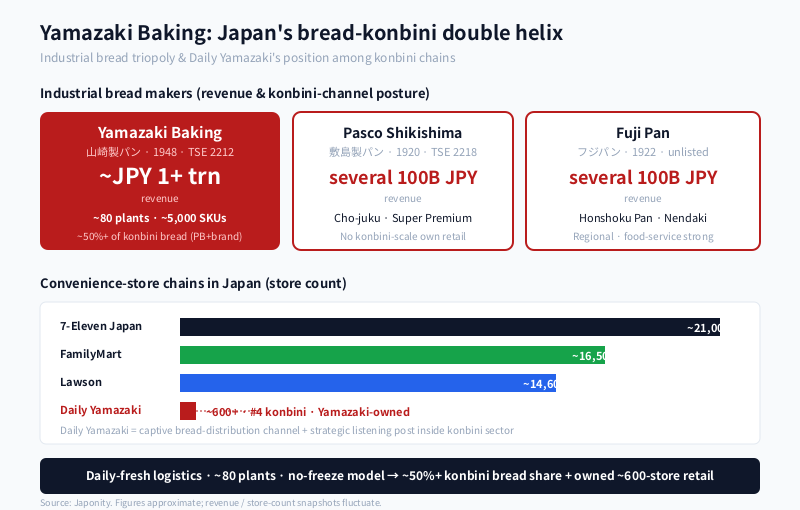

Yamazaki Baking Co., Ltd. (山崎製パン株式会社) is the company most Japanese consumers never think about and yet eat from almost every day. By sales it is Japan’s largest bread maker, its largest Western-style confectionery producer, and one of the world’s biggest baking groups, with revenue exceeding approximately JPY 1 trillion across a portfolio of roughly 5,000 SKUs. It runs about 80 production sites and a daily-delivery logistics network that pushes fresh bread onto retail shelves within hours of baking — supplying, by widely cited industry estimates, on the order of half of all bread products sold through Japan’s convenience-store chains, including substantial volumes of private-label SKUs for 7-Eleven, FamilyMart and Lawson. It is also, less obviously, a retailer in its own right: Daily Yamazaki, the company’s small-format convenience-store chain, operates approximately 600+ stores nationwide as Japan’s number-four konbini brand — small enough to be a rounding error against 7-Eleven’s footprint, large enough to function as both a captive distribution channel and a strategic listening post inside the convenience-store sector.

The baker most Japanese consumers eat from every day

Yamazaki was founded in 1948 in Ichikawa City, Chiba Prefecture, by Nobuhiro Iijima (飯島藤十郎), under the original name Iijima Bakery before being renamed Yamazaki Baking the same year. Headquartered today in Chiyoda-ku, Tokyo, and listed on the Tokyo Stock Exchange Prime market under code 2212, the company grew over seven decades from a single Chiba bakery into a national baking group whose name is invisible on many of the products it makes — because so many sit on retail shelves under a private-label banner rather than the Yamazaki brand.

The portfolio is best understood as four overlapping businesses on a single logistics backbone. Yamazaki bakes bread — sliced shokupan (Royal Bread, Double Soft), table rolls, baguettes and croissants — at industrial scale; produces sweetened breads (kashi-pan) and the confectionery staples of Japanese childhood (anpan, cream-pan, melon-pan, jam-pan, donuts); runs Western-style cake and pastry production for retail and food-service; and operates its own retail formats — Daily Yamazaki, Vie de France, Yamazaki Café and the Vie de France de Paris joint venture. Beneath all of this sits a logistics operation engineered around a single principle non-negotiable in Japanese fresh-bread retail: deliver daily, deliver fresh, never freeze.

From a single Chiba bakery to a JPY ~1 trillion group

The founding story tracks the post-war reconstruction of Japanese food retail. Iijima opened the original bakery in 1948 when wheat-based foods were being actively promoted in the post-occupation diet, school-lunch programmes were standardising bread consumption in classrooms, and Western-style bakery products were transitioning from luxury to staple. Yamazaki rode that demand curve aggressively in the 1950s and 1960s, building progressively larger plants, standardising production around sliced shokupan and kashi-pan, and acquiring or partnering with regional bakeries to extend its geographic footprint.

By the 1970s, the company had diversified into Western-style confectionery and begun experimenting with retail formats. Vie de France, launched as a French-style in-store bakery concept, would grow into a chain of approximately 150+ outlets across Japan, anchored inside major train stations and shopping centres. The Daily Yamazaki convenience-store format followed, leveraging the existing bread-distribution network to create a small-store retail concept that doubled as a captive sales channel. By the 2000s, Yamazaki was running approximately 80 production sites and listing among the country’s largest food-manufacturing groups by revenue. It is today led by chairman Nobuyuki Iijima (飯島延浩), the founder’s son, with day-to-day management under president Hisao Iijima (subject to verification against the latest disclosure) — a family-influenced governance structure unusually durable for a company of its scale, and one that has kept Yamazaki tightly focused on bread, confectionery and the logistics that move them.

The konbini supply chain: why ~50% of convenience-store bread is Yamazaki

The single most consequential fact about Yamazaki — and the one least visible to consumers — is its role inside Japan’s convenience-store supply chain. Industry estimates widely place Yamazaki’s share of konbini bread and bread-adjacent products (sliced bread, table rolls, sweet breads, sandwiches and pastries combined) at approximately 50% or more, counting both Yamazaki-branded SKUs and private-label production for the convenience-store chains’ own brands. For Seven Premium bread, Family Mart Collection bread and Lawson Select bakery items, Yamazaki is often the manufacturer whose name does not appear on the packaging.

That position is the product of three structural advantages difficult for any competitor — domestic or foreign — to replicate at speed. First, geographic plant density: approximately 80 production sites mean almost any konbini distribution centre is within a few hours’ truck-run of a Yamazaki bakery, supporting the daily-delivery cadence konbini buyers demand. Second, SKU breadth: roughly 5,000 active SKUs across bread, confectionery and pastry give Yamazaki the manufacturing flexibility to absorb a national private-label programme without disrupting its branded business. Third, a non-negotiable daily-fresh, no-freeze logistics model that aligns precisely with the konbini sector’s refusal to compromise on shelf freshness.

| Segment | Brands / formats | Approx. SKU scale | Strategic role |

|---|---|---|---|

| Sliced & table bread | Royal Bread, Double Soft, lunch rolls | Several hundred SKUs | Volume foundation; konbini PB anchor |

| Sweetened bread (kashi-pan) | Anpan, cream-pan, melon-pan, jam-pan | ~1,000+ SKUs | Daily-fresh konbini and supermarket category |

| Western confectionery | Donuts, Western cakes, pastries | Several hundred SKUs | Seasonal & gifting; Vie de France inputs |

| Convenience store retail | Daily Yamazaki, Yamazaki Daily Store | ~600+ stores | Captive channel; #4 konbini in Japan |

| In-store bakery & café | Vie de France, Vie de France de Paris, Yamazaki Café | ~150+ outlets | French-style premium positioning |

Private-label margins per unit are typically thinner than branded equivalents, but the volume is large, the cadence is predictable, and the relationship gives Yamazaki real-time visibility into shifting demand across approximately 55,000 konbini stores nationwide — data fed back into branded R&D and SKU rationalisation, and one of the quiet reasons the company has been so difficult to displace.

Daily Yamazaki: the #4 konbini that exists for two reasons

Among Japan’s convenience-store chains, Daily Yamazaki is unambiguously the smallest of the major banners — approximately 600+ stores against 7-Eleven Japan’s roughly 21,000, FamilyMart’s roughly 16,500 and Lawson’s roughly 14,600. The footprint is small enough that Daily Yamazaki is sometimes omitted from headline market-share tables, yet it is consistently described as Japan’s number-four convenience-store chain when one looks past the top three. The interesting question is not why Daily Yamazaki is small — it is why it exists at all.

There are two answers, and both matter. The first is that Daily Yamazaki is, by design, a captive distribution channel for the parent’s bakery business. Where the big-three konbini operate as buyers in a competitive bread-procurement market, Daily Yamazaki is a Yamazaki-owned retail surface where the company controls shelf allocation, in-store baking and the daily refresh cycle directly. The standalone economics of any individual store matter less than the aggregate role of the chain as a 600+-location showcase and absorbent for Yamazaki SKUs.

The second answer is that Daily Yamazaki functions as a strategic listening post inside the konbini sector. Operating one’s own convenience-store chain — however modestly sized — means seeing operating costs, store-level demand patterns, payment behaviour, fresh-food shelf-life economics and franchise dynamics from the inside, not just from the supplier side of the loading dock. That intelligence is valuable in negotiations with the larger konbini chains and in long-cycle product planning, and it gives Yamazaki a retail footprint of its own if the convenience-store sector ever consolidates in ways that disrupt the bread-procurement market.

Vatel Manuel-style logistics: why Japanese bread is not American bread

A foreign baker arriving in Japan often carries two assumptions that need to be unlearned: that bread is a frozen-supply-chain product, and that consumers tolerate shelf lives measured in weeks. Neither assumption applies to the Japanese mass-market bread category as Yamazaki has shaped it. Its logistics model — governed internally by detailed operational manuals covering daily handling, hygiene and freshness standards — is built around a delivery cadence in which bread baked overnight reaches retail shelves the same morning, with shelf life measured in days, and unsold product handled through strict return and disposal protocols.

This is structurally different from the U.S. and continental European mass-bread models that rely on preservatives, longer shelf life and frozen-distribution intermediaries. It is part of why imported foreign bread brands have struggled historically in the Japanese mass-bread aisle: the freshness expectation is set, and the logistics infrastructure to meet it is dominated by Yamazaki and a small number of peers. For foreign bakery operators, the entry strategy almost never looks like “ship our product to Japan.” It looks more often like local production through a joint venture, a licensing arrangement with a Japanese baker, or an in-store bakery concept that finishes dough on the retail premises — exactly the pattern of Yamazaki’s Vie de France de Paris joint venture with the Paris bakery house of the same name.

Yamazaki vs Pasco Shikishima vs Fuji Pan: the bread triopoly

Japan’s industrial bread market is often described as a three-way contest between Yamazaki, Pasco Shikishima (敷島製パン) and Fuji Pan (フジパン), with Yamazaki clearly the largest of the three. The three groups together account for the substantial majority of mass-market industrial bread production in Japan, with Yamazaki holding the leadership position by revenue, plant footprint and konbini-channel share.

| Indicator | Yamazaki Baking | Pasco Shikishima | Fuji Pan |

|---|---|---|---|

| Founded | 1948 (Ichikawa, Chiba) | 1920 (Nagoya, Aichi) | 1922 (Nagoya, Aichi) |

| Headquarters | Chiyoda-ku, Tokyo | Nagoya | Nagoya |

| Approx. revenue | ~JPY 1+ trillion | Several hundred billion JPY | Several hundred billion JPY |

| Listing | TSE Prime (2212) | TSE Prime (2218) | Unlisted (group) |

| Flagship brands | Royal Bread, Double Soft, Lunch Pack | Cho-juku, Super Premium | Honshoku Pan, Nendaki series |

| Konbini channel posture | Dominant PB & branded supplier | Strong regional / branded | Regional, food-service strong |

| Owned retail format | Daily Yamazaki (~600+ konbini) + Vie de France (~150+) | None at konbini scale | None at konbini scale |

The structural difference that matters most is the last row. Neither Pasco Shikishima nor Fuji Pan operates an owned convenience-store chain at meaningful scale. Yamazaki is the only one of the three that is simultaneously the dominant industrial bread maker, the largest konbini bread supplier, and the operator of its own — however modestly sized — convenience-store chain. That triple position is the deepest source of Yamazaki’s pricing power in the konbini channel and the hardest competitive moat for a rival baker to attack.

Vie de France, Yamazaki Café, and the French bakery question

Yamazaki’s relationship with French bakery is older, deeper and more commercial than the foreign-licensee model that has come to dominate luxury food-service in Japan. Vie de France, launched in the early 1980s as an in-store French-style bakery format, has grown into a network of approximately 150+ outlets, frequently positioned inside major railway stations, department stores and shopping centres. The format gave Yamazaki a premium retail surface to complement its mass-market bread distribution — a way to sell baguettes, croissants and pâtisserie at higher unit margins to consumers who would not necessarily reach for a Yamazaki-branded shokupan in a supermarket aisle.

The Vie de France de Paris joint venture extended that logic by partnering with the Paris bakery house of the same name, importing French recipes and brand authenticity into Yamazaki’s in-store bakery network. The Yamazaki Café concept extends the bakery experience into a sit-down format. For foreign bakery brands evaluating Japan, the Vie de France precedent is the most relevant template: a French-origin concept delivered through a Japanese industrial baker’s logistics, retail-format know-how and station-precinct real-estate relationships — rather than through direct-import or direct-operation models that typically struggle against Japan’s freshness expectations and store-economics realities.

What this means for foreign food brands, investors and bakery operators

Yamazaki’s structural position dictates the practical playbook for three distinct categories of foreign counterparty. For foreign food brands and ingredient suppliers — wheat, butter, sugar, dairy, jam, chocolate, frozen fillings — Yamazaki is, by raw procurement volume, one of the most consequential single buyers in the Japanese food system. The conversation that opens doors is usually not a category-buyer pitch but a supply-chain conversation: consistent multi-site delivery, quality certification compatible with Japanese standards, and price stability across yen-volatile commodity cycles.

For foreign bakery operators and brands — French, Italian, German, American — the lesson is that direct entry is rarely the right model. The companies that have built durable Japanese positions in premium bakery have almost all done so through partnerships with Japanese bakers, with Yamazaki the most natural counterparty given its retail-format experience and station-precinct relationships. Vie de France de Paris is one template; in-store bakery concessions inside Daily Yamazaki or Vie de France outlets are another. Cold imports are almost always the wrong answer.

For investors, Yamazaki sits in an unusual category: a slow-growth, defensive food-staples business with an underappreciated quasi-monopoly position in a critical retail channel. The strategic questions over the next five years sit at three frontiers — whether konbini-channel dominance survives accelerating private-label consolidation by the big-three chains; whether Daily Yamazaki ever scales beyond its current ~600-store boundary or remains a listening post; and whether in-store bakery and café formats can offset the secular pressure on plain industrial bread consumption from a shrinking population.

FAQ

How big is Yamazaki Baking compared to other Japanese bread makers?

Yamazaki is Japan’s largest bread maker, largest Western-style confectionery producer and one of the world’s biggest baking groups by revenue, with sales of approximately JPY 1 trillion or more. The two next-largest industrial bread makers — Pasco Shikishima and Fuji Pan — are substantially smaller in revenue and plant footprint, and together with Yamazaki they account for the substantial majority of Japan’s industrial bread market.

Why is Yamazaki so dominant in convenience-store bread?

Three reasons. First, plant density: roughly 80 production sites mean that every konbini distribution centre in Japan is within a daily-delivery truck-run of a Yamazaki bakery. Second, SKU breadth: approximately 5,000 active SKUs allow Yamazaki to absorb a national private-label programme without disrupting its branded business. Third, logistics discipline: a daily-fresh, no-freeze model that aligns precisely with what Japanese konbini chains demand. Industry estimates widely place Yamazaki’s share of konbini bread, sandwiches and pastries (branded plus private-label) at approximately 50% or more.

What is Daily Yamazaki and how does it compare to 7-Eleven, FamilyMart and Lawson?

Daily Yamazaki is Yamazaki Baking’s own convenience-store chain, with approximately 600+ stores nationwide, making it Japan’s number-four konbini brand by store count. It is far smaller than 7-Eleven Japan (approximately 21,000 stores), FamilyMart (approximately 16,500) and Lawson (approximately 14,600). It exists primarily as a captive distribution channel for Yamazaki bread products and as a strategic listening post inside the convenience-store sector, rather than as a head-to-head competitor to the big three.

Why don’t foreign bread brands sell well in Japan?

The Japanese mass-bread category is built around daily-fresh delivery and shelf life measured in days, not weeks. Yamazaki and a small number of domestic peers operate a no-freeze, daily-delivery logistics model that imported bread products — typically engineered for longer shelf life and frozen distribution — cannot match. Foreign bakery brands that succeed in Japan almost always do so through local production, licensing or joint-venture structures, often with a Japanese industrial baker as the operating partner.

How can a foreign company partner with Yamazaki?

The most common paths are ingredient supply contracts (wheat, dairy, butter, sugar, jam, chocolate, frozen fillings), bakery brand licensing through formats such as Vie de France or Vie de France de Paris, in-store bakery concessions inside Daily Yamazaki or Vie de France outlets, and co-development of premium SKUs targeted at the konbini private-label channel. Direct-import models for branded foreign bread products are rarely the right answer; partnership-led entry through Yamazaki’s logistics and retail-format infrastructure typically is.

Working with Yamazaki Baking

If you are a foreign food brand, ingredient supplier, bakery operator, licensor or investor looking to engage Yamazaki Baking — whether for ingredient supply contracts, private-label co-development, in-store bakery concessions inside Daily Yamazaki or Vie de France, French-style bakery joint ventures, or strategic investment dialogue — Japonity helps structure the introduction. Start with our Business Matching service to map the right counterparties inside the Yamazaki Baking group and the wider Japanese industrial bakery ecosystem.

Related from Japonity — Japan’s food retail, restaurants and konbini

- Zensho Holdings — Sukiya and the global beef-bowl empire

- Seven & i Holdings — The convenience-store empire targeted by Couche-Tard

- Lawson — The konbini now jointly owned by Mitsubishi Corp and KDDI

- FamilyMart — The Itochu-owned konbini, five years after the take-private

Want to source Japanese products beyond these company profiles? Japonity also runs a Japan Sourcing Hub — a research-grade catalogue of 1,185 verified Japanese food products and 200+ overseas EC stores, ready for B2B procurement.

Interested in Japanese business opportunities?

Whether you're looking for technology partners, engineering talent, or market insights — we can help connect you with the right Japanese organizations.

Get in Touch →