When Japan’s Financial Services Agency handed down a business improvement order to Sompo Japan Insurance in early 2024, the rebuke was less about a single rogue auto-repair partner than about the architecture of Japanese non-life insurance itself. The Bigmotor scandal — in which the country’s largest used-car retailer was found to have inflated collision-repair claims, allegedly with the tacit cooperation of insurance-company staff embedded inside its dealerships — was the loudest crisis in SOMPO Holdings’ fifteen-year history. Yet it landed at a strange moment for the group. While the domestic non-life business absorbed regulatory censure, SOMPO Care, the nursing arm acquired in 2015, had quietly grown into Japan’s largest private operator of senior-care facilities. And SOMPO International, the Bermuda-headquartered specialty insurer it bought from Endurance for approximately $6.3 billion in 2017, was contributing a rising share of group earnings. The company that emerged from the 2024 reckoning is no longer simply a Japanese motor insurer with overseas ambitions. It is a federation of three businesses — domestic P&C, global specialty, and senior care — held together by a holding structure that the parent must now prove can govern itself.

From NKSJ to SOMPO: the mergers that built a top-two non-life insurer

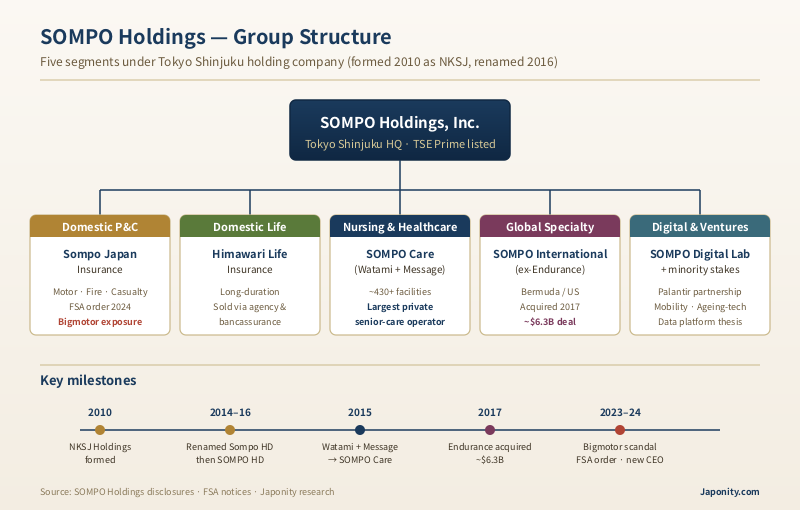

SOMPO Holdings traces its corporate identity to April 2010, when Sompo Japan Insurance and Nipponkoa Insurance combined their parent entities under the holding company NKSJ Holdings. The merger consolidated two mid-sized non-life carriers with overlapping motor and fire portfolios into Japan’s number-two property and casualty insurer, behind Tokio Marine Holdings and ahead — depending on the year and the metric — of MS&AD Insurance Group. The holding company was renamed Sompo Holdings in 2014, then restyled SOMPO Holdings in all-uppercase English in 2016 as part of a broader rebrand intended to telegraph a global, services-oriented identity rather than a domestic insurance conglomerate.

The operating non-life subsidiary, Sompo Japan Insurance, was itself the product of a 2014 internal merger between the legacy Sompo Japan and Nipponkoa operating entities, simplifying a structure that had carried duplicate underwriting teams, agency networks, and claims operations for four years post-merger. The Himawari Life insurance arm provides the group’s domestic life-insurance offering, sold predominantly through the same agency and bancassurance channels as the non-life parent. Group headquarters sit in Tokyo’s Shinjuku district, in a tower that — like rival Tokio Marine’s Marunouchi base — is itself a balance-sheet asset reflecting the historical accumulation of insurance reserves into Tokyo office real estate.

The three-way oligopoly: Tokio Marine, SOMPO, MS&AD

Japanese non-life insurance is, in practice, a three-firm market. Tokio Marine, SOMPO, and MS&AD between them write the overwhelming majority of domestic motor, fire, and casualty premium. The competitive shape of this oligopoly matters because it conditions every strategic choice each group makes — including, as the Bigmotor episode revealed, the distribution practices around which the entire industry’s claims experience is built.

| Group | Formed | Headquarters | Distinctive positioning |

|---|---|---|---|

| Tokio Marine Holdings | 2008 (TMNF heritage 1879) | Marunouchi, Tokyo | Largest non-life by premium; aggressive overseas M&A through Tokio Marine HCC, Philadelphia, Delphi |

| SOMPO Holdings | 2010 (as NKSJ) | Shinjuku, Tokyo | Senior-care diversification (SOMPO Care); SOMPO International specialty platform |

| MS&AD Insurance Group | 2010 | Marunouchi, Tokyo | Mitsui Sumitomo + Aioi Nissay Dowa; broad consumer non-life and overseas reinsurance footprint |

The three groups compete most fiercely in motor insurance, which remains the largest single non-life line in Japan by direct premium. Motor is also the line in which agency-based distribution — used-car dealers, repair shops, automobile-sales chains — has historically wielded outsized influence, because the dealer who sells the car typically writes the insurance policy that goes with it. That distribution architecture is the context in which Bigmotor became a problem not only for SOMPO Japan but for the industry as a whole.

The Bigmotor scandal: when distribution turned into capture

Bigmotor was, until 2023, Japan’s largest used-car retailer by store count, with a vertically integrated business that included sales, financing, body-shop repairs, and — critically — insurance-agency operations. Investigations that became public during 2023 alleged that Bigmotor staff had systematically inflated collision-damage estimates submitted to non-life insurers, in some cases physically damaging vehicles beyond the original loss to justify higher payouts. The scheme implicated all three major non-life groups to varying degrees, but SOMPO Japan attracted the most regulatory attention because of the unusually deep operational integration between its claims-handling staff and Bigmotor’s repair operations, including seconded employees working inside dealership locations.

In January 2024, Japan’s Financial Services Agency issued a business improvement order to Sompo Japan Insurance under the Insurance Business Act, citing failures in claims-management governance and inadequate response when internal whistleblowers raised concerns about Bigmotor practices. Kengo Sakurada, who had led the group since 2016 and was the public face of SOMPO’s transformation strategy, stepped back from executive responsibility, with Mikio Okumura assuming the group CEO role in 2024. The episode triggered a broader industry conversation — pushed by the FSA — about whether the agency-distribution model that built Japanese non-life insurance had structurally encouraged the kind of regulatory capture Bigmotor exemplified.

SOMPO Care: how an insurer became Japan’s largest private nursing operator

While the 2024 scandal dominated headlines, the more consequential long-run story for SOMPO is the senior-care business it began building in 2015. In that year SOMPO acquired Watami’s nursing-home subsidiary, then completed a takeover of Message Co., one of Japan’s largest publicly listed senior-care operators. The combined business was rebranded SOMPO Care and now operates approximately 430 senior-care facilities across Japan — paid private homes, group homes, and home-care service centres — making it the country’s largest private-sector operator of senior accommodation by facility count.

The strategic logic was demographic. Japan’s population aged 65-plus crossed 29 percent in the mid-2020s, and the nation’s long-term care insurance system — kaigo hoken — guarantees both demand and a defined public-payor reimbursement structure. For a non-life insurer staring at a shrinking motor-insurance pool (driven by population decline, ageing drivers exiting the market, and the gradual encroachment of advanced driver-assistance systems on collision frequency), senior care offered a way to redeploy underwriting capital and distribution relationships into a service business with durable, government-supported revenue. SOMPO Care’s revenue base is not equity-volatile in the way that catastrophe reinsurance is; nor is it exposed to the agency-distribution governance risks that ended up costing SOMPO Japan its reputation in 2024.

The senior-care arm has also become a strategic data and innovation asset. SOMPO has invested heavily in technology partnerships — including a publicised tie-up with Palantir Technologies to deploy data infrastructure across the nursing-care operations — pitching itself as a “real-data platform” for the ageing-society economy. Whether the data thesis ultimately generates outsized returns is unproven; but as a hedge against domestic motor stagnation, the diversification is already paying off in EBITDA terms.

SOMPO International: the Endurance acquisition and the offshore specialty bet

The other leg of SOMPO’s three-legged stool is global specialty insurance and reinsurance, built around the 2017 acquisition of Endurance Specialty Holdings for approximately $6.3 billion. Endurance, headquartered in Bermuda with major operations in the United States, gave SOMPO a Lloyd’s syndicate, an agriculture-insurance franchise (Endurance had built a meaningful US crop-insurance book), and a casualty and professional-lines presence in the US specialty market. The platform was rebranded SOMPO International in 2017 and now sits alongside Sompo Japan and SOMPO Care as one of the three primary earnings engines.

The Endurance deal was the largest overseas acquisition by a Japanese non-life insurer at the time it was announced, comparable in strategic intent — if not in price — to Tokio Marine’s earlier purchases of HCC Holdings and Philadelphia Consolidated. The underlying thesis across all three Japanese majors has been the same: domestic premium pools are flat to declining, capital is plentiful, the yen has historically been cheap relative to US-dollar earnings, and US specialty insurance offers underwriting margins unavailable in saturated Japanese motor. The risk, of course, is that overseas acquisitions concentrate Japanese balance sheets in catastrophe-exposed lines — hurricane, wildfire, severe convective storm — that periodically produce loss years uncorrelated with the domestic book.

SOMPO International’s contribution to group profit has grown meaningfully through the late 2010s and into the 2020s, particularly as the post-2020 hard market in global specialty and reinsurance lifted underwriting margins. The business has also given SOMPO a credible recruiting platform outside Japan and a corporate-governance reference point — Bermuda regulatory standards, US public-company-style disclosure — that may, over time, exert upward pressure on governance at the Japanese parent.

Segment economics: where the earnings actually come from

The simplest way to read SOMPO’s group structure is as a portfolio of five segments, each with distinct economics, regulatory regimes, and growth profiles.

| Segment | Operating entity | Economic character |

|---|---|---|

| Domestic P&C | Sompo Japan Insurance | Largest premium contributor; motor + fire dominant; flat-to-declining domestic pool |

| Domestic Life | Himawari Life Insurance | Long-duration liabilities; sold through non-life agencies and bancassurance |

| Nursing & Healthcare | SOMPO Care + Cedar (group-home network) | Approximately 430+ facilities; kaigo-hoken reimbursement base; demographic tailwind |

| SOMPO International | Bermuda/US-domiciled specialty & reinsurance | Catastrophe-exposed; benefited from post-2020 hard market |

| Digital & new ventures | SOMPO Digital Lab + minority stakes | Palantir partnership, mobility-insurance experiments, ageing-tech investments |

The five-segment view also clarifies what the Bigmotor episode actually threatened. It was a governance and reputational hit concentrated in the Domestic P&C segment, but the diversification afforded by Nursing & Healthcare and SOMPO International meant the consolidated balance sheet absorbed the regulatory penalty without strategic disruption to the other earnings engines. That insulation is itself a vindication — quiet and partial — of the diversification thesis Sakurada pursued through the late 2010s.

Governance after Bigmotor: what the FSA wants

The 2024 business improvement order was specific in its critique. Japan’s FSA was not merely punishing a claims-fraud scheme; it was signalling that the agency-distribution model embedded across Japanese non-life insurance — wherein the same firm sells the policy, settles the claim, and in many cases owns or operates the repair facility — produced conflicts of interest the major groups had failed to manage. The Insurance Business Act improvement order required SOMPO Japan to overhaul claims-management governance, restructure relationships with major agency partners, and establish independent oversight of distribution conflicts.

The post-Bigmotor environment has accelerated several industry-wide reforms: separation of underwriting from claims-handling staff in dealer-embedded operations, mandatory disclosure of large agency relationships, and tightened whistleblower-protection requirements. Whether these reforms structurally change the economics of motor insurance distribution — or merely add compliance overhead — is the open question for the late-2020s. Under Mikio Okumura, SOMPO has publicly committed to a “rebuilding trust” agenda; the next two FSA review cycles will determine whether that commitment translates into measurable governance improvement.

The pivot question: insurer, care provider, or holding company?

The most interesting strategic question facing SOMPO Holdings under Okumura is identity. The group is large enough in nursing and healthcare that, on certain measures, it is no longer accurately described as an “insurer that also does care” — it is a care operator that also writes insurance. SOMPO International, meanwhile, has reached a scale where its specialty-insurance underwriting decisions are increasingly governed by Bermuda regulatory norms rather than Japanese FSA conventions. And the digital ventures, while still small relative to the consolidated balance sheet, anchor a narrative SOMPO has consistently sold to investors: that the group’s long-run value lies less in underwriting cycles than in becoming an “infrastructure provider for the ageing society.”

The three identities are not mutually exclusive, but they imply different capital-allocation priorities. An insurance-first SOMPO would prioritise underwriting discipline and dividend stability. A care-first SOMPO would invest aggressively in facility expansion, technology platforms, and adjacent healthcare services. A holding-company SOMPO would treat all three segments as portfolio assets to be optimised for total return. The 2024 crisis bought Okumura time to make that choice explicit — and the answer, when it arrives, will shape the next decade of competitive dynamics across the three-firm Japanese non-life oligopoly.

FAQ

When was SOMPO Holdings formed and how did it get its current name?

The group was formed in April 2010 as NKSJ Holdings, through the combination of Sompo Japan Insurance and Nipponkoa Insurance. It was renamed Sompo Holdings in 2014 and restyled SOMPO Holdings in uppercase English in 2016 as part of a broader global rebrand.

What was the Bigmotor scandal and how did it affect SOMPO?

Bigmotor, formerly Japan’s largest used-car retailer, was found in 2023 to have systematically inflated collision-repair claims submitted to non-life insurers, in some cases damaging vehicles to justify higher payouts. SOMPO Japan was singled out due to the deep operational integration between its claims staff and Bigmotor dealerships. The FSA issued a business improvement order in January 2024, and Mikio Okumura succeeded Kengo Sakurada as group CEO in 2024.

What is SOMPO Care and how big is it?

SOMPO Care is the group’s senior nursing and healthcare subsidiary, built from the 2015 acquisitions of Watami’s nursing arm and Message Co. It operates approximately 430+ facilities across Japan, making it the country’s largest private-sector operator of senior accommodation by facility count.

What is SOMPO International and how did SOMPO acquire it?

SOMPO International is the group’s global specialty insurance and reinsurance platform, headquartered in Bermuda with significant US operations. It was acquired in 2017 through the purchase of Endurance Specialty Holdings for approximately $6.3 billion and rebranded SOMPO International the same year.

How does SOMPO compare to Tokio Marine and MS&AD?

SOMPO is generally Japan’s number-two non-life insurer by premium, behind Tokio Marine Holdings and ahead — depending on the year and metric — of MS&AD Insurance Group. All three were formed through holding-company mergers in 2008-2010 and now compete across domestic motor and fire insurance, overseas specialty acquisitions, and adjacent service-business diversification.

Working with SOMPO

For companies exploring partnerships with SOMPO Holdings — whether in non-life and life insurance distribution, senior-care technology and operations, global specialty underwriting through SOMPO International, or digital and data-platform ventures — Japonity’s Business Matching service connects qualified counterparties to the right corporate-development and partnership teams across the group’s Japanese, Bermudian, and US operations. Submit a partnership brief to begin a structured introduction process.

Related from Japonity — Japan’s non-life insurers

- Tokio Marine Holdings — Japan’s #1 non-life insurer and its US-led profit transformation

- MS&AD Insurance Group — Japan’s most internationally-built non-life insurer

Want to source Japanese products beyond these company profiles? Japonity also runs a Japan Sourcing Hub — a research-grade catalogue of 1,185 verified Japanese food products and 200+ overseas EC stores, ready for B2B procurement.

Interested in Japanese business opportunities?

Whether you're looking for technology partners, engineering talent, or market insights — we can help connect you with the right Japanese organizations.

Get in Touch →