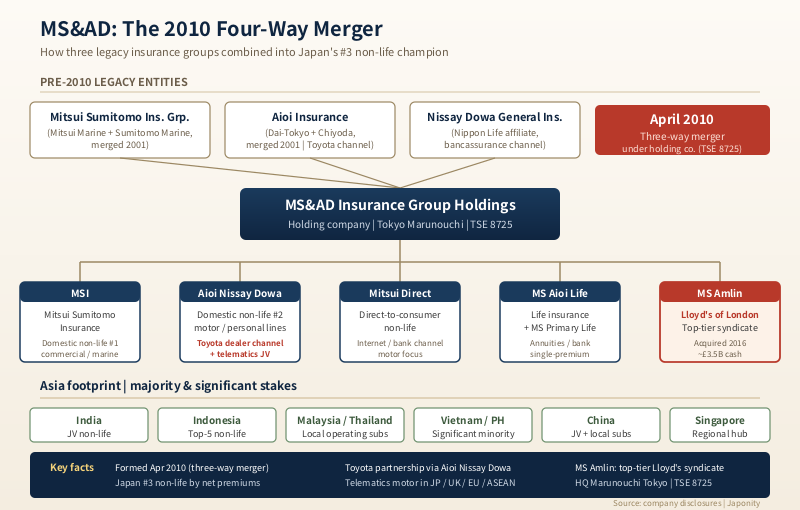

In April 2010, four mid-sized Japanese non-life insurers — Mitsui Sumitomo Insurance, Aioi Insurance, Nissay Dowa General Insurance and the holding company that bound them together — completed one of the most complicated mergers in modern Japanese corporate history. The resulting entity, MS&AD Insurance Group Holdings, has spent the subsequent fifteen years quietly turning that structural complexity into competitive advantage. It is now Japan’s third-largest non-life insurer by net premiums, the owner of MS Amlin — a top-quartile Lloyd’s of London syndicate acquired in 2016 for roughly £3.5 billion — and the partner of choice for Toyota Motor Corporation in the global build-out of telematics-based auto insurance. For foreign reinsurance buyers looking at Japan, and for Asian-market entrants looking for a Japanese underwriting partner, MS&AD is the most international and the most idiosyncratic of the three Japanese non-life champions. Understanding which subsidiary does what — and why — is the difference between a smooth placement and a six-month exercise in entity confusion.

The four-way merger that nobody outside Japan really understood

To grasp MS&AD’s structure, it helps to start with the merger arithmetic. In April 2010, three separate non-life insurance groups combined under a single holding company listed on the Tokyo Stock Exchange as 8725. The first leg, Mitsui Sumitomo Insurance Group Holdings, was itself the product of an earlier 2001 merger between Mitsui Marine and Fire and Sumitomo Marine and Fire — two of the oldest non-life carriers in Japan, with roots in the Meiji-era marine cargo trade. The second leg, Aioi Insurance, was formed in 2001 by combining Dai-Tokyo Fire and Marine with Chiyoda Fire and Marine, and had spent the subsequent decade building a deep distribution relationship with Toyota dealerships across Japan. The third leg, Nissay Dowa General Insurance, was a smaller carrier tied to Nippon Life — the country’s largest life insurer — and brought a captive bancassurance and life-cross-sell distribution channel that neither of the other two possessed.

The deal logic was demographic and regulatory in equal measure. Japan’s non-life insurance market had been over-capacitised for a decade; underwriting margins on the dominant compulsory automobile liability product were thin and getting thinner; and the Financial Services Agency had made clear that capital efficiency at the level of holding-company solvency, rather than at the operating-subsidiary level, would drive its supervisory expectations going forward. Consolidation was, in practical terms, the only way to defend domestic returns while building the international franchise that organic growth could not deliver.

What the merger produced was not a single insurer with a single brand. It produced a holding company with two parallel non-life operating subsidiaries — Mitsui Sumitomo Insurance (MSI) and Aioi Nissay Dowa Insurance (ADI), the latter being the post-2010 fusion of Aioi and Nissay Dowa — each retaining its own brand, distribution network, agent relationships and underwriting culture. A third subsidiary, Mitsui Direct General Insurance, was kept separate as a direct-to-consumer brand sold over the internet and through bank channels. The life insurance side was organised under two further subsidiaries, Mitsui Sumitomo Aioi Life Insurance and Mitsui Sumitomo Primary Life Insurance, the latter focused on single-premium variable annuities distributed through banks. The result, on paper, looks redundant. In practice it preserves the distribution moats — Toyota dealerships will not sell a non-Aioi policy; Nippon Life agents will not push a non-MSI-Aioi product — that were the strategic prize of the merger in the first place.

Why the three-way non-life oligopoly matters

Japanese non-life insurance is a three-firm market. Tokio Marine Holdings, Sompo Holdings and MS&AD between them control roughly nine-tenths of domestic net premiums written, and the competitive dynamics are calibrated less around price than around distribution and capital allocation. For a foreign reinsurer, a Lloyd’s syndicate, or a global broker placing Japanese risk, knowing which of the three to engage — and on which line of business — is the first-order question.

| Dimension | Tokio Marine | MS&AD | SOMPO |

|---|---|---|---|

| Domestic non-life share | ~25% | ~30% (combined MSI + ADI) | ~25% |

| Principal non-life subs | Tokio Marine & Nichido | MSI + Aioi Nissay Dowa + Mitsui Direct | Sompo Japan |

| International franchise | Philadelphia, HCC, Pure (US specialty) | MS Amlin (Lloyd’s), Asia majority stakes | Endurance / Sompo International (Bermuda) |

| Lloyd’s presence | Tokio Marine Kiln (top-5 syndicate) | MS Amlin (top-5 syndicate) | Sompo Syndicate (mid-tier) |

| Auto telematics partner | Internal | Toyota (deep keiretsu partnership) | Internal |

| Reputation with brokers | Most disciplined underwriter | Most international, complex structure | Most aggressive in nursing care, US specialty |

Tokio Marine’s signature is underwriting discipline and a US specialty book built through three large acquisitions. SOMPO is the most aggressively diversified — into nursing care, US specialty insurance and digital ventures — and has historically been the most willing to take strategic risk. MS&AD sits between the two: more international than SOMPO measured by London-market presence, more structurally complex than Tokio Marine, and more tightly woven into Japan’s corporate keiretsu networks than either. The Toyota relationship, in particular, is structural rather than commercial — Aioi Nissay Dowa is functionally the captive auto insurer for Toyota’s domestic dealer network, and that distribution lock is not something a foreign or domestic competitor can replicate at any sensible price.

MS Amlin and the Lloyd’s footprint

The single most consequential capital allocation decision by MS&AD since the 2010 merger was the acquisition of Amlin plc in early 2016 for approximately £3.5 billion in cash. Amlin was a FTSE 250-listed insurer with one of the larger Lloyd’s syndicates, a Bermuda reinsurance platform and a continental European specialty book. Renamed MS Amlin after the deal closed, it became the international underwriting backbone of the MS&AD group and gave the Japanese parent a top-quartile presence in the London market — something no other Japanese non-life insurer has matched at comparable scale.

The strategic rationale was twofold. First, Japan’s domestic non-life market generates relatively predictable but low-margin cash flow; the MS Amlin acquisition gave MS&AD access to harder-currency, harder-priced specialty risk — marine, energy, property catastrophe, financial lines — at Lloyd’s pricing rather than at the compressed margins of Tokyo motor and fire. Second, the deal positioned the group to recycle Japanese yen capital into sterling- and dollar-denominated underwriting at a moment when Lloyd’s was structurally short of capital and pricing was rebuilding from the 2011-2012 soft cycle.

The execution has not been linear. MS Amlin posted material losses in the late 2010s as the Lloyd’s market experienced a string of catastrophe years and adverse reserve development on long-tail US casualty lines. The group restructured aggressively from 2018 onward — exiting underperforming classes, shrinking Bermuda reinsurance capacity, and rebuilding the underwriting team. By the early 2020s the franchise was returning to profitability on a hardened market, and the MS Amlin syndicate now consistently ranks in the top tier at Lloyd’s by premium income. For foreign brokers, the takeaway is that MS&AD has a real London-market underwriting capability rather than a portfolio investment dressed up as an operating subsidiary — placements can be led, not just followed, out of London.

The Toyota partnership and the telematics bet

If MS Amlin is MS&AD’s international story, the Toyota partnership is its domestic moat and its digital bet. Aioi Nissay Dowa Insurance has been the principal non-life insurance partner of Toyota Motor Corporation for more than two decades, with distribution through Toyota’s dealer network in Japan and an increasingly tight collaboration on telematics-based motor insurance — products that price premium based on how, when and where the policyholder actually drives, rather than on demographic proxies alone.

The partnership has progressively globalised. Aioi Nissay Dowa established telematics operations in the UK and continental Europe in the mid-2010s, and the joint venture with Toyota for connected-car insurance has expanded into ASEAN and selected emerging markets. The structural insight is that Toyota’s connected-car platform — the data feed from vehicle telematics units — is one of the largest, most consistent and most underwriting-relevant data sets in the global auto industry. Owning the exclusive insurance distribution relationship to that data feed gives Aioi Nissay Dowa an analytics advantage that no greenfield insurer, however well capitalised, can match in a reasonable time frame.

The economics are subtle. Telematics-based pricing does not on its own widen margins — competitive pressure compresses them on the same time scale. What it does is shift the loss-cost curve: better drivers are correctly identified and priced, worse drivers are correctly identified and either priced or declined, and the adverse selection that bedevils traditional motor underwriting is materially reduced. For a portfolio the size of the Aioi Nissay Dowa Japanese motor book — measured in tens of millions of policies — even a low single-digit improvement in combined ratio is worth tens of billions of yen annually.

The Asia footprint that does the quiet work

Beyond MS Amlin in London and the Toyota partnership in motor, MS&AD has built the most extensive Asian non-life insurance footprint of any Japanese insurer. The group holds majority or significant minority stakes in carriers across India, China, Indonesia, Malaysia, Thailand, the Philippines, Vietnam and Singapore. In several of those markets — Indonesia and Malaysia in particular — the MS&AD subsidiary or affiliate is among the top-five non-life insurers by gross premium written, providing a fully local underwriting platform rather than a Japanese carrier with a representative office.

The strategic logic mirrors the megabanks’ ASEAN expansion. Japan’s domestic non-life market is mature, low-growth and capital-rich; Asian markets ex-Japan are credit-and-insurance-hungry, growing in nominal terms at high single digits, and structurally undersupplied in commercial and specialty lines. Channelling Japanese underwriting capital and reinsurance capacity into local-currency premium at Asian pricing produces materially higher returns on capital than domestic deployment can generate. For multinational corporates placing Asian property and casualty programmes, MS&AD’s local underwriting presence is increasingly difficult to replicate through a non-Japanese carrier without a similar long-term Asian build-out.

Capital, solvency and the FSA’s quiet pressure

For most of the past decade MS&AD’s domestic non-life business has run at combined ratios in the mid-90s — profitable, but not extraordinarily so, and exposed to two large tail risks: Japanese natural catastrophe (earthquake, typhoon, flood) and US casualty reserve development through MS Amlin. The Financial Services Agency has progressively tightened its capital adequacy expectations, including the introduction of economic-value-based solvency requirements aligned with the international ICS framework. For MS&AD, this has meant disciplined run-off of cross-shareholdings in Japanese listed equities — historically a significant share of the group’s investment book — and reallocation into higher-yielding fixed income and offshore equities.

The cross-shareholding question is particularly delicate. Japanese non-life insurers historically held large cross-shareholdings in their corporate policyholders as part of the keiretsu relationship structure; the FSA has, since the mid-2010s, made clear that such holdings are no longer acceptable as either a capital management tool or a relationship-management tool. MS&AD has been steadily reducing the book, but the pace has been a source of investor frustration, and the group’s reported solvency margin remains highly sensitive to TOPIX moves through the cross-shareholding portfolio. For foreign analysts modelling the group, the cross-shareholding run-off schedule is one of the more important medium-term variables and is not always made explicit in headline disclosures.

What foreign reinsurance buyers and Asian entrants actually need to know

For a foreign reinsurer or Lloyd’s syndicate looking at Japanese non-life risk, MS&AD is most usefully understood as three different counterparties wearing one holding-company logo. Property catastrophe and large commercial risk on the MSI book is placed through the Mitsui Sumitomo Insurance reinsurance team in Tokyo, with a long-standing relationship culture and a preference for multi-year continuity over single-year price competition. Motor and personal lines risk on the Aioi Nissay Dowa book is handled separately — and is materially less reinsured on a quota-share basis, given the data-rich telematics underwriting — but does come to market for excess-of-loss catastrophe cover and specific large-commercial slices. The MS Amlin book in London is, for placement purposes, a fully separate Lloyd’s-market entity, and brokers typically engage it as they would any other top-tier syndicate rather than as a subsidiary of a Japanese parent.

For an Asian market entrant — say, a Korean or Singaporean group looking for a Japanese underwriting partner for joint programmes — the relevant entity is almost always MSI’s international division in Tokyo, which coordinates the group’s Asian carrier network and is the operational layer for cross-border product launches. Engaging directly at the holding-company level rarely produces useful traction; engaging through the relevant operating subsidiary, with a clear product and territory specification, almost always does.

The institutional culture, finally, deserves brief note. MS&AD has the most genuinely federated culture of the three Japanese non-life groups. Decisions on the MSI side are taken through a Mitsui-Sumitomo lineage of relationship-banking-style underwriting; decisions on the Aioi Nissay Dowa side are taken through a Toyota-supplier-style operational rigour; decisions on MS Amlin are taken in London on Lloyd’s-market timetables and Lloyd’s-market terms. The holding company aggregates capital and sets group-level solvency targets but does not impose uniform underwriting philosophy. For foreign counterparties, this is both the source of MS&AD’s resilience — each subsidiary keeps its native culture — and the source of its complexity.

FAQ

How is MS&AD structured, and which subsidiary should I actually engage?

MS&AD Insurance Group Holdings is a financial holding company listed on the Tokyo Stock Exchange as 8725, with five principal operating subsidiaries. The two domestic non-life carriers are Mitsui Sumitomo Insurance (MSI) — handling commercial lines, marine, fire and most non-Toyota motor — and Aioi Nissay Dowa Insurance (ADI), focused on motor, personal lines and the Toyota dealer channel. Mitsui Direct General Insurance is the direct-to-consumer brand. Mitsui Sumitomo Aioi Life Insurance and Mitsui Sumitomo Primary Life Insurance handle life and bank-channel annuities respectively. International specialty underwriting runs through MS Amlin at Lloyd’s. The right entity depends on the product and line of business — there is no single “MS&AD” counterparty for cross-border placements.

What did MS&AD actually buy when it acquired Amlin in 2016?

MS&AD acquired Amlin plc, a FTSE 250-listed insurance group, for approximately £3.5 billion in cash. The acquisition included Amlin’s Lloyd’s syndicate (one of the larger syndicates by premium income), its Bermuda reinsurance platform, and a continental European specialty insurance book based in the Netherlands. Post-acquisition the group was rebranded MS Amlin and integrated into MS&AD’s international underwriting structure. After several years of restructuring and adverse reserve development on legacy US casualty lines, the franchise has stabilised and the syndicate is currently a top-tier Lloyd’s market participant. For foreign brokers, MS Amlin is functionally a London-market entity backed by Japanese capital, not a Japanese carrier with a London office.

How does the Toyota partnership actually work, and is it exclusive?

Aioi Nissay Dowa Insurance is the principal insurance partner of Toyota Motor Corporation, with distribution through Toyota’s domestic dealer network and a global joint venture for telematics-based motor insurance. The relationship is structural rather than contractual — it operates within Japan’s keiretsu cross-shareholding and supplier-network logic — and while not literally exclusive, the practical effect is that the Toyota dealer channel sells Aioi Nissay Dowa motor policies as its default offering. The telematics joint venture, which began in Japan and has expanded into the UK, continental Europe, and selected emerging markets, gives Aioi Nissay Dowa exclusive insurance access to Toyota’s connected-car data feed, which is one of the largest underwriting-relevant data sets in the global auto industry.

How does MS&AD compare to Tokio Marine and SOMPO for foreign reinsurance buyers?

The three groups have roughly comparable domestic non-life market shares but materially different international profiles. Tokio Marine has the largest US specialty franchise, built through the acquisitions of Philadelphia, HCC and Pure, and is generally regarded as the most underwriting-disciplined. SOMPO has built an aggressive nursing-care and US specialty (Sompo International, formerly Endurance) franchise and is the most diversified into non-insurance businesses. MS&AD is the most London-market-focused through MS Amlin, the most tied into Japanese corporate keiretsu relationships, and the most operationally federated of the three. For Lloyd’s syndicates and London brokers, MS&AD is the most natural Japanese counterparty; for US specialty placements, Tokio Marine or SOMPO is more often the right entry point.

What is MS&AD’s exposure to Japanese natural catastrophe risk, and how is it reinsured?

As one of the three large Japanese non-life insurers, MS&AD carries material exposure to Japanese earthquake, typhoon and flood risk on both the MSI and ADI books. Earthquake coverage on personal lines is mostly written through the Japan Earthquake Reinsurance scheme (JER), a government-backed pool, which substantially mutualises the household earthquake risk across the industry and the state. Commercial earthquake and natural catastrophe risk above retention is placed through the global reinsurance market on excess-of-loss programmes renewed annually at April 1, the principal Japanese renewal date. MS&AD is one of the larger placements at every April 1 renewal and is closely watched by global reinsurers as a leading indicator of pricing for the broader Asian property catastrophe market.

Working with MS&AD

For foreign reinsurers, Lloyd’s syndicates, global brokers, multinational corporates and Asian-market entrants, MS&AD is the most international and the most structurally complex of the three Japanese non-life champions. Engaging the right subsidiary — MSI for commercial and reinsurance placements, Aioi Nissay Dowa for motor and personal lines including Toyota-related distribution, MS Amlin for London-market specialty risk — is the difference between a productive multi-product relationship and a six-month exercise in entity confusion. The group’s federated culture is a feature rather than a bug: each subsidiary keeps its native underwriting philosophy and its distribution moats, and the holding company aggregates capital without imposing a single risk-appetite framework.

Japonity helps overseas insurance, reinsurance and brokerage firms identify the right Japanese counterparty — MS&AD, Tokio Marine, SOMPO or the specialty mutual carriers — and build the introductions that turn an initial placement into a multi-year programme relationship. See our Business Matching page for how to start a structured engagement with MS&AD and its peers.

Related from Japonity — Japan’s non-life insurers

- Tokio Marine Holdings — Japan’s #1 non-life insurer and its US-led profit transformation

- SOMPO Holdings — The Bigmotor scandal, the senior-care pivot, and the Endurance trade

Want to source Japanese products beyond these company profiles? Japonity also runs a Japan Sourcing Hub — a research-grade catalogue of 1,185 verified Japanese food products and 200+ overseas EC stores, ready for B2B procurement.

Interested in Japanese business opportunities?

Whether you're looking for technology partners, engineering talent, or market insights — we can help connect you with the right Japanese organizations.

Get in Touch →