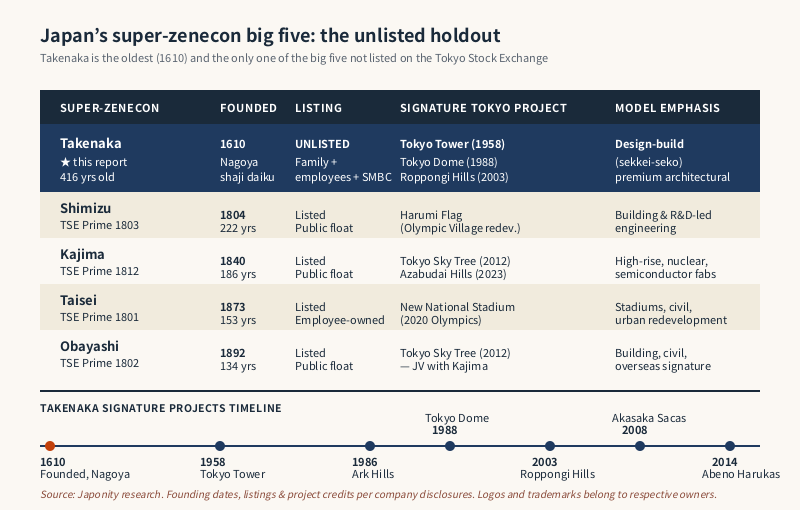

Of the five firms Japanese clients, regulators and lenders call the super-zenecon — the general contractors with the balance sheet and engineering depth to deliver Japan’s tallest, most seismically demanding and most politically sensitive structures — Takenaka Corporation (株式会社竹中工務店) is the strangest member of the cluster, and the one foreign analysts misread most often. It is the oldest, founded in 1610 in Nagoya by Tobei Takenaka I as a temple-carpenter shop a generation before Edo became the shogunal capital. It is the only one not listed on the Tokyo Stock Exchange — uniquely among the big five, Takenaka remains roughly four hundred years on entirely in private hands, held by the founding family, by employee shareholders, and by a small group of long-relationship corporate and banking shareholders. And its business model still runs on sekkei-seko, the integrated design-build approach in which architecture, structural engineering and on-site construction are handled inside the same firm rather than fragmented across separate designers, contractors and subcontractors as in the Western model. For foreign developers reading the Tokyo redevelopment cycle, Takenaka is the contractor behind Tokyo Tower (1958), the Tokyo Dome (1988), Roppongi Hills Mori Tower (2003), Ark Hills, Akasaka Sacas and a long list of museums, university campuses and corporate headquarters — and one of the few major Japanese firms of any sector that has resisted the listed-company governance template for the entirety of the postwar era.

From a 1610 temple-carpenter shop to a super-zenecon

The founding story is unusually well-documented because Takenaka, like a number of long-lived Japanese houses, kept lineage records. Tobei Takenaka I opened the original workshop in Nagoya in 1610, focused on shaji — shrine and temple — construction, a category that in early Edo Japan was the most technically demanding kind of building work available. Temple carpentry required mastery of complex timber joinery, large-span roof structures, and decorative woodwork executed without standardised dimensions or modern tools; the trade carried apprenticeship lineages comparable to those of European cathedral masons. The Takenaka shop survived the transitions that ended most early-Edo trades: the late-shogunate political collapse, Meiji-era industrialisation, and the shift from wood to steel and reinforced concrete that reorganised Japanese construction between 1880 and 1920.

The decisive move into modern building came under the fourteenth-generation head, Tobei Takenaka XIV, who in 1899 reorganised the family business as a modern construction firm and relocated operating headquarters to Kobe, then one of Japan’s most cosmopolitan trading cities. The firm was formally incorporated in 1937 as Takenaka Komuten Co., Ltd. — the name it still uses — and grew rapidly through postwar reconstruction, the high-growth decades and the long redevelopment cycle that has reshaped central Tokyo since the early 2000s. Corporate headquarters today is in Tokyo, with major offices in Osaka, Nagoya and Kobe and overseas subsidiaries across the United States, Europe, Southeast Asia and China. Group revenue is approximately ¥1.5 trillion or more in recent years, placing Takenaka among the top three or four super-zenecon by revenue depending on project mix in any given year.

The super-zenecon big five and Takenaka’s listing anomaly

The five firms differ in heritage, ownership and emphasis, but they cluster tightly enough on scale and capability that Japanese procurement treats them as a peer group. Four are listed on the Tokyo Stock Exchange’s Prime Market. Takenaka is the lone holdout — and the gap is not incidental. The table below sketches the comparison.

| Super-zenecon | Founded | Listing | Ownership structure | Signature Tokyo project |

|---|---|---|---|---|

| Takenaka Corporation | 1610 | Unlisted | Takenaka family, employees, banks (private) | Tokyo Tower (1958), Tokyo Dome (1988), Roppongi Hills Mori Tower (2003) |

| Shimizu Corporation | 1804 | TSE Prime (1803) | Public float, founding-family minority | Harumi Flag (Olympic Village redev.) |

| Kajima Corporation | 1840 | TSE Prime (1812) | Public float, founding-family minority | Tokyo Sky Tree (JV), Azabudai Hills |

| Taisei Corporation | 1873 | TSE Prime (1801) | Public float, large employee holding | New National Stadium (2020 Olympics) |

| Obayashi Corporation | 1892 | TSE Prime (1802) | Public float | Tokyo Sky Tree (JV with Kajima) |

The cluster has no real parallel in another developed economy. American construction is fragmented between regional builders and pure construction managers; European peers — Bouygues, Vinci, Hochtief, Skanska — dominate national markets but rarely match the in-house engineering breadth of a Japanese super-zenecon, which keeps architectural, structural, mechanical and civil engineering under one roof. Inside the cluster, Takenaka’s distinguishing feature is not size — Kajima and Obayashi are larger by group revenue in most recent years — but the combination of three traits: the oldest continuous lineage, the only unlisted ownership structure, and the most explicitly design-led business model.

The unlisted status is the trait that most surprises foreign observers. Japan’s listed-company population is unusually broad, and a contractor of Takenaka’s revenue scale would, in nearly any other country, be a public company by default. Takenaka has consciously stayed private. The shareholder register is dominated by the Takenaka family, by an employee shareholding association that holds a substantial bloc through internal stock plans, and by long-relationship corporate and banking shareholders — primarily Sumitomo Mitsui Banking Corporation, Mitsui Sumitomo Insurance and other firms inside the Sumitomo Mitsui Financial Group orbit. There is no public float. The firm’s annual reports and disclosures are produced to a standard comparable to its listed peers, but distribution is to lenders and customers rather than to capital markets.

Two reasons are usually cited for the private posture. The first is generational continuity: a private structure makes it materially easier to preserve a multi-generation family identity, a long capital-allocation horizon and a culture organised around craftsmanship rather than quarterly earnings. The second is the design-build model itself. Takenaka’s competitive identity rests on integrating architectural design with construction execution — a model that is difficult to defend under public-market pressure to break out higher-margin design services from lower-margin contract construction. Private ownership lets the firm hold the integrated model together when listed peers would face investor calls to spin out design subsidiaries.

Sekkei-seko: why the design-build model matters

In most Western large-project construction, design and construction are separated. An owner commissions an architect — typically a stand-alone firm such as SOM, Foster + Partners or Kohn Pedersen Fox — to produce a design, then tenders the construction contract to a general contractor or construction manager, who in turn lets subcontracts to specialty trades. The model emphasises owner-side control and competitive pricing on the build phase, but splits design intent from build execution and pushes risk to interfaces between firms.

The Japanese super-zenecon model is partly integrated by default — each of the big five carries significant in-house architectural and engineering staff — but Takenaka pushes the integration further than its peers. Its in-house design organisation, Takenaka Sekkei-bu, is one of the largest architectural practices in Japan by registered architect headcount, comparable in scale to standalone firms such as Nikken Sekkei. It operates as a near-autonomous studio with senior architects whose names appear on landmark buildings in the way Western practice would expect of a partner-architect at an independent firm. Structural, mechanical and façade engineering report into adjacent technical departments in the same legal entity, and the construction division executes the design with the design team retained through completion.

The model has several practical consequences. Design intent is preserved more reliably through value-engineering and procurement, because the same firm is responsible for both. Innovations in materials, joints, structural systems and façades can be developed in-house and trialled on real projects without commercial negotiation between separate firms. Project-management risk is internalised: when interface problems appear between, say, a complex curtain wall and the structural frame, the resolution does not require a contract negotiation between architect and contractor.

The trade-offs are real. Design-build is harder to scale when pipelines are concentrated in a single firm, and clients seeking the lowest construction bid will sometimes prefer separate-contract structures. Takenaka’s response has been to keep the practice focused on premium architectural categories — corporate headquarters, museums, cultural facilities, premium office towers, stadium and dome structures — where the integrated model is most clearly valued.

The Tokyo signature portfolio: Tower, Dome, Roppongi Hills

Takenaka’s footprint on the visible Tokyo skyline is denser than most foreign observers realise. Three projects in particular anchor its public profile.

Tokyo Tower, completed in 1958 at 333 metres, was the tallest free-standing structure in Japan for more than half a century and the visual icon of postwar Tokyo until the Sky Tree opened in 2012. The tower’s distinctive lattice form was designed by structural engineer Tachū Naitō, with construction led by Takenaka — a project that combined the firm’s reinforced-concrete foundation experience with steel-erection capability developed during the 1950s reconstruction. Its continued operation as a broadcasting transmitter and tourist landmark seven decades on remains a working monument to mid-century Japanese construction engineering.

The Tokyo Dome, completed in 1988 in Bunkyo Ward, was the first air-supported domed stadium in Japan and one of the largest of its kind in the world at the time. It serves as the home stadium of the Yomiuri Giants and as the principal indoor venue for large-scale concerts, conferences and trade shows in Tokyo. The membrane-roof structural system, the air-pressure mechanical plant and the integration with adjacent hotel, amusement park and retail facilities made the project a 1980s engineering showcase, and it remains a reference for large-span enclosed-arena work.

Roppongi Hills Mori Tower, completed in 2003 at 238 metres, anchors Mori Building’s flagship Roppongi redevelopment and was for a time among the tallest office towers in Tokyo. Takenaka delivered the tower as part of a vertically integrated complex that included residential towers, the Mori Art Museum on the upper floors, a hotel, retail concourses and complex podium-level transit and public-realm infrastructure. The project helped define the template for the large-floorplate, premium-grade central Tokyo office tower category that would dominate twenty years of subsequent Mori, Mitsubishi Estate, Mitsui Fudosan and Tokyu redevelopment.

Around these flagships sits a long list of further credits: Ark Hills (1986), the first large-scale private-sector central-Tokyo redevelopment, anchored by ANA Intercontinental and Suntory Hall; Akasaka Sacas (2008), the TBS Holdings broadcasting and retail complex; long-running renovation and seismic-strengthening of Hanshin Koshien Stadium; Abeno Harukas (Osaka, 2014), for a time Japan’s tallest skyscraper; corporate headquarters for large industrial and telecoms clients; and museums and cultural facilities from the National Art Center, Tokyo, to a long tail of regional museums and university buildings. The pattern is consistent: premium-segment architectural buildings in which the integrated design-build model is a competitive advantage rather than a marginal feature.

Ownership, governance and family lineage

The Takenaka family has held the head-of-house role across the entire history of the firm. The presidency in recent years has been held by Toichi Takenaka, a member of the founding family, who has emphasised the integrated design-build model, the firm’s craftsmanship lineage and the digital-engineering and decarbonisation agendas the contractor needs to defend over the next decade. The leadership style is consistent with the cultural register foreign observers expect from a long-tenured Japanese family firm: low public profile, internal continuity, engineering-first executive backgrounds, decisions taken on long horizons.

The governance structure differs from a listed peer in several ways that matter for foreign counterparties. Capital allocation is decided internally rather than negotiated with public shareholders, which gives the firm room to invest in long-payback design and research initiatives — the firm’s R&D centre in Chiba develops anti-seismic systems, automated construction equipment and digital-twin platforms — without the quarterly pressure that listed peers face. The firm’s strategic horizon, particularly on lineage commitments such as historical preservation, temple and shrine work, and long-relationship corporate-headquarters clients, runs longer than a typical listed-company strategic plan.

The risks of the private structure are real. The firm cannot raise primary equity from public markets in the way listed peers can; succession depends on the depth and continuity of the family and senior-employee bench; and external scrutiny is filtered through long-relationship banks, customers and employees rather than through public-market analysts. So far the trade-off has favoured continuity, but the model would be tested in a sharper downturn.

What comes next

The Tokyo redevelopment cycle still has visible runway. Mori Building, Mitsubishi Estate, Mitsui Fudosan and Tokyu have multi-decade master plans for Toranomon, Yaesu, Shibuya and Shinagawa that imply continued super-zenecon capacity demand at least through the late 2030s, and Takenaka’s premium-architectural positioning aligns well with the trophy-office and mixed-use categories that dominate that pipeline. Adjacent demand pockets are visible too: semiconductor and pharmaceutical facilities, stadium and arena renovation, university and museum expansions, and a steady current of corporate-headquarters consolidations as Japanese listed firms reorganise around hybrid work and ESG-aligned standards.

The firm is also leaning into digital design and automation. Generative-design tools, robotic site equipment, modular and prefabricated construction, and digital-twin operations platforms are all visible in Takenaka’s R&D publications. The decarbonisation agenda — low-embodied-carbon concrete, mass-timber construction for medium-rise buildings, on-site renewable energy integration — is a category where the integrated design-build model is well-positioned to deliver, because the trade-offs sit across architectural, structural and mechanical disciplines that fragmented teams would have to renegotiate.

For foreign developers, infrastructure investors and corporate occupiers approaching the Japanese market, Takenaka is a different counterparty from its listed peers. The firm cannot be reached through equity-market channels, the disclosure cadence is private, and the engagement model is built on long-relationship trust rather than competitive bidding cycles. That is a deliberate posture, and it is the structural reason the firm has been able to defend its design-led, integrated, family-anchored model into a fifth century.

FAQ

When was Takenaka Corporation founded, and what was its original business?

Takenaka was founded in 1610 in Nagoya by Tobei Takenaka I as a temple-carpenter shop (shaji daiku), specialising in shrine and temple construction. The business was reorganised as a modern construction firm in 1899 under the fourteenth-generation head and was formally incorporated in 1937 as Takenaka Komuten Co., Ltd. It is the oldest of Japan’s five super-general-contractors by founding date and operates today from a Tokyo headquarters with major offices in Osaka, Nagoya and Kobe.

Why is Takenaka the only super-zenecon not listed on the stock exchange?

Takenaka is approximately one hundred percent privately held — by the Takenaka founding family, by an employee shareholding association, and by a small group of long-relationship corporate and banking shareholders primarily inside the Sumitomo Mitsui Financial Group orbit. The private structure is a deliberate posture, designed to preserve a multi-generation family identity, a long capital-allocation horizon and the integrated design-build business model, all of which would be harder to defend under public-market pressure to maximise short-term return or to spin out higher-margin design services from the contract-construction business.

What is the “design-build” model and how does it differ from Western construction?

Design-build (sekkei-seko) is an integrated model in which architectural design, structural and mechanical engineering, and on-site construction are handled inside the same firm. In the Western fragmented model the owner commissions an architect, then separately tenders the construction contract, then lets subcontracts to specialty trades. Takenaka’s in-house design organisation (Takenaka Sekkei-bu) is one of the largest architectural practices in Japan by registered architect headcount, and the firm retains the design team through construction completion. The integrated model preserves design intent through value-engineering and procurement, internalises interface risk, and supports long-payback R&D in materials, structural systems and façades.

Which signature Tokyo projects has Takenaka delivered?

Takenaka’s Tokyo flagship credits include Tokyo Tower (1958, design by structural engineer Tachū Naitō and construction by Takenaka), the Tokyo Dome (1988, the first air-supported domed stadium in Japan), Roppongi Hills Mori Tower (2003, the 238-metre office tower anchoring Mori Building’s flagship Roppongi redevelopment), Ark Hills (1986), Akasaka Sacas (2008) and a long list of corporate headquarters, museums and university buildings. Outside Tokyo, signature work includes Abeno Harukas in Osaka and continuing renovation of Hanshin Koshien Stadium, the home of Japanese professional and high-school baseball.

How does Takenaka compare in size and segment focus to the other super-zenecon?

Takenaka’s group revenue is approximately ¥1.5 trillion or more in recent years, placing it among the top three or four super-zenecon by revenue depending on project mix in any given year — Kajima and Obayashi are typically larger by reported group revenue, with Taisei and Shimizu broadly comparable. Takenaka’s segment mix is more weighted toward premium-architectural building construction — corporate headquarters, museums, cultural facilities, premium office towers, stadium and dome structures — than toward civil engineering or nuclear work, where Kajima, Obayashi and Taisei carry larger franchises. The firm’s overseas business is concentrated in the United States, Europe, Southeast Asia and China through wholly-owned subsidiaries.

Working with Takenaka

For overseas developers, infrastructure investors, corporate occupiers and cultural-facility owners planning major architectural or premium-building programmes in Japan, the super-zenecon — and Takenaka in particular, given its design-build integration, premium-architectural credentials and long-relationship counterparty profile — are essential partners. Engagement with a private firm of Takenaka’s profile typically begins through long-relationship banks, professional networks or peer client introductions rather than through equity-market channels. Japonity introduces qualified overseas companies to Japanese general contractors, real estate developers, architectural design houses and infrastructure operators through its business matching service. If you are exploring a Japan-market headquarters build, a museum or cultural facility, a stadium or arena project, a corporate redevelopment or a co-investment alongside a super-zenecon, get in touch to start a conversation.

Related from Japonity — Japan’s super-general contractors (zenecon)

- Kajima Corporation — Japan’s super-zenecon — Tokyo Sky Tree, Azabudai Hills, TSMC Kumamoto

- Obayashi Corporation — The 1892 super-zenecon — Tokyo Sky Tree, Marina Bay Sands, Burj Khalifa

- Taisei Corporation — Employee-owned super-zenecon — Tokyo Olympic Stadium, Esconfield

- Shimizu Corporation — The 1804 super-zenecon — Tokyo Sky Tree, Akashi-Kaikyo, Lunar Ring

Want to source Japanese products beyond these company profiles? Japonity also runs a Japan Sourcing Hub — a research-grade catalogue of 1,185 verified Japanese food products and 200+ overseas EC stores, ready for B2B procurement.

Interested in Japanese business opportunities?

Whether you're looking for technology partners, engineering talent, or market insights — we can help connect you with the right Japanese organizations.

Get in Touch →