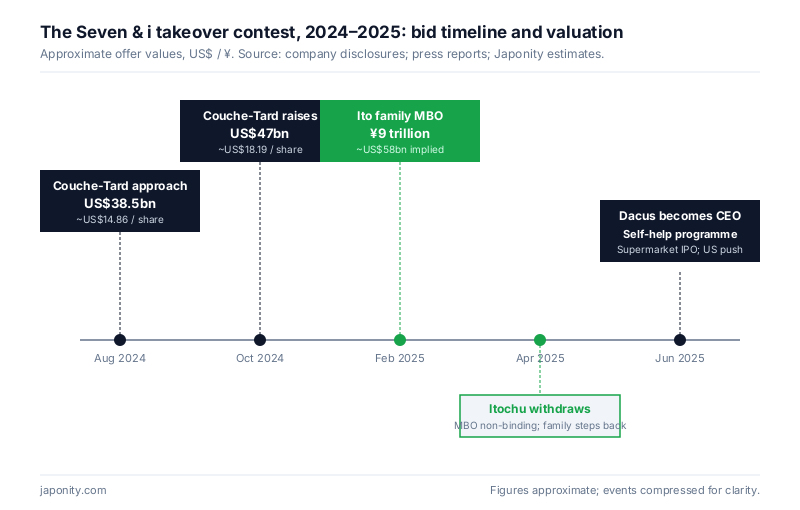

On 19 August 2024, Alimentation Couche-Tard — the Canadian operator of Circle K — confirmed an unsolicited approach to acquire Seven & i Holdings, the Tokyo-listed parent of 7-Eleven. At a headline value north of US$38 billion, it would have been the largest foreign takeover of a Japanese company ever attempted. The target was not just a retailer. It was the operator of more than 85,000 convenience stores across roughly 20 territories — a logistics, real-estate and brand machine that Toshifumi Suzuki had spent four decades industrialising. By January 2025, Junro Ito, son of the founder Masatoshi Ito, had countered with a management buyout proposal in the trillions of yen, mobilising Itochu, Japanese banks and overseas capital partners. The fight that followed has become the most-watched test case of Japan’s foreign-takeover defences since the Toshiba saga — and a referendum on whether a global retail platform headquartered in Tokyo can outrun a North American operator’s view of its own under-utilised assets.

From a Senju kimono shop to 85,000 stores

Seven & i’s lineage runs back to 1920, when Masatoshi Ito’s uncle opened a small clothing store in Asakusa. The Ito family rebuilt it after the war as Yokado, a general-merchandise chain serving Tokyo’s working-class districts, and incorporated it as Ito-Yokado in 1958. For two decades it grew as a suburban-mall operator competing with Daiei and Seiyu — a domestic story, profitable but unremarkable by global standards.

The pivot came in 1973, when a young Ito-Yokado executive named Toshifumi Suzuki licensed the 7-Eleven brand from the US Southland Corporation and opened the first Japanese store in Toyosu, Tokyo. Suzuki’s bet, which his Southland counterparts initially treated as an unlikely territorial experiment, was that the American convenience-store format — small footprint, long hours, dense SKU mix — would translate to urban Japan if it were re-engineered around fresh food, daily replenishment and a tightly choreographed distribution network. He was right. By 1991, 7-Eleven Japan had become the format’s most profitable operator anywhere in the world, and Ito-Yokado used that cash to acquire its struggling US licensor outright — a reverse takeover of the parent that has few parallels in retail history.

Seven & i Holdings, the listed entity that emerged from a 2005 restructuring, was built to consolidate that asset base: 7-Eleven Japan, 7-Eleven Inc. in the United States, Ito-Yokado supermarkets, the Sogo & Seibu department-store chain (acquired in 2006, divested in 2023), Akachan Honpo baby goods, Seven Bank, and a constellation of food manufacturing, logistics and digital businesses. Today the group operates roughly 85,000 stores globally through company-owned, franchised and area-licensed arrangements — more than any other convenience-store operator and, by store count, the largest retail chain in the world.

The shape of the group, by segment

The segment mix is the first thing a foreign buyer or partner needs to understand, because the group’s profit pool, growth trajectory and strategic flexibility differ sharply by line.

| Segment | Approx. share of group revenue | Strategic posture |

|---|---|---|

| 7-Eleven International (mostly US) | ~70% | Growth engine; Speedway integration; under-monetised fresh-food opportunity |

| 7-Eleven Japan | ~15% | Cash cow; saturated domestic market; private-label and digital ID expansion |

| Ito-Yokado & superstores | ~8% | Restructuring target; store closures and IPO of supermarket arm under discussion |

| Financial services (Seven Bank etc.) | ~3% | ATM network monetisation; cross-sell to 7-Eleven customer base |

| Specialty retail (Akachan Honpo, Loft until 2017) | ~2% | Non-core; review pending |

| Sogo & Seibu (department stores) | Divested 2023 | Sold to Fortress Investment Group; out of perimeter |

The headline is that the US business, not Japan, is now the dominant line. That inversion — a Tokyo-headquartered group whose largest segment by revenue, store count and recent capital expenditure is American — is exactly the structural fact that made Couche-Tard’s bid credible. From Laval, Quebec, Seven & i looks less like a Japanese company than like a US convenience-store operator with a Japanese head office attached.

The Speedway acquisition and what it did to the balance sheet

In May 2021, Seven & i’s US arm completed the acquisition of Speedway from Marathon Petroleum for approximately US$21 billion. It was the largest deal in the group’s history and roughly doubled the US store count to over 13,000 outlets. The strategic logic was straightforward: scale benefits in fuel procurement, distribution overlap with existing 7-Eleven Inc. routes, and a chance to lift Speedway’s underperforming food-and-merchandise mix toward 7-Eleven Japan’s category-killer fresh-food economics.

Three years on, the integration is best described as partially delivered. Procurement synergies materialised broadly on schedule. The fresh-food upside — the ambition that Suzuki’s Japan playbook could be transplanted into a US footprint of largely petrol-station retail — has proven harder. American convenience-store customers buy fuel, tobacco, beverages and snacks; converting them into purchasers of bento, onigiri and prepared meals at Japanese gross margins is a multi-year cultural and supply-chain project, not a synergy line in a deal model.

The unfinished business is precisely what Couche-Tard’s analysts identified as a value-creation opportunity that incumbent management was not capturing fast enough. From Laval’s perspective, Seven & i’s US stores were trading inside a Japanese parent whose conglomerate discount, governance structure and slower restructuring of Ito-Yokado were depressing the asset’s market value.

August 2024: the Couche-Tard approach

Couche-Tard’s August 2024 letter was a textbook unsolicited approach. The Canadian bidder is itself a serial acquirer, having rolled up the European Statoil forecourt network, US Pantry Stores and most recently parts of the TotalEnergies portfolio. Its operating model — disciplined cost control, aggressive fuel and merchandise margin optimisation, capital recycling into new acquisitions — is recognised as one of the most efficient in global convenience retail.

The initial offer, reported at around US$14.86 per share or US$38.5 billion, was raised in October 2024 to roughly US$18.19 per share, valuing the equity at approximately US$47 billion. At that level the bid implied a premium of more than 20 per cent to the undisturbed share price and would have given Seven & i shareholders one of the highest exit valuations in recent Japanese M&A history.

The response from Tokyo was firm but measured. The board established a Special Committee of independent directors to evaluate the proposal, declined to engage on the first offer on valuation grounds, and demanded reassurance on antitrust risk. The latter point was substantive rather than rhetorical: a Couche-Tard / 7-Eleven combination would have controlled an outright majority of US convenience-store outlets in many metropolitan areas, triggering near-certain Federal Trade Commission divestiture demands of a scale that no convenience-store transaction in US history had attempted.

January 2025: the Ito family management buyout

The countermove arrived on 6 February 2025, when Seven & i confirmed a non-binding management buyout proposal from a group led by Junro Ito, the founder’s son and a Seven & i director, in partnership with Itochu Corporation. The vehicle, structured under the working name FemtoStream Holdings in some legal filings, would have valued the company at roughly ¥9 trillion (around US$58 billion) — implying a meaningful premium to Couche-Tard’s revised offer.

The MBO architecture was instructive. Itochu, one of Japan’s five great trading houses and an existing partner of FamilyMart (the convenience-store chain that competes directly with 7-Eleven in Japan), would have taken a strategic stake. Japan’s three megabanks — Mitsubishi UFJ, Sumitomo Mitsui and Mizuho — were lined up to provide acquisition financing. Bain Capital and other foreign private-equity firms were sounded out as minority equity participants. The Ito family’s combined direct and indirect holdings would have served as the anchor equity. Within weeks, however, financing complications and Itochu’s eventual withdrawal in February 2025 led the family-led group to step back from a formal binding bid.

The MBO’s collapse did not end the contest. Instead, Seven & i’s board pivoted to a self-help programme: a planned listing of the supermarket business, an accelerated US restructuring under newly appointed President Stephen Dacus (who succeeded Ryuichi Isaka as CEO in spring 2025), and a commitment to return cash to shareholders sufficient — the board argued — to close the gap that Couche-Tard’s offer had exposed. Negotiations with Couche-Tard remained live through 2025 but on terms in which Seven & i retained control of the timetable.

What the fight reveals about Japan’s foreign-takeover landscape

The Seven & i situation is the most consequential cross-border takeover contest in Japan since the Toshiba going-private process of 2023. Three structural lessons emerge.

The METI defence framework is real but not absolute. Japan’s revised Foreign Exchange and Foreign Trade Act gives the Ministry of Economy, Trade and Industry standing to scrutinise foreign acquisitions of companies designated as strategically sensitive. Convenience-store retail is not, on its face, on the protected list — but the operational footprint (food security, payments infrastructure, ATM networks, disaster-relief logistics) gave METI a defensible foothold to require consultation. Couche-Tard could not bypass the review, and the practical effect was to slow the auction to a Japanese-board-friendly cadence.

Family stewardship still matters at scale. Masatoshi Ito died in March 2023 at the age of 98. Two years later, his son Junro mobilised family capital, friendly trading-house relationships and the moral authority of the founding name to credibly counter a US$47 billion offer. That a single founding family could, in 2025, organise a defensive MBO on a comparable scale to the inbound bid is not the picture of Japanese corporate governance that international investors usually carry. It is, however, increasingly representative of how Japan’s largest privately-anchored public companies — Kao, Daikin, SoftBank, Keyence, Nidec — actually behave when contested.

The conglomerate discount is the real adversary. Couche-Tard’s bid was not principally an offer to operate Seven & i’s assets better. It was an offer to liberate them from a conglomerate structure whose market value was demonstrably less than the sum of its parts. Seven & i’s own response — divesting Sogo & Seibu, IPO-ing the supermarket arm, accelerating US restructuring, raising buybacks — is an acknowledgement that the discount was real. The board’s argument is that Japanese management can close that discount in-house. Couche-Tard’s argument was that only a change of ownership could. The next eighteen months will adjudicate which is right.

What this means for foreign companies engaging with the group

For an overseas firm — a supplier, a partner, a private-label manufacturer, a logistics provider, an investor — the Seven & i situation matters in concrete operational ways.

- The procurement door is open but disciplined. 7-Eleven Japan’s private-label programme (Seven Premium, Seven Gold) sources from a tightly managed network of Japanese and overseas manufacturers. The standards are exacting; the volumes are large. Foreign suppliers who can clear the food-safety and consistency thresholds find one of the most reliable buyers in global retail.

- The US business is the integration story. Speedway’s conversion to 7-Eleven branding, the fresh-food rollout, and the loyalty-programme unification (7Rewards) are creating procurement opportunities for foreign food, beverage and packaging firms at a scale that the Japan business cannot match.

- Financial services is an under-noticed line. Seven Bank’s ATM network — installed inside 7-Eleven stores nationwide — is one of the most-used cash and remittance channels in Japan and a critical inbound-tourism payment touchpoint. Foreign payments and remittance firms (Western Union, Wise, regional Asian operators) have multi-year partnership tracks here.

- Real estate and logistics carry hidden value. The group’s distribution centres, fresh-food factories and store-network real estate are the operational backbone that any acquirer — Couche-Tard, an MBO, or a future bidder — would be paying for. Foreign logistics-tech, refrigeration and supply-chain firms have a credible buyer here.

- Governance is in flux. Board composition, foreign-director ratio and the role of the Special Committee on M&A matters have all evolved through 2024–25. Foreign engagement should now go through the IR and Strategy functions in Tokyo, which have been materially upgraded since the bid.

The next chapter

By mid-2025, the contest has not closed. Couche-Tard’s revised offer remained on the table through the first half of the year; Seven & i’s self-help programme is being delivered in instalments. The supermarket-arm IPO, the supermarket portfolio rationalisation and the US restructuring will each produce data points that the market — and any future bidder — will price. Whether the group ultimately stays Japanese-listed, accepts a structured Couche-Tard transaction with US divestitures attached, or executes a renewed family-anchored buyout is unresolved. What is no longer in question is that the global value of 7-Eleven’s footprint has been re-marked. The conglomerate discount that quietly cost Seven & i shareholders for two decades is, finally, being negotiated away.

For overseas observers, the lesson is straightforward. Japan in 2025 is open to cross-border takeover offers in a way it was not five years ago — but openness is not the same as inevitability. A founding family, a trading-house ally, a co-operative bank syndicate and a board willing to use the time the regulatory process buys can still write the ending. The interesting question is no longer whether large Japanese companies are takeoverable. It is what price, and on what terms, their incumbent stewards will choose to accept.

FAQ

What was Alimentation Couche-Tard’s 2024 bid for Seven & i Holdings?

In August 2024, Couche-Tard — the Canadian operator of Circle K — made an unsolicited approach to acquire Seven & i Holdings at roughly US$14.86 per share, valuing the equity at about US$38.5 billion. After Seven & i’s board rejected the initial offer on valuation grounds, Couche-Tard raised the proposal in October 2024 to approximately US$18.19 per share, or around US$47 billion in total. It would have been the largest foreign takeover of a Japanese company on record. Negotiations remained live into 2025, with Seven & i’s Special Committee weighing the offer alongside antitrust risk in the US convenience-store market.

What is the Ito family’s role in Seven & i?

The Ito family founded the company in 1920 and built it into Ito-Yokado, the supermarket chain that became Seven & i Holdings’ anchor. Masatoshi Ito, who led the group for decades, died in March 2023 at the age of 98. His son Junro Ito, a Seven & i director, led the January 2025 management buyout proposal that valued the group at roughly ¥9 trillion (about US$58 billion). Though the MBO did not progress to a binding bid after Itochu withdrew, the family retains significant economic and reputational influence and continues to be central to the group’s governance trajectory.

How does 7-Eleven’s US business compare with its Japan business?

Measured by revenue and store count, the US business is now substantially larger. 7-Eleven International — overwhelmingly the US operation — accounts for roughly 70 per cent of group revenue, while 7-Eleven Japan contributes around 15 per cent. The Japan business, however, remains the higher-margin operator, anchored by category-defining fresh food, dense urban store coverage and a private-label programme that competitors have struggled to replicate. The US business, expanded sharply by the 2021 Speedway acquisition, is the growth and restructuring story; Japan is the cash and brand engine.

What was the FemtoStream Holdings MBO proposal?

FemtoStream Holdings was the working name of the acquisition vehicle reported in connection with Junro Ito’s February 2025 management buyout proposal. Backed by the Ito family, Itochu Corporation and a syndicate of Japanese megabanks, the vehicle was structured to take Seven & i private at roughly ¥9 trillion. The proposal was non-binding and ultimately stepped back from formal commitment after financing complications and Itochu’s withdrawal. It nonetheless reset the conversation: by signalling that Japanese family capital could organise a counter-offer above Couche-Tard’s bid, it constrained the Canadian bidder’s optionality.

Why did Seven & i acquire Speedway in 2021?

The US$21 billion acquisition of Speedway from Marathon Petroleum, completed in May 2021, roughly doubled 7-Eleven Inc.’s US store count to more than 13,000 outlets. The strategic logic combined fuel-procurement scale, route-density overlap with existing 7-Eleven Inc. stores, and the ambition to import 7-Eleven Japan’s fresh-food category economics into a largely petrol-station footprint. Procurement and back-office synergies have largely landed. The fresh-food upside is partially delivered and remains the principal value-creation lever — and the precise opportunity that Couche-Tard argued incumbent management was capturing too slowly.

Working with Seven & i

Japonity helps overseas suppliers, food and beverage manufacturers, payments and remittance operators, logistics-tech firms and capital partners engage with Seven & i Holdings and the wider Japanese convenience-store ecosystem on substantive terms. Whether you are a private-label candidate seeking entry into Seven Premium, a foreign operator interested in the Speedway-to-7-Eleven conversion supply chain, or an investor mapping the group’s evolving governance and capital structure, we provide the introductions, diligence support and on-the-ground coordination required to make engagement viable.

To start a conversation, visit our business matching page.

Related from Japonity — Japan’s retail & convenience-store giants

- Aeon Group — Japan’s biggest retailer by sales — and ASEAN’s largest mall network

- Lawson — The konbini now jointly owned by Mitsubishi Corp and KDDI

Want to source Japanese products beyond these company profiles? Japonity also runs a Japan Sourcing Hub — a research-grade catalogue of 1,185 verified Japanese food products and 200+ overseas EC stores, ready for B2B procurement.

Interested in Japanese business opportunities?

Whether you're looking for technology partners, engineering talent, or market insights — we can help connect you with the right Japanese organizations.

Get in Touch →