In April 2014, the bell rang again at the Tokyo Stock Exchange for Seibu Holdings (TSE: 9024), ending an eight-year private interregnum under New York-based Cerberus Capital Management that had begun with one of the most spectacular falls in postwar Japanese corporate history. Yoshiaki Tsutsumi — for years Japan’s richest man, according to Forbes — had been arrested in 2005 on securities-law violations; his Seibu Railway had been delisted; and Cerberus had stepped in to recapitalise the group, restructure its sprawling hotel and resort book, and ultimately float it back on the public markets. A decade later, Seibu Holdings sold 31 Prince Hotels properties to Singapore’s GIC for roughly JPY 150 billion (around USD 1.6 billion) in 2022, divested the Seibu and Sogo department stores to Fortress in 2023 for about JPY 250 billion, and refocused around the western-Tokyo rail corridor, Prince Hotels as an asset-light operator, and the Saitama Seibu Lions of Nippon Professional Baseball. The Kobayashi rail-and-everything-else playbook still anchors the group — but the balance sheet behind it looks unrecognisable from the one Yoshiaki Tsutsumi built.

The Tsutsumi empire: from Karuizawa land to the richest man in the world

Modern Seibu begins with Yasujiro Tsutsumi (1894–1964), a politically connected entrepreneur from rural Shiga prefecture who built his fortune by acquiring distressed mountain and lakeside land in the 1920s and 1930s — Karuizawa, Hakone, the Izu peninsula — and developing it for the rising urban middle class. Yasujiro acquired the Musashino Railway (the predecessor of today’s Seibu Ikebukuro Line) in 1940 and the old Seibu Railway in 1945, fusing them into what became the modern Seibu Railway in 1946. He served as Speaker of the House of Representatives in the early 1950s and assembled, through the postwar decades, the most personally controlled large business group in Japan.

On Yasujiro’s death in 1964, the empire split between two sons by different mothers. The elder, Seiji Tsutsumi (1927–2013), inherited the Seibu Department Store side of the house — a small Ikebukuro retail outlet at the terminus of the Seibu line — and turned it into Saison Group, the most culturally influential retailer of late-twentieth-century Japan (Seibu Department Store, Parco, Muji, Loft, FamilyMart in its formative years, the Seibu Saison Hotel chain, and a publishing arm). The younger, Yoshiaki Tsutsumi (1934–2020), inherited the railway, the hotels and the Karuizawa land — and built from these the asset-heavy Seibu Group that this article concerns.

Through the 1980s and into the 1990s, Yoshiaki’s Seibu Group ran Prince Hotels, the Seibu Lions baseball team (moved from Fukuoka to Tokorozawa in 1979), Seibu Railway, and a private real-estate book whose true value was famously opaque. Forbes ranked Yoshiaki the wealthiest individual in the world for four consecutive years in the late 1980s, on estimates of group land value that, in retrospect, captured the absolute peak of the bubble economy.

2004–2006: arrest, delisting, Cerberus

The unwinding came in 2004. An investigation by Japan’s securities regulators found that the Seibu group had under-reported the true Tsutsumi family shareholding in Seibu Railway in its annual securities filings for years, in violation of disclosure rules. In March 2005, Yoshiaki Tsutsumi was arrested. The Tokyo Stock Exchange delisted Seibu Railway in December 2004, citing the false disclosure. Yoshiaki was convicted in 2005 and received a suspended prison sentence; he resigned from all group positions and would never return to operating control.

By 2006, the group needed both fresh capital and credible outside oversight. Cerberus Capital Management, the New York private-investment firm, led a consortium that ultimately took a controlling stake — at peak roughly a third of Seibu Holdings, the new holding company formed to consolidate the railway, hotel and real-estate operations. Over the following eight years Cerberus pushed for asset disposals, governance reforms, and an eventual relisting. The relationship was not always smooth: Cerberus publicly pressed for additional rail-line closures and faster hotel disposals, and the Japanese government and Saitama prefecture pushed back. But in April 2014, Seibu Holdings completed its initial public offering on the Tokyo Stock Exchange, with Cerberus selling down its stake (and continuing to exit over subsequent years).

The post-relisting Seibu Holdings that emerged is a fundamentally different group from the one Yoshiaki Tsutsumi ran. Headquartered in Tokyo’s Toshima ward (the Ikebukuro terminus), it discloses cleanly across reporting segments, has independent directors, runs a conservative dividend policy, and treats its hotel book as something to monetise rather than to hoard.

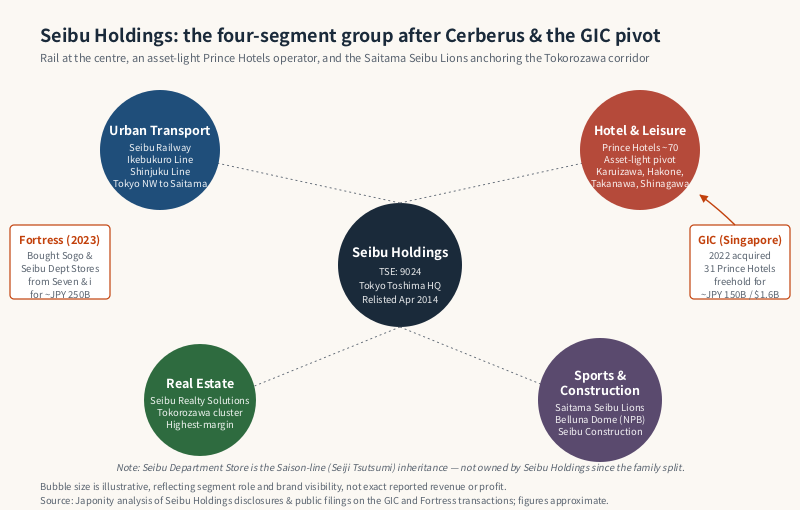

The four-segment group today

Seibu Holdings reports across four core segments. Together they generate annual consolidated revenue in the range of JPY 450–500 billion, with Urban Transportation and Real Estate providing stable cash flow and Hotel & Leisure providing growth optionality through the asset-light pivot.

| Segment | Core businesses | Profile |

|---|---|---|

| Urban Transportation & Regional Business | Seibu Railway (Ikebukuro Line, Shinjuku Line, Yamaguchi Line); bus operations across western Tokyo and Saitama | Backbone of the group; commuter-heavy with Saitama suburb traffic; stable cash flow |

| Hotel & Leisure | Prince Hotels (now operating ~70 properties, of which 31 are owned by GIC and leased back); golf courses, ski resorts, Karuizawa estate | Reshaped 2022 by the GIC transaction; pivot from owner-operator to operator-led |

| Real Estate | Seibu Realty Solutions; residential and office development along the rail corridor; Tokorozawa redevelopment | Highest-margin segment; concentrated in Tokyo northwest and central Saitama |

| Construction & Other | Seibu Construction; sports and entertainment (Saitama Seibu Lions of NPB) | Lions are housed here as a sports business; modest direct margin, large brand value |

Notably absent from the segment table is the Seibu and Sogo department-store business. That is because Seven & i Holdings — which had acquired the chain in 2006 from the post-Saison restructuring — sold it in September 2023 to a Fortress Investment Group-led consortium for approximately JPY 250 billion. Although the Seibu Department Store brand still sits at the Ikebukuro terminus served by the Seibu Ikebukuro Line, it is no longer part of either Seven & i or, indeed, Seibu Holdings. The naming overlap is a relic of the Tsutsumi family split sixty years ago, not a current corporate relationship.

The 2022 GIC transaction: an asset-light pivot in real time

The single most consequential corporate transaction in Seibu’s post-relisting history is the February 2022 sale of 31 Prince Hotels properties to GIC, the Singapore sovereign wealth fund, for approximately JPY 150 billion (around USD 1.6 billion at the prevailing exchange rate). Under the deal structure, GIC acquired the real-estate freehold of properties including the Grand Prince Hotel Takanawa, the Grand Prince Hotel New Takanawa, the Prince Park Tower Tokyo, Karuizawa Prince Hotel and Shinagawa Prince Hotel; Seibu Holdings continued to operate the properties under long-term lease arrangements through its Prince Hotels subsidiary.

The strategic logic is straightforward and increasingly common across Japanese hospitality: a domestic operator with deep operating know-how but a balance sheet weighed down by aging real-estate carrying values monetises the freehold to a global sovereign or institutional capital partner whose cost of capital is materially lower, then continues to run the properties under a master lease. For Seibu, the transaction delivered cash to deleverage, freed management attention to focus on operations and brand, and crystallised what had been an opaque legacy of Tsutsumi-era land holdings into market-priced value.

For GIC, the trade fits a pattern of long-duration Japanese hospitality real-estate accumulation, taking advantage of the long-term yield gap between Japanese property and global benchmarks. The Prince portfolio anchors a core hospitality position in one of the world’s largest inbound tourism markets.

The transaction does not end Seibu’s hotel exposure — Prince Hotels still operates roughly 70 properties in total. But the directional shift is clear: future growth is being engineered as an asset-light operator with brand, loyalty and operational capability, rather than as the asset-heavy resort empire that Yoshiaki Tsutsumi built.

The Ikebukuro–Shinjuku–Saitama corridor: Seibu’s home market

Seibu Railway operates two main commuter trunk lines out of Tokyo and a handful of branches. The Ikebukuro Line runs roughly 57 kilometres from Ikebukuro Station — the third-busiest railway station in Japan by daily passenger volume — northwest into Saitama prefecture, terminating at Agano in the Chichibu foothills. The Shinjuku Line runs from Seibu-Shinjuku, on the western edge of the Shinjuku terminal complex, west and north-west through Tokorozawa and on to Hon-Kawagoe in Saitama. The Yamaguchi Line, a short attraction loop, serves Seibu’s Toshimaen-area assets and the leisure facilities at Seibukyujo-mae adjacent to the Lions’ stadium.

Tokorozawa — a city of roughly 340,000 in central-southern Saitama prefecture — sits at the junction of the Ikebukuro and Shinjuku lines and functions as the operational heart of the Seibu Group: corporate offices, the Saitama Seibu Lions’ Belluna Dome (the team’s home stadium), and a major redevelopment cluster including the Tokorozawa Sakura Town mixed-use complex co-developed with Kadokawa, the publisher and media group. The Tokorozawa corridor is, in effect, Seibu’s Umeda — the concentrated real-estate node where rail, retail, residential and entertainment assets reinforce one another along the Kobayashi playbook.

Compared with the southwest-Tokyo corridor that Tokyu dominates around Shibuya, the Seibu corridor is demographically less wealthy and culturally less fashion-forward; it is the railway of the bedroom suburbs of northwest Tokyo and central Saitama, of postwar middle-class developments, of Studio Ghibli (whose museum sits along the Seibu Tamagawa line). It is also, increasingly, the corridor along which Tokyo’s housing-affordability pressure pushes new commuter demand, with redevelopment activity around Nerima, Ekoda, Shakujii-koen and Tokorozawa station areas accelerating through the 2020s.

Saitama Seibu Lions: the cultural anchor

The Saitama Seibu Lions, founded in 1949 in Fukuoka as the Nishitetsu Clippers, were acquired by Yoshiaki Tsutsumi in 1978 and relocated to Tokorozawa for the 1979 season. Renamed first the Seibu Lions and, from 2008, the Saitama Seibu Lions (in a gesture of regional identity that mirrored similar rebrandings by other NPB teams), the franchise plays its home games at Belluna Dome (formerly the Seibu Dome and the Seibu Lions Stadium), an unusual semi-open-air ballpark that holds approximately 31,000.

From a financial reporting standpoint the Lions, like the Hanshin Tigers within Hankyu Hanshin or the Yomiuri Giants within Yomiuri, generate modest direct revenue and modest margin. The strategic value is indirect: ticket-led rail ridership on the Yamaguchi Line and Ikebukuro Line into Tokorozawa, brand identification with Saitama prefecture (a vital but historically under-celebrated political and economic counterparty for the group), and a portfolio of stadium-adjacent leisure assets that anchor weekend traffic on what would otherwise be a one-way commuter network.

For overseas businesses, the Lions are also a route into Saitama-region sponsorship, retail activations and inbound-tourism collaborations that are surprisingly under-tapped relative to their Tokyo-21-ward equivalents.

Peer comparison: how Seibu sits among Tokyo’s private rail conglomerates

| Group | Core corridor | Distinctive assets | Strategic posture |

|---|---|---|---|

| Seibu Holdings (9024) | Tokyo northwest (Ikebukuro/Shinjuku) into Saitama | Saitama Seibu Lions, Prince Hotels (asset-light post-GIC), Karuizawa estate | Slimmed and refocused post-Cerberus; asset-light hotel pivot |

| Tokyu Corporation (9005) | Tokyo southwest (Shibuya/Yokohama) | Shibuya redevelopment, Tokyu Department Store, Tokyu Hotels | Asset-heavy; Tokyo urban-renewal pure play |

| Tobu Railway (9001) | Tokyo northeast (Asakusa/Skytree) into Saitama, Tochigi, Gunma | Tokyo Skytree, Nikko tourism cluster, Tobu Department Store | Tourism-heavy with Nikko inbound exposure |

| Keio Corporation (9008) | Tokyo west (Shinjuku) to Hachioji and Takao | Keio Department Store, Keio Plaza Hotel, urban real-estate | Commuter-heavy with smaller diversification |

| Odakyu Electric Railway (9007) | Tokyo west (Shinjuku) to Odawara and Hakone | Hakone tourism cluster, Odakyu Department Store | Tourism + commuter balance |

Among Tokyo’s private-rail conglomerates, Seibu sits between Tokyu — which is more asset-heavy and more retail-led — and Odakyu, which is more tourism-led around Hakone. Seibu’s distinctive combination is its NPB franchise, its post-GIC asset-light hotel platform, and its concentrated Saitama exposure.

Governance and the post-Cerberus chapter

Seibu Holdings is led by a Tokyo-based board with a meaningful complement of independent directors, a legacy of the Cerberus-era reforms. Takashi Goto served as president and group chief executive across much of the 2010s and into the early 2020s, overseeing both the relisting and the GIC transaction; the succession to current president Tatsuya Goto took place in the mid-2020s and continues the strategic direction set during the asset-light pivot. The chairman role and the board structure reflect Japanese listed-company norms but with a markedly higher level of transparency than the Tsutsumi-era group ever exhibited.

The strategic questions facing Seibu through the late 2020s sit at the intersection of three trends. First, inbound tourism to Japan continues to run well above pre-pandemic levels, with the weak yen sustaining a structural tailwind for hospitality operators — and Seibu’s Prince brand, with its concentration of properties in Tokyo, Karuizawa, Hakone and Kyoto, is well positioned to benefit. Second, Saitama’s housing and commercial real-estate market is benefiting from Tokyo affordability pressure, and the Tokorozawa redevelopment cluster is a multi-decade story. Third, the post-GIC operating partnership requires Seibu to perform as a hotel operator in a way that the Yoshiaki Tsutsumi-era group never had to demonstrate — its loyalty programme, distribution, revenue management and brand investment will be tested against asset-light global operators in a way the legacy business was insulated from.

For overseas businesses, Seibu Holdings is the natural counterparty for hospitality partnerships seeking Prince Hotels distribution, for retail and consumer brands targeting the northwest-Tokyo and Saitama corridors, for sports sponsorship through the Lions, and for real-estate development along one of the major commuter arteries that still has meaningful redevelopment landbank.

FAQ

Q1. Are Seibu Holdings and the Seibu Department Store the same company?

No. The Seibu Department Store was the inheritance of Seiji Tsutsumi (elder brother), who built it into the Saison Group. After Saison’s restructuring, the department-store business was sold to Seven & i Holdings in 2006 and then on to a Fortress-led consortium in September 2023 for approximately JPY 250 billion. The Seibu Department Store at Ikebukuro is therefore not currently owned by Seibu Holdings, despite sharing the Tsutsumi-era heritage and the Ikebukuro location.

Q2. Why was Seibu Railway delisted in 2004 and then relisted in 2014?

Seibu Railway was delisted in December 2004 after the Tokyo Stock Exchange determined that the company had under-reported the Tsutsumi family shareholding in its annual securities filings for years. Yoshiaki Tsutsumi, the longtime group head, was arrested in March 2005 and convicted of securities-law violations. From 2006, a consortium led by Cerberus Capital Management took a controlling stake and recapitalised and restructured the group; Seibu Holdings then completed its IPO on the Tokyo Stock Exchange in April 2014.

Q3. What did the 2022 GIC transaction actually involve?

In February 2022, Seibu Holdings sold the freehold of 31 Prince Hotels properties — including the Grand Prince Hotel Takanawa, Prince Park Tower Tokyo, Shinagawa Prince Hotel and Karuizawa Prince Hotel — to Singapore’s GIC sovereign wealth fund for approximately JPY 150 billion (around USD 1.6 billion). Prince Hotels continues to operate the properties under long-term lease, pivoting from an asset-heavy owner-operator model toward an asset-light operator model.

Q4. Does Seibu Holdings still own the Saitama Seibu Lions?

Yes. The Saitama Seibu Lions baseball team is owned by Seibu Holdings and is operated as part of the group’s Construction & Other segment, which houses the sports and entertainment business. The team plays its home games at Belluna Dome in Tokorozawa.

Q5. How can a non-Japanese company engage with Seibu Holdings?

Each segment has its own commercial team — Prince Hotels for hospitality distribution and brand partnerships, Seibu Railway and Seibu Realty Solutions for real-estate and station-area redevelopment, and the Lions organisation for sports sponsorship and Saitama-region activations. Japonity can help map the appropriate counterparty within the group and prepare a Japanese-language briefing to support a first meeting.

Working with Seibu Group

Seibu Holdings is the anchor commercial counterparty along Tokyo’s northwest corridor into Saitama prefecture, and an increasingly visible hospitality operator across Japan through the Prince Hotels brand. Hotel partners seeking distribution and loyalty access, retail and consumer brands targeting the Ikebukuro and Tokorozawa catchments, real-estate co-developers evaluating station-area sites, and sports sponsors approaching the Saitama Seibu Lions all have natural reasons to engage with the group.

If you are exploring a hospitality partnership, retail or real-estate negotiation, sports sponsorship, or inbound-tourism collaboration with any part of the Seibu Group, Japonity can help you map the right entity, prepare a Japanese-language briefing, and structure a first meeting. Start at /business-matching/.

Related from Japonity — Japan’s passenger railways & rail conglomerates

- JR East — The world’s largest railway by passengers — and Japan’s biggest station-retail empire

- JR Central — The Tokaido Shinkansen monopoly and the maglev moonshot

- Tokyu Corporation — The Shibuya-redeveloping rail conglomerate

- Hankyu Hanshin Holdings — Kansai’s railway-real-estate-entertainment empire

- Kintetsu Group Holdings — Japan’s longest private railway — Osaka-Nara-Ise-Nagoya

Want to source Japanese products beyond these company profiles? Japonity also runs a Japan Sourcing Hub — a research-grade catalogue of 1,185 verified Japanese food products and 200+ overseas EC stores, ready for B2B procurement.

Interested in Japanese business opportunities?

Whether you're looking for technology partners, engineering talent, or market insights — we can help connect you with the right Japanese organizations.

Get in Touch →