quality, because neither had been as financially stretched at the starting line.

The segments that remained: car carriers, bulk, and LNG

What is sometimes lost in the ONE story is that K Line’s standalone businesses — the segments it kept on its own balance sheet — also performed well, and continue to define the company today.

The car carrier business, with a fleet of approximately 80 pure car and truck carriers (PCCs), is the most distinctive. K Line is one of the three largest global operators of car carriers, alongside NYK’s affiliate and Norway’s Wallenius Wilhelmsen. The economics of car shipping are different from containers: contracts are typically multi-year, customers are concentrated (Toyota, Nissan, Honda, Hyundai, and the European OEMs account for most volume), and the global PCC fleet is structurally tight. When global auto exports recovered post-pandemic and Chinese EV exports began surging in 2023, PCC charter rates reached historic highs — and K Line’s segment results reflected it.

Dry bulk — primarily Capesize vessels carrying iron ore and Panamax carrying coal and grain — remains exposed to the Baltic Dry Index and to Chinese steel demand. The segment is more cyclical than car carriers but less so than containers, and K Line’s bulk fleet is sized for the company’s customer relationships rather than for global market share. Energy transportation, including LNG carriers and crude tankers, is K Line’s smallest core segment; the LNG fleet in particular is materially smaller than MOL’s, reflecting MOL’s historical strength in that segment.

2024 and after: deleveraged, disciplined, and structurally different

By 2024, K Line had completed what investors will likely look back on as one of the cleanest balance-sheet turnarounds in Japanese industrials. Net debt had been reduced to a level the company had not seen since the 1990s; equity ratios had rebuilt to peer-group norms; and the company had executed multiple rounds of share buybacks. President Shotaro Yamashita, who took over from Yukikazu Myochin in 2023, has emphasised continued capital discipline, selective fleet renewal, and a measured approach to the next phase of the cycle.

The strategic questions facing K Line in the second half of the 2020s are different from those of a decade ago. Container rates have normalised — ONE remains profitable but at a fraction of 2022 levels — and the question is whether the combined Japanese carrier is genuinely competitive against the global majors over a full cycle, or only when supply chains break. Car carrier rates are likely to soften as new PCC capacity, much of it ordered during the 2023 highs, comes into the water. Decarbonisation — LNG-fuelled vessels, methanol, ammonia — will require capital expenditure across all segments. And the broader question of how to deploy a now-strong balance sheet, between fleet investment, shareholder returns, and possible adjacencies, is the kind of problem K Line has not faced in two decades.

For Japan’s industrial system, K Line’s recovery matters beyond its own shareholders. Japanese exporters — automotive, machinery, food, electronics — rely on the three-carrier oligopoly for ocean logistics; a financially weak K Line was a strategic vulnerability for the country as much as for the company. A deleveraged K Line, paired with a stable ONE and well-capitalised NYK and MOL, gives Japanese exporters something they did not have in 2016: a Japanese-owned shipping system that can absorb a downturn without forcing emergency consolidation.

FAQ

Why is K Line considered the smallest of the Big Three Japanese shipping companies?

K Line was founded in 1919, roughly a generation after NYK (1885) and MOL (whose constituent companies date to 1884), and it never had the zaibatsu backing that gave NYK and MOL access to Mitsubishi and Mitsui’s global trading networks. By fleet size, K Line operates approximately 450 vessels compared with NYK’s roughly 800 and MOL’s roughly 700.

What is ONE (Ocean Network Express) and what is K Line’s stake?

ONE is a Singapore-incorporated container shipping joint venture launched in April 2018, combining the container divisions of NYK, MOL, and K Line. K Line holds approximately 31 percent of ONE, NYK approximately 38 percent, and MOL approximately 31 percent. ONE is the world’s sixth-largest container operator and is accounted for under the equity method by each of its three Japanese parents.

Why was the 2022 fiscal year so significant for K Line?

The container shipping super-cycle of 2021–2022 produced unprecedented profits at ONE, which flowed through to K Line’s earnings via equity-method consolidation. K Line reported the largest net profit in its 100-year history, used the cash to deleverage aggressively, and the share price appreciated roughly ten-fold from its 2016 trough.

What segments does K Line operate outside of containers?

K Line’s standalone segments are dry bulk (Capesize and Panamax), car carriers (approximately 80 PCC vessels — one of the three largest global PCC fleets), energy transportation (LNG carriers and tankers), and logistics. Container operations are conducted through the ONE joint venture rather than on K Line’s standalone balance sheet.

Where is K Line headquartered and how can it be accessed publicly?

K Line is headquartered in Toranomon, Tokyo, and is listed on the Tokyo Stock Exchange Prime Market under code 9107. The company publishes English-language investor disclosures, including annual reports, integrated reports, and segment-level financial data, on its corporate website.

Working with K Line

For exporters, OEMs, energy developers, and logistics partners considering Japanese ocean-freight relationships — whether for car carrier capacity, LNG transportation, bulk commodities, or container slots via ONE — K Line offers a counterparty whose balance sheet, after the 2022–2024 deleveraging, is structurally stronger than at any point in the past two decades. If you are exploring partnerships with Japanese shipping companies or need an introduction to the relevant K Line business unit, Japonity supports international counterparties through our business matching service.

Related from Japonity — Japan’s deep-sea shipping

- NYK Line — Japan’s oldest shipping company and the auto-carrier king

- Mitsui O.S.K. Lines (MOL) — Japan’s #2 shipping company and the world’s largest LNG carrier fleet

Want to source Japanese products beyond these company profiles? Japonity also runs a Japan Sourcing Hub — a research-grade catalogue of 1,185 verified Japanese food products and 200+ overseas EC stores, ready for B2B procurement.

Interested in Japanese business opportunities?

Whether you're looking for technology partners, engineering talent, or market insights — we can help connect you with the right Japanese organizations.

Get in Touch →