Kose Corporation is Japan’s second-largest cosmetics company by revenue, sitting behind Shiseido and ahead of POLA Orbis and Mandom, with consolidated sales of approximately ¥300 billion. It is the rare top-tier Japanese beauty house that is still meaningfully family-controlled: founded in Tokyo in 1946 by Kozaburo Kobayashi, the company remains anchored by the Kobayashi family, which holds an approximately 40%-plus stake. Two strategic moves define its modern profile — the 1985 launch of Sekkisei, which became Japan’s most-sold single skincare product for years, and the 2014 acquisition of U.S. color cosmetics brand Tarte for approximately $135 million, which gave Kose a millennial-and-Gen-Z direct line into the United States that no other Japanese beauty company has matched.

A family company that scaled without going generic

Kozaburo Kobayashi founded Kose Inc. (小林合名会社 reorganized as コーセー) in Tokyo’s Nihonbashi district in 1946, in the immediate post-war retail vacuum where small Japanese consumer brands began rebuilding from raw materials and door-to-door distribution. The company spent its first decade as a regional supplier of basic skincare and hair products. The strategic pivot came in 1956 with the launch of Albion, a premium counter-service brand that established Kose’s institutional muscle in department-store retail and gave it the credibility to operate in the luxury tier alongside Shiseido and the European houses.

What Kose did not do, and what now distinguishes it, was reorganize itself around a single tiered brand pyramid. Shiseido, the larger of the two, runs a layered house structure where the corporate name sits across mass and prestige. Kose chose instead to build, hold, and acquire distinctly branded operating companies that share R&D and back-office infrastructure but retain their own counter identities, marketing teams, and even balance-sheet personalities. Albion was held as a separate company. DECORTÉ launched in 1970 as a premium-only counter brand. Kose Cosmeport was carved out for drugstore distribution. Tarte, when it was acquired in 2014, was deliberately not folded into the Kose visual system. The result is a portfolio that looks more like LVMH’s beauty stable than Shiseido’s tiered house.

The Kobayashi family and the governance question

Kose’s listing on the Tokyo Stock Exchange (ticker 4922) coexists with one of the largest founding-family equity blocks among Japanese consumer companies. The Kobayashi family, through direct holdings and family holding vehicles, controls approximately 40%-plus of outstanding shares. Kazuhiro Kobayashi, the second-generation family leader, has held the chairman role for most of the modern era; his son Mitsuhito Kobayashi has been positioned in senior executive responsibility, including the president role, in the company’s most recent leadership transitions.

This matters for two reasons. First, it means strategic decisions — long-cycle R&D investment, overseas acquisitions, brand portfolio choices — are made on family-stewardship horizons rather than quarterly activist horizons. The 2014 Tarte deal, which a fully institutionalized board might have hesitated on given the price tag and the cultural distance, was executed cleanly because the controlling family was willing to underwrite it. Second, it means foreign partners, licensors, and acquirers reading Kose through a standard listed-company lens often misread how decisions actually get made. The relevant counterparty is frequently a small group inside the Kobayashi orbit, not a layered Tokyo head-office process.

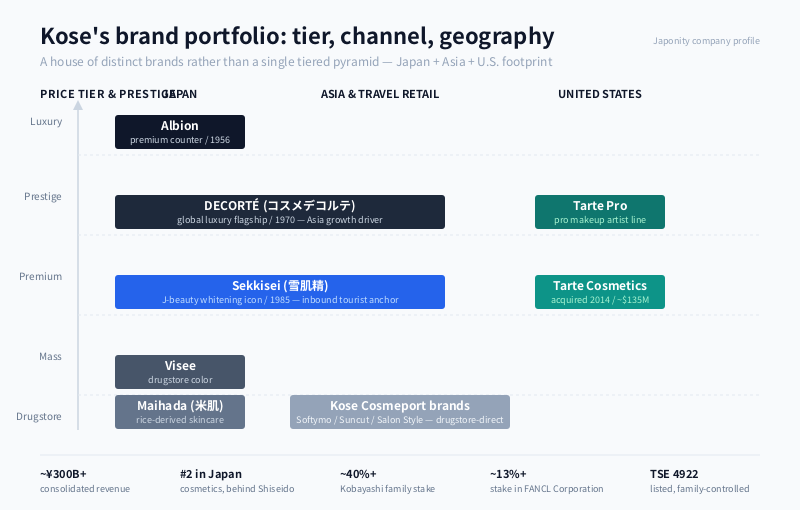

The brand portfolio nobody draws cleanly

The clearest way to read Kose is by the brand stack, because the corporate name itself does very little work in the consumer-facing market. The table below summarizes the company’s main brand assets by tier and channel.

| Brand | Tier | Channel | Strategic role |

|---|---|---|---|

| DECORTÉ (コスメデコルテ) | Premium prestige | Department store counter, travel retail | Global luxury flagship; Asia/China growth driver |

| Albion | Premium luxury | Department store counter (separate company) | Domestic Japan high-end loyalty franchise |

| Sekkisei (雪肌精) | Mid-premium | Department store, specialty, travel retail | J-beauty whitening icon; Asia tourist anchor |

| Tarte Cosmetics | Mass-premium color | Sephora, Ulta, DTC, social | U.S./global millennial color cosmetics |

| Tarte Pro | Professional | Pro makeup artists, education | Credibility layer above Tarte mainline |

| Visee | Mass color | Japanese drugstore, GMS | Domestic drugstore color cosmetics share |

| Maihada (米肌) | Skincare | Japan specialty / DTC | Domestic rice-derived skincare line |

| Kose Cosmeport brands (e.g. Softymo, Suncut, Salon Style) | Mass | Drugstore | Volume and household penetration |

Two things stand out. First, the gap between DECORTÉ at the top and the Kose Cosmeport drugstore brands at the bottom is wider than Shiseido’s equivalent range — Kose has chosen not to lean as hard on a single house-of-brands signal. Second, Tarte and Tarte Pro sit almost entirely outside the Japanese consumer’s awareness; the brand is treated by Kose management as a U.S./global business with its own P&L culture, not as a Japanese product translated for foreign markets.

Sekkisei: the single-product franchise that built modern Kose

Sekkisei, launched in 1985, is the most important product in Kose’s history and one of the most commercially significant skincare launches in post-war Japan. The hero SKU — Sekkisei Lotion, the blue-bottled whitening toner with the Japanese herbal extract formulation — became Japan’s most-sold single cosmetic product for an extended run through the late 1990s and 2000s, a position that few single skincare items in any market have held for that long. The franchise has since expanded into emulsions, masks, sunscreens, and a higher-priced Sekkisei Clear Wellness tier.

Sekkisei’s strategic value to Kose goes well beyond its domestic shelf footprint. It became one of the defining “J-beauty” icons for inbound Asian tourists during the 2010s and early 2020s, particularly from mainland China, Taiwan, Hong Kong, and Korea. Travel-retail demand at Narita, Haneda, Kansai, and Hong Kong duty-free turned Sekkisei into a cross-border franchise without the company needing to build full retail presence in those markets. When inbound traffic collapsed in 2020-2022, that exposure became a vulnerability; the recovery of inbound Chinese travel into 2024-2025 has been a major swing factor for Kose’s domestic earnings.

The 2014 Tarte acquisition and what it actually bought

In February 2014, Kose acquired Tarte Cosmetics, a New York-based color cosmetics brand founded in 1999 by Maureen Kelly, for approximately $135 million. At the time the deal was widely covered as a competent but unremarkable mid-size cross-border acquisition. In retrospect it is one of the most strategically valuable beauty M&A moves any Japanese company has made in the past two decades.

Tarte gave Kose three things that no organic effort would have delivered. First, a brand that already had genuine purchase intent and social-platform authority among U.S. millennials, anchored on the Amazonian Clay foundation, the Shape Tape concealer, and a sequence of viral palettes. Second, a distribution position inside Sephora and Ulta — the two channels that govern U.S. prestige and mass-premium beauty discovery — that a Japanese-founded brand would have taken a decade to earn. Third, a marketing organization fluent in the social, creator, and DTC playbook in the U.S., which Kose’s Tokyo team did not have and arguably could not have built in-house.

Kose’s management has been disciplined about not over-Japanizing Tarte. The brand has retained its New York creative direction, its product-development cadence, and its visual identity. The Tarte Pro extension, aimed at professional makeup artists and beauty educators, gave the franchise an upmarket credibility layer that Kose has lightly mirrored in Japan but has been content to let run on its own terms in the U.S. The result is that, more than a decade after the deal closed, Tarte continues to operate as a meaningfully American business owned by a Japanese parent, rather than as a Japanese brand wearing an American jacket.

How Kose differs from Shiseido, POLA Orbis, and Mandom

The Japanese cosmetics oligopoly is small enough that the four listed leaders — Shiseido, Kose, POLA Orbis, and Mandom — can be cleanly distinguished by what they choose to optimise for. The structural differences matter for partners, licensors, and acquirers because they shape what kind of conversation is actually available.

| Company | Approx. revenue (¥B) | Approx. global Japan exposure | Brand structure | Strategic identity |

|---|---|---|---|---|

| Shiseido | ~¥900-1,000 | Heavily global, China-exposed | Tiered house: prestige (Clé de Peau, SHISEIDO) → premium → mass | Global prestige flagship; restructuring mass portfolio |

| Kose | ~¥300+ | Japan + Asia + U.S. (Tarte) | House of distinct brands: DECORTÉ / Sekkisei / Albion / Tarte | Family-controlled; U.S. millennial reach via Tarte |

| POLA Orbis | ~¥200 | Japan-heavy | POLA (counselling), Orbis (direct), ITRIM, Jurlique etc. | Direct-selling and counselling DNA |

| Mandom | ~¥70-80 | Japan + Indonesia | Men’s grooming led (Gatsby, Lúcido) | Men’s grooming + Southeast Asia mass |

Shiseido is the global prestige flagship and the most exposed to Chinese consumer cycles. Kose is meaningfully smaller but structurally more diversified across U.S. millennial color, Asian J-beauty, and domestic department-store prestige, and is the only one of the four with a serious U.S. operating business. POLA Orbis is anchored on direct-selling and counselling-led skincare; Mandom is a focused men’s grooming and Southeast Asia mass-market specialist. The strategic conversations these four companies are willing to have with foreign partners are very different — Shiseido prioritizes global prestige scale, Kose tolerates portfolio additions that look quite unlike its existing brands, POLA Orbis is selective about counselling-channel fit, and Mandom is focused on Indonesia and the men’s category.

The FANCL stake and the limits of consolidation

Kose holds an approximately 13%-plus equity stake in FANCL Corporation, the Yokohama-based Japanese skincare and health-food company known for its preservative-free product philosophy and direct-to-consumer roots. The position, built up over multiple tranches, is sometimes read as a precursor to deeper consolidation. The cleaner reading is that it is a strategic alliance stake — close enough to align on category positioning and cross-border opportunities, deliberately short of the level that would force a full bid.

That posture is consistent with how the Kobayashi family has historically operated. Kose has not pursued the kind of consolidation moves that would convert it into a Japanese L’Oréal. It has instead built a portfolio through selective acquisitions (Tarte) and minority alliances (FANCL) that preserve operational independence at the target company while giving Kose category insight and optionality. Whether that posture survives the next generation of family leadership, and whether the FANCL stake eventually moves to a control transaction, are open questions worth watching.

Geography: Japan + Asia + U.S., not Asia + Europe

Kose’s geographic footprint differs from Shiseido’s in a way that is often missed. Shiseido has built up meaningful European prestige distribution and acquired or developed several Western brands (Clé de Peau, Drunk Elephant in 2019, Nars, Laura Mercier historically). Kose’s Western exposure is concentrated in the United States via Tarte and limited in Europe. Its non-U.S. international business sits squarely in Asia — China, Taiwan, Hong Kong, Korea, Thailand, Singapore — with travel retail playing an outsized role.

This geographic shape has implications for partners. For Korean or Chinese skincare brands seeking a Japanese distribution partner or capital ally, Kose is a more focused conversation than Shiseido because Asia is more central to its growth thesis. For U.S. or European indie color brands looking for a Japanese acquirer that knows how to run a non-Japanese operating company without smothering it, the Tarte precedent makes Kose a more credible counterparty than the alternative Japanese majors.

R&D: Kose Cosmetology Laboratory and the skincare science layer

Kose’s R&D is consolidated under the Kose Cosmetology Laboratory and the company’s Tokyo and Gunma research facilities. The institutional focus has historically been on skincare actives — whitening (Sekkisei), anti-aging (DECORTÉ), rice-derived ingredients (Maihada), and travel-retail-friendly formulations combining sunscreen and brightening claims. Unlike some of the keiretsu-rooted Japanese majors, Kose does not maintain a closed supplier club; ingredient houses and packaging firms outside the traditional Japanese cosmetics base have been able to qualify into Kose programs when the technology is genuinely differentiated.

Where Kose is exposed, and where it is durable

The exposures are well-mapped: Chinese consumer demand recovery, inbound tourism into Japan, the U.S. prestige-beauty cycle via Tarte, and foreign exchange. The Chinese exposure is real but smaller in proportion than Shiseido’s. The durable elements are less discussed: Albion’s multi-decade department-store loyalty franchise, the Kose Cosmeport drugstore business that underwrites R&D scale, and Sekkisei’s brand longevity through multiple macro cycles. The Kobayashi family’s willingness to hold and invest through downturns has allowed the company to avoid the kind of restructuring trauma Shiseido has experienced in its mass-cosmetics divestments.

Why Kose warrants its own read

The default framing — “Japanese cosmetics” — collapses Kose into a Shiseido sub-narrative. That is a mistake. Kose is a structurally different business: family-controlled, brand-portfolio-led rather than house-tier-led, exposed to the U.S. through a fully owned American brand that it has deliberately not Japanized, and anchored on a J-beauty franchise (Sekkisei) that has outlived most competing single-product propositions. The 2014 Tarte acquisition turned out to be one of the better cross-border consumer M&A trades of the decade, and the FANCL stake leaves an option open for further consolidation on the family’s terms.

For foreign partners — whether they are indie brand founders, ingredient suppliers, packaging innovators, distribution partners in Asia, or capital allies — the practical question is which counterparty inside Kose the conversation should run through. The corporate name does relatively little work; the relevant entry point depends on the brand. That is the kind of detail that matters when a first meeting decides whether the next two years of engagement are productive or wasted.

FAQ

Who owns Kose Corporation?

Kose is publicly listed on the Tokyo Stock Exchange (ticker 4922) but remains substantially controlled by the founding Kobayashi family, which holds an approximately 40%-plus equity stake through direct holdings and family vehicles. Kazuhiro Kobayashi, the second-generation family leader, has held the chairman role in the modern era, and his son Mitsuhito Kobayashi has been positioned in senior executive responsibility including the president role. This level of founding-family control is unusual among Japan’s top-tier consumer companies and shapes how strategic decisions get made.

What is Sekkisei and why does it matter to Kose?

Sekkisei is a Japanese skincare line launched by Kose in 1985, anchored on a hero whitening lotion in a blue bottle that uses Japanese herbal extracts. It became Japan’s most-sold single cosmetic product for an extended run through the late 1990s and 2000s, a rare achievement for a single skincare SKU. Beyond domestic share, Sekkisei became one of the defining “J-beauty” icons for inbound Asian tourists, particularly from mainland China, and remains a major driver of travel-retail and inbound demand for Kose.

How big is Tarte Cosmetics in Kose’s business?

Kose acquired Tarte Cosmetics in 2014 for approximately $135 million. Tarte operates as a meaningfully American business — its product development, creative direction, and distribution remain U.S.-centered, with Sephora and Ulta as core retail channels. The brand gives Kose a U.S. millennial and Gen-Z reach that no other Japanese cosmetics company has matched. Kose has been deliberately disciplined about not folding Tarte into a Japanese brand system, which is a major reason the franchise has continued to grow under Japanese ownership.

How is Kose different from Shiseido?

Shiseido is roughly three times Kose’s revenue and is structured as a tiered house of brands led by the corporate name, with heavy exposure to global prestige and to China. Kose is smaller, family-controlled, and built as a house of distinct brands (DECORTÉ, Sekkisei, Albion, Tarte, Visee) rather than a single tiered pyramid. Kose has a stronger U.S. operating position via Tarte, less European prestige exposure than Shiseido, and a more concentrated Asia + U.S. growth profile. The two are competitors at the Japanese department-store counter but follow noticeably different strategic models.

What is the FANCL stake and is it a takeover signal?

Kose holds an approximately 13%-plus equity stake in FANCL Corporation, the Yokohama-based skincare and health-food company. The position has been built up over multiple tranches and currently functions as a strategic alliance rather than a precursor to a control bid. It is consistent with how the Kobayashi family has historically operated — selective minority stakes and clean acquisitions, but not aggressive consolidation. Whether the stake eventually moves to a full transaction is an open question tied to the family’s next-generation leadership decisions.

Working with Kose

For overseas brand founders, ingredient suppliers, packaging technology firms, distribution partners in Asia or the U.S., and capital allies, Kose offers several distinct paths of engagement. Indie brand founders looking for a Japanese acquirer that knows how to run a non-Japanese operating company without smothering it will find the Tarte precedent more relevant than any precedent at Shiseido or POLA Orbis. Ingredient and formulation suppliers can engage through the Kose Cosmetology Laboratory, where the supplier qualification process is comparatively open relative to keiretsu-rooted Japanese majors. Asian distributors and travel-retail partners can build conversations around the Sekkisei and DECORTÉ franchises.

The practical detail that matters most is which counterparty inside Kose the conversation should actually run through, because the corporate name does relatively little of the work. DECORTÉ, Albion, Tarte, Sekkisei, and Kose Cosmeport each have their own operating cadence and decision-making centers, and the right first conversation depends on the brand. If your company is exploring partnership, licensing, or capital alignment with Kose or with Japanese cosmetics more broadly, Japonity’s business matching service can help structure a credible first conversation with the right counterparty.

Related from Japonity — Japan’s consumer-and-retail brands

- Aeon Group — Japan’s biggest retailer by sales — and ASEAN’s largest mall network

- Pan Pacific International Holdings — Don Quijote and DON DON DONKI — the only Japanese mass-retailer to crack overseas Asia

- Nitori Holdings — Japan’s IKEA — the 36-year profit-growth streak

Want to source Japanese products beyond these company profiles? Japonity also runs a Japan Sourcing Hub — a research-grade catalogue of 1,185 verified Japanese food products and 200+ overseas EC stores, ready for B2B procurement.

Interested in Japanese business opportunities?

Whether you're looking for technology partners, engineering talent, or market insights — we can help connect you with the right Japanese organizations.

Get in Touch →