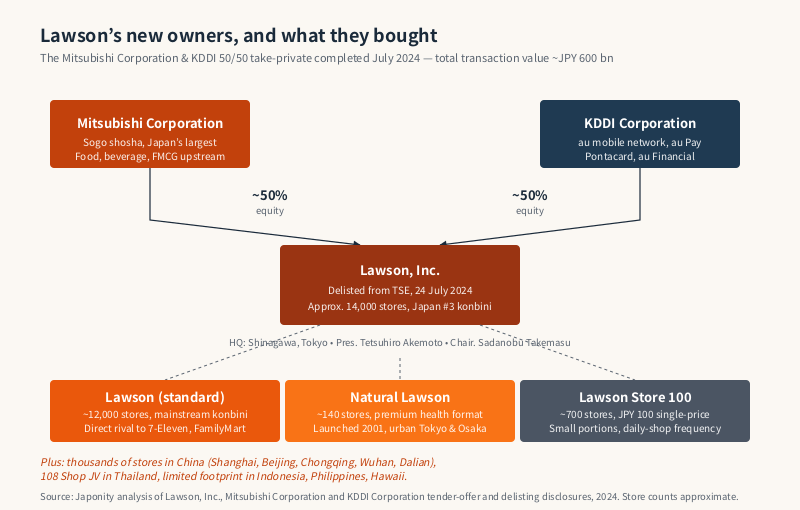

On 24 July 2024, Lawson, Inc. delisted from the Tokyo Stock Exchange after more than fifty years on the market, and Japan’s third-largest convenience-store chain became the joint property of two companies that, a generation earlier, would have struck most observers as an unlikely pairing — Mitsubishi Corporation, the country’s largest sogo shosha, and KDDI, its second-largest mobile telecommunications carrier. Each now holds roughly fifty per cent of Lawson’s equity following a tender offer and squeeze-out completed for an approximate total transaction value of six hundred billion yen. The chain itself operates approximately fourteen thousand stores across Japan, sits behind Seven-Eleven Japan and FamilyMart in the konbini league table, and runs the most format-diverse store portfolio of any major Japanese convenience operator — from the standard blue-and-white Lawson, to the premium health-conscious Natural Lawson, to the hundred-yen Lawson Store 100. The take-private was not a defensive move. It was a deliberate bet that a convenience store, in the hands of a trading house and a telco rather than a public shareholder base, can be turned into something Japanese retail has not yet seen — a tightly integrated physical-and-digital platform sitting at the intersection of FMCG, financial services, mobility and last-mile logistics. Whether the bet pays off will reshape what foreign suppliers, brand owners and investors think a Japanese konbini is for.

From an Ohio dairy to a Tokyo konbini chain

The Lawson brand was not born in Japan. It traces its origin to 1939, when James J. Lawson, a dairyman in Cuyahoga Falls, Ohio, opened the J.J. Lawson Milk Company to sell fresh milk through small storefronts in the American Midwest. The format expanded through the 1950s and 1960s into a regional chain of dairy-anchored convenience stores, eventually absorbed by Consolidated Foods and later sold on, with the original American Lawson chain effectively disappearing from the United States in the 1980s. By that point, however, the brand had already crossed the Pacific.

The bridge was Daiei, the now-defunct Japanese supermarket pioneer that, in the early 1970s, was scouting American retail formats it could license into Japan. Daiei opened the first Japanese Lawson store in Toyonaka, Osaka Prefecture, in 1975. The fit was excellent: Japan’s urban density, long working hours, small apartments and rising number of single-person households made a small neighbourhood store carrying daily essentials extraordinarily well suited to Japanese life. Lawson grew rapidly through the 1980s and 1990s as a Daiei subsidiary, learning, alongside Seven-Eleven Japan and FamilyMart, how to operate the high-frequency, low-ticket economics that define the Japanese konbini.

The pivotal corporate event was Daiei’s slow-motion financial collapse around the turn of the millennium. Mitsubishi Corporation acquired Daiei’s controlling stake in Lawson in February 2001, becoming the company’s largest single shareholder. The sogo shosha’s involvement was strategic from the outset: Lawson gave Mitsubishi a guaranteed downstream channel for the foods, beverages and FMCG products flowing through its upstream supply chains. The chain’s headquarters moved to Shinagawa in central Tokyo, and a sequence of professional chief executives — Takeshi Niinami, then Sadanobu Takemasu — pushed Lawson through two decades of format experimentation and selective overseas expansion. Niinami left to run Suntory in 2014. Takemasu became CEO in 2017 and is now chairman; Tetsuhiro Akemoto took the president role in 2023 ahead of the take-private.

The format zoo, konbini edition

One reason Lawson is the most strategically interesting of the three major Japanese convenience chains is that it runs the widest portfolio of store formats. Seven-Eleven Japan operates essentially one store concept, executed with exceptional discipline. FamilyMart is also largely single-format. Lawson, by contrast, deliberately maintains a three-format domestic footprint, plus an overseas network, that allows it to address segments of the Japanese consumer market the other two do not directly cover.

| Format | Concept | Approximate stores | Positioning |

|---|---|---|---|

| Lawson (standard) | Mainstream konbini: bento, drinks, snacks, household essentials, ATMs, ticketing, parcel services | Approximately 12,000-plus stores in Japan | Direct competitor to 7-Eleven and FamilyMart on the main konbini battleground |

| Natural Lawson | Premium health-conscious format: organic and additive-conscious foods, natural cosmetics, wellness products | Approximately 140 stores, urban Japan | Targets affluent women, white-collar workers in central Tokyo and Osaka |

| Lawson Store 100 | Hundred-yen format: small-portion fresh produce, prepared foods and household basics at a single price point | Approximately 700 stores | Frequency-driven daily-shop for single-person households and price-sensitive shoppers |

| Lawson China | Standard konbini adapted for Chinese cities | Several thousand stores across Shanghai, Beijing, Chongqing, Wuhan, Dalian and other cities | Largest foreign konbini chain in China by store count |

| 108 Shop (Thailand JV) | Convenience format operated through joint venture with Saha Group | Hundreds of stores in Thailand | Southeast Asian beachhead under a localised brand |

| Lawson Indonesia, Philippines, Hawaii | Standard and adapted formats in selected markets | Limited footprint | Experimental or partner-led overseas presence |

The three Japanese formats are not nostalgic legacy holdouts. Natural Lawson, launched in 2001, was an early bet that health-conscious urban consumers would pay a premium for organic produce, additive-light prepared foods and well-curated cosmetics inside a convenience-store footprint — a thesis that has since become mainstream globally but which Lawson reached unusually early. Lawson Store 100 addresses the opposite end of the market: budget-conscious shoppers, single-person households and the elderly who want small portions of fresh food at a single transparent price point. Together they let Lawson cover a consumer span — from the Aoyama professional buying organic miso to the suburban pensioner buying a hundred-yen banana — that single-format competitors cannot match in one corporate envelope.

The three-way konbini contest

The Japanese convenience-store market is, by global standards, mature, dense, slow-growing and dominated by three operators. Seven-Eleven Japan, owned by Seven & i Holdings, runs more than twenty thousand domestic stores, is the most operationally productive of the three on a per-store basis and anchors a global 7-Eleven network through Seven-Eleven, Inc. in the United States. FamilyMart, taken private by Itochu Corporation in 2020, runs roughly sixteen thousand domestic stores and is leveraging Itochu’s trading-house supply chain in a manner conceptually similar to what Mitsubishi has been doing with Lawson, but with a longer head start as a wholly trading-house-owned business.

Lawson, with approximately fourteen thousand domestic stores, sits in third place by store count and revenue. The three operators together define the category; smaller chains such as MiniStop within the Aeon group and Hokkaido’s Seicomart do not threaten them on any meaningful national basis. The competitive question for Lawson is not whether it can take share from the smaller players. It is whether it can close the operational and digital gap with 7-Eleven and FamilyMart, or differentiate so distinctly that closing the gap is no longer the right metric.

Why Mitsubishi and KDDI bought it

The take-private announced in February 2024 and completed in July 2024 was structured as a tender offer led by Mitsubishi in coordination with KDDI. KDDI acquired roughly half of the equity from Mitsubishi and other shareholders, leaving the two companies each holding approximately fifty per cent and serving as joint controlling shareholders. The total transaction value across the tender offer and subsequent squeeze-out came to approximately six hundred billion yen.

For Mitsubishi, the logic was deepening. The trading house had been Lawson’s largest shareholder for more than two decades, and full ownership removes the public-market constraints that limit how aggressively the chain can be repurposed as a downstream channel for Mitsubishi’s food, beverage, materials and energy businesses. For KDDI, the rationale is more novel and arguably more interesting. KDDI runs au, one of Japan’s three nationwide mobile networks; au Pay, a QR-code mobile payment system; au Financial Holdings, a banking and consumer-finance arm; and Pontacard, a major loyalty programme already partnered with Lawson. KDDI’s bet is that a network of fourteen thousand physical stores can become the physical anchor of a fully integrated digital-physical retail platform. Pontacard already links the two companies’ customer bases. Au Pay can be the primary payment rail. Au Financial products can be cross-sold at the counter. Parcel pickup, used-goods drop-off, electric-vehicle charging, mobile-contract activation and quasi-pharmacy services can all be layered onto the konbini footprint.

The implicit thesis is that the konbini, in Japan, is no longer just a small-format store. It is a piece of public infrastructure embedded in every neighbourhood, and the company that knits the physical network together with a mobile network, a payment rail, a loyalty programme and a financial-services stack will own a category of consumer relationship that neither pure retail nor pure telecoms can deliver alone.

The Asia footprint and the China question

Outside Japan, Lawson runs the largest convenience-store footprint of any Japanese chain in China, with several thousand stores across Shanghai, Beijing, Chongqing, Wuhan, Dalian and other cities. The Chinese business is operated through a mix of wholly owned regional subsidiaries and joint ventures, and has been a multi-decade exercise in patient localisation against increasingly competitive domestic chains such as Meiyijia and Imai Convenience.

Competitive intensity has risen sharply in recent years. Chinese consumer behaviour has moved aggressively toward instant grocery delivery, community group buying and super-app integration, all of which compress the differentiation a foreign-branded fresh-food konbini can offer. Lawson China has nonetheless continued to grow store counts and has, in some city clusters, become the dominant modern-trade convenience operator. Whether the China business is a long-term growth engine or a position that will be rationalised down to its strongest cities is one of the open questions Mitsubishi and KDDI now own outright.

The Southeast Asian footprint is smaller but commercially interesting. In Thailand, Lawson operates through a joint venture with Saha Group under the localised brand 108 Shop, with hundreds of stores concentrated in Bangkok and provincial cities. Indonesia, the Philippines and Hawaii each host a limited number of stores under partner-led or experimental formats. None rivals the scale of the Japanese or Chinese operations, but they preserve optionality and serve as test beds for what a Japanese konbini concept looks like when transplanted into markets at different stages of modern-trade development.

Private brands and the trading-house supply chain

One of the most consequential effects of Mitsubishi’s two-decade control of Lawson has been the steady build-out of private-label product flowing through the konbini network. Lawson’s own private brands — including Lawson Select and Machi no Lawson — span prepared foods, beverages, baked goods, snacks and household basics, and account for a meaningful share of in-store sales. The supply chain behind these brands runs through Mitsubishi’s food and beverage trading affiliates and a network of contract manufacturers, many of them longstanding trading-house counterparties.

For foreign FMCG suppliers — coffee roasters, snack manufacturers, dairy processors, ready-meal producers, cosmetic brands and beverage exporters — Lawson is therefore not a one-door entry into Japan but a multi-door system. A product can enter through a direct supplier contract with Lawson Merchandising, be co-developed as a private-label item using Mitsubishi-sourced raw materials, be sold through Natural Lawson as a premium niche product before scaling to standard Lawson, or be tested in Lawson China or 108 Shop Thailand as a pre-Japan beachhead. The take-private does not change those entry points fundamentally, but it does mean that decisions on which products get scaled and which formats receive investment will be made inside a private corporate structure, on a longer time horizon than a quarterly-listed company can typically tolerate.

Governance after delisting

Sadanobu Takemasu, chief executive from 2017, moved to chairman around the take-private, and Tetsuhiro Akemoto took over as president from 2023. The post-delisting board reflects the joint ownership, with representation from both Mitsubishi and KDDI and operational management remaining with Lawson’s executive team in Shinagawa. The reporting cadence and disclosure burden have both fallen substantially with the move off the Tokyo Stock Exchange, freeing the company to invest in store renovations, digital integration with au Pay and Pontacard, and format experimentation without quarterly earnings-call commentary.

The governance arrangement is unusual by Japanese standards. Joint fifty-fifty ownership across a sogo shosha and a telco, with neither shareholder dominant, requires careful coordination on strategic decisions and capital allocation. The closest precedent is Itochu’s wholly owned control of FamilyMart, but the Mitsubishi-KDDI structure adds a layer of cross-industry alignment — and potential friction — the simpler Itochu-FamilyMart model does not have. Whether the dual-shareholder structure proves a source of strategic creativity or strategic deadlock will be one of the more closely watched questions in Japanese retail through the rest of the decade.

What it means for foreign suppliers and partners

For overseas brands, three implications follow. First, longer time horizons: a privately held Lawson can support category investments and supplier partnerships a public konbini chain might pull back from under quarterly margin pressure. Second, deeper digital integration: suppliers whose products are integrated into the au-Pay-and-Pontacard loyalty stack — through mobile coupons, app-driven campaigns — will see disproportionate visibility. Third, broader format options: a brand whose positioning fits Natural Lawson can enter there without clearing standard-format scale hurdles, then scale up if early traction supports it.

The risks are equally real. Private ownership means less public reporting and slower formal decision processes. Joint fifty-fifty governance means strategic shifts can be slow when Mitsubishi and KDDI disagree. And the chain remains the third player in a category dominated, operationally, by 7-Eleven. None of those are reasons to avoid Lawson as a partner — but they are reasons to understand the corporate structure carefully before committing to a category strategy that depends on it.

FAQ

Who owns Lawson, Inc. now?

Following the take-private completed on 24 July 2024, Lawson is jointly owned by Mitsubishi Corporation and KDDI Corporation, each holding approximately fifty per cent of the equity. The total transaction value of the tender offer and subsequent squeeze-out came to approximately six hundred billion yen. Lawson is no longer listed on the Tokyo Stock Exchange. Operational management remains based at the company’s Shinagawa headquarters in Tokyo, with Tetsuhiro Akemoto as president and Sadanobu Takemasu as chairman.

How many Lawson stores are there in Japan and overseas?

Lawson operates approximately fourteen thousand stores in Japan across three formats — the standard Lawson, the premium Natural Lawson (around 140 stores) and the hundred-yen Lawson Store 100 (around 700 stores). Outside Japan, the company runs several thousand stores in China across Shanghai, Beijing, Chongqing, Wuhan, Dalian and other cities; hundreds of stores in Thailand under the 108 Shop joint venture with Saha Group; and smaller footprints in Indonesia, the Philippines and Hawaii. Lawson China is the largest Japanese-brand convenience-store operator in China by store count.

How is Lawson different from 7-Eleven Japan and FamilyMart?

Lawson is the smallest of the three majors by store count and revenue but runs the widest portfolio of store formats. Seven-Eleven Japan and FamilyMart each essentially operate one standard konbini format, executed with operational discipline and supply-chain scale. Lawson runs three distinct formats — standard, Natural Lawson and Lawson Store 100 — alongside its overseas business, which means it covers premium health-conscious shoppers and price-sensitive single-portion shoppers that the other two do not directly target. The trade-off is generally lower per-store productivity than 7-Eleven Japan.

What is Natural Lawson?

Natural Lawson is Lawson’s premium health-conscious format, launched in 2001 and operating approximately 140 stores concentrated in central Tokyo and Osaka. Its assortment emphasises organic and additive-conscious foods, natural cosmetics, wellness products, gluten-conscious bakery and prepared meals with cleaner ingredient panels than standard convenience-store fare. The format targets affluent urban women, professionals and health-aware shoppers. For overseas brands in organic food, natural cosmetics or wellness, Natural Lawson is often a more accessible first entry into Japanese convenience retail than the standard format.

What does the Mitsubishi-and-KDDI ownership change in practice?

The joint ownership repositions Lawson from a publicly listed konbini chain into a hybrid retail-plus-telecoms-plus-financial-services platform. KDDI brings the au mobile network, au Pay mobile payments, the Pontacard loyalty programme and a consumer financial-services stack. Mitsubishi brings the upstream food, beverage, materials and energy supply chains plus two decades of accumulated retail know-how at Lawson. The combination is intended to turn the fourteen-thousand-store network into the physical anchor of a deeply integrated digital-and-physical platform — a model with few clear precedents in either Japanese retail or global convenience retail.

Working with Lawson

For overseas FMCG brands, food and beverage exporters, private-label manufacturers, wellness and cosmetics companies, fintech and loyalty partners, and capital providers, Lawson’s post-delisting structure opens a wider and longer-horizon set of entry points than most foreign suppliers have historically considered — from standard-format supplier contracts, to Natural Lawson premium-niche placements, to Lawson Store 100 single-portion items, to Lawson China and 108 Shop Thailand pre-Japan beachhead distribution. Japonity introduces qualified overseas companies to Japanese retailers, trading houses, telcos and consumer-platform operators through its business matching service. If you are exploring a Japan-market entry into convenience-retail distribution, a private-label opportunity with a sogo-shosha-backed channel, or a fintech or loyalty integration into a national konbini network, get in touch to start a conversation.

Related from Japonity — Japan’s retail & convenience-store giants

- Seven & i Holdings — The convenience-store empire targeted by Couche-Tard

- Aeon Group — Japan’s biggest retailer by sales — and ASEAN’s largest mall network

Want to source Japanese products beyond these company profiles? Japonity also runs a Japan Sourcing Hub — a research-grade catalogue of 1,185 verified Japanese food products and 200+ overseas EC stores, ready for B2B procurement.

Interested in Japanese business opportunities?

Whether you're looking for technology partners, engineering talent, or market insights — we can help connect you with the right Japanese organizations.

Get in Touch →