On the eastern edge of Reno, Nevada, sits a building so large it has its own postcode in the local industrial imagination: the Tesla–Panasonic gigafactory, a roughly 1.9-million-square-metre complex that since 2017 has produced most of the cylindrical lithium-ion cells in every Model 3 ever delivered. Eight time zones away, in Lake Forest, California, a quieter Panasonic subsidiary holds an estimated 60-plus percent of the global market for in-flight entertainment on commercial widebody aircraft — the small screens, the cabin Wi-Fi, the seat-back USB ports. And in Kadoma, Osaka, the same group still ships the rice cookers, hair dryers, and beauty appliances that defined its postwar brand. Three businesses, three customer bases, three economic logics. In April 2022, Panasonic — founded in 1918 by Konosuke Matsushita as a maker of duplex lamp sockets — formally became Panasonic Holdings Corporation, a Tokyo-listed parent sitting above eight operational subsidiaries. The restructuring was understated in the English-language press. It was, in fact, one of the most consequential governance changes in Japanese industry this decade, and it changes how foreign EV makers, aerospace customers, and B2B buyers should approach the group.

From duplex sockets to holdco: a 108-year commercial arc

Konosuke Matsushita, a former Osaka Electric Light apprentice, founded Matsushita Electric in 1918, producing improved electrical sockets from a rented two-room workshop. By the late 1920s the firm had moved into bicycle lamps and dry-cell batteries; by the 1950s, into the washing machines, televisions, and refrigerators that defined the Japanese postwar middle-class home. The Matsushita doctrine of mass production, vertical integration, and what Konosuke called the “tap-water philosophy” — making electrical goods as abundant and cheap as tap water — gave the company decades of compounding scale.

The Matsushita name was retired globally in 2008, replaced by the Panasonic mark already familiar in export markets. The rebrand coincided with the painful unwinding of what had been the group’s identity for two generations: consumer TVs and imaging. Plasma TV losses in the early 2010s — at one point exceeding ¥750 billion in cumulative impairments — forced the divestiture or shrinkage of much of the legacy display, semiconductor, and imaging business. By the time Kazuhiro Tsuga ended his decade as president in 2021, the group had been reshaped around three growth pillars: automotive batteries, B2B infrastructure (including aircraft IFE and supply-chain software), and a slimmer consumer-appliance core.

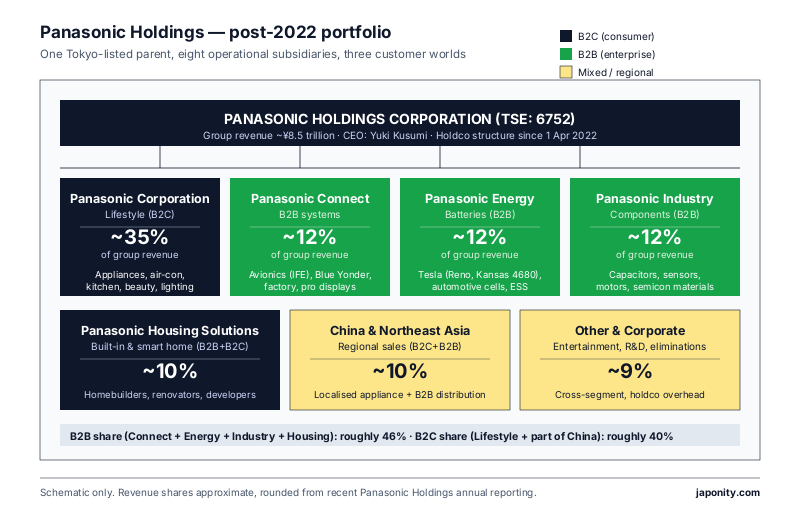

Yuki Kusumi, Tsuga’s successor, completed the structural part of that transition. On 1 April 2022, the listed parent became Panasonic Holdings Corporation, and the divisional businesses were carved out as operational subsidiaries — Panasonic Corporation (lifestyle appliances), Panasonic Energy (batteries), Panasonic Connect (B2B systems, including avionics), Panasonic Industry, and Panasonic Housing Solutions, among others. The point was not cosmetic. It was to give each subsidiary its own balance sheet, its own KPIs, and — crucially — the ability to enter joint ventures, capital raises, and partnerships without dragging the entire group’s risk profile along.

The 2022 holdco transition: why it matters more than it has been written about

Western coverage tended to describe the 2022 reorganisation as keiretsu housekeeping. That framing is wrong. The holdco structure does three things that materially change the group’s behaviour toward foreign counterparties.

First, it isolates capital risk by segment. Before 2022, a foreign EV maker negotiating a multi-billion-dollar battery off-take with Panasonic was effectively asking the entire group — including unrelated appliance and housing businesses — to back the deal. Post-2022, that contract sits with Panasonic Energy, whose balance sheet and capital allocation are notionally independent. The parent retains ownership, but the subsidiary can in principle pursue minority partners, project financing, or a future partial listing of its own.

Second, it creates clean optionality for divestiture. Several subsidiaries — Panasonic Connect’s avionics arm, certain housing units, possibly Industry — are structurally separable in a way they were not under the old divisional model. The Japanese press has speculated since 2023 about a possible carve-out of Panasonic Avionics. Whether or not that happens, the option exists in a way that would have required full corporate restructuring before.

Third, it changes the negotiating interface. A procurement team at an airline, semiconductor fab, logistics integrator, or EV OEM no longer sits across from “Panasonic Corporation, Audio-Visual and Communications Division.” It sits across from a named operational subsidiary with its own CEO and its own P&L. The conversation moves faster, and pricing flexibility is sometimes greater, because the seller is closer to the financials of the deal.

The portfolio today: a buyer’s-eye map

Total group revenue at Panasonic Holdings is approximately ¥8.5 trillion annually, with operating profit in the high single-digit-percent range — modest by global electronics standards but a meaningful improvement over the 2010s troughs. The segment mix below is approximate and rounded; readers running serious due diligence should pull the latest filings, since the group has been actively re-segmenting.

| Operational subsidiary | Approx. revenue share | What it actually does | Who buys from it |

|---|---|---|---|

| Panasonic Corporation (Lifestyle) | ~35% | Consumer appliances, air conditioning, beauty, kitchen, lighting | Mass-market consumers; appliance retailers |

| Panasonic Connect | ~12% | Avionics (IFE / cabin systems), supply-chain software (Blue Yonder), professional displays, factory solutions | Airlines, retailers, logistics integrators, factories |

| Panasonic Energy | ~12% | Cylindrical and prismatic Li-ion cells, automotive battery systems | Tesla, other EV OEMs, energy storage integrators |

| Panasonic Industry | ~12% | Electronic components, capacitors, sensors, semiconductor materials, motors | Industrial OEMs, automotive Tier 1s, electronics manufacturers |

| Panasonic Housing Solutions | ~10% | Built-in appliances, smart home equipment, building materials | Homebuilders, renovators, B2B property developers |

| China & Northeast Asia | ~10% | Regionalised appliance and B2B sales | Chinese and Korean retail / B2B channels |

| Other / corporate | ~9% | Entertainment, R&D, cross-segment | Mixed |

What this makes visible — and what the old “Panasonic, the TV company” framing obscured — is that the group is now structurally more B2B than B2C by revenue. Lifestyle appliances remain the largest single bucket, but Energy, Connect, Industry, and Housing Solutions together exceed it. That recomposition is the central fact about the group in 2026.

The Tesla relationship: a 16-year case study in dependency and dilution

No commercial relationship has shaped Panasonic Energy’s identity more than its partnership with Tesla. The two began collaborating around 2010, when Tesla was preparing the Model S and Panasonic was already the world leader in cylindrical lithium-ion cells for laptops and power tools. In 2014 they jointly announced Gigafactory 1 in Reno, with Panasonic responsible for cell manufacturing inside the building and Tesla for pack assembly and the shell. Mass production of 2170-format cells began in 2017.

At its peak in the late 2010s, Tesla accounted for an estimated half or more of Panasonic Energy’s automotive-cell revenue — a customer concentration that, for any other supplier, would have triggered an investor revolt. Panasonic accepted it because Tesla volumes gave the company production-scale leadership in a chemistry (NCA, then NCM variants) where scale economics were brutal. The trade-off was margin pressure from a single anchor customer with strong bargaining power.

Since 2020, that dependency has eased. Tesla has diversified its cell supply to include CATL and LG Energy Solution; Panasonic has diversified its customer base across US, European, and Japanese OEMs; and Panasonic Energy has announced new 4680-format cell capacity in Kansas (a roughly $4 billion plant with significant US Inflation Reduction Act tax-credit exposure). The 4680 — larger format, higher energy density, suited for next-generation EV packs — is the technical bet on which the next decade of the relationship rests. For a foreign EV OEM evaluating Panasonic Energy in 2026, the implications are clear: Panasonic now has spare capacity to court non-Tesla customers in a way it did not in 2018; the Kansas plant gives IRA-compliant cell supply for North American assembly; and the holdco structure means the contracting counterparty is a focused subsidiary, not a sprawling conglomerate.

Panasonic Avionics: the quiet aerospace monopoly

Few foreigners reading this article will have heard of Panasonic Avionics Corporation by name; many will have used its products this month. Headquartered in Lake Forest, California, it is the dominant supplier of in-flight entertainment and connectivity systems for commercial widebody aircraft worldwide, with an estimated market share north of 60% on widebody IFE installs, depending on how the segment is measured. Its principal competitor is Thales; together they constitute a near-duopoly in linefit IFE for new aircraft.

The business is structurally attractive for three reasons. First, switching costs are extreme: an airline that has standardised on Panasonic IFE for 200 widebodies cannot easily move to Thales without retraining maintenance crews, rewriting cabin software integrations, and replacing seat-back hardware. Second, the systems carry long-tail aftermarket revenue — software updates, content licensing, connectivity airtime, hardware replacements over a 20-plus-year aircraft life. Third, regulatory and certification barriers to entry are non-trivial, insulating incumbents from disruption.

Sitting inside Panasonic Connect rather than as a standalone listed entity, Avionics is a high-margin business buried inside a more diversified parent. The holdco structure has surfaced the unit’s economics in a way the old structure did not, which is part of why carve-out speculation has persisted in the Japanese press. Any aerospace procurement team negotiating IFE for a fleet refresh in 2026 should price in the possibility of ownership change.

Blue Yonder, factory automation, and the B2B software pivot

The most under-noticed move in recent Panasonic history is the September 2021 acquisition of Blue Yonder, the Scottsdale-based supply-chain software vendor, for an enterprise value of approximately $7.1 billion. The deal — Panasonic’s largest by some distance — placed a US-headquartered B2B SaaS business inside what had until then been a hardware-defined Japanese group. Blue Yonder now sits inside Panasonic Connect alongside the avionics and factory-automation units.

The logic is straightforward: Panasonic Connect’s hardware customers — retailers, factories, logistics integrators — increasingly buy outcomes, not boxes. A warehouse operator wants pick-and-pack throughput, not a scanner; a retailer wants forecasting accuracy, not a POS terminal. Blue Yonder gives Connect a software layer over its hardware portfolio, with a recurring-revenue profile the group’s appliance businesses cannot match. For foreign B2B buyers, the implication is that Panasonic Connect is increasingly an integrated-solutions vendor, not a component supplier — a posture the Panasonic of 2015 could not have credibly offered.

Leadership, governance, and the Kusumi era

Yuki Kusumi took over from Kazuhiro Tsuga as Group CEO in April 2021 and presided over the holdco transition the following year. His Connect-side background — deep experience in B2B and avionics — was a deliberate signal that the next decade would be defined by enterprise customers rather than retail consumers. Tsuga had spent his presidency cleaning up the consumer-electronics legacy, exiting unprofitable categories, and rebuilding the automotive battery business around the Tesla deal.

Governance under Kusumi has emphasised explicit return-on-invested-capital targets at the subsidiary level, more outside directors on the holdco board, and clearer disclosure of segment economics. Sustainability commitments have been re-stated, with carbon-neutrality targets across both operations and the lifecycle emissions of battery and appliance products — increasingly a negotiating point with European OEMs that require Scope 3 disclosure from suppliers.

Practical implications for foreign counterparties

For three distinct foreign audiences, the post-2022 Panasonic is a different counterparty than the pre-2022 version.

For EV makers and battery off-takers, the relevant entity is Panasonic Energy, with its own CEO, its North American footprint (Reno plus Kansas), and a strategic interest in diversifying away from single-customer concentration. A non-Tesla OEM evaluating cell supply in 2026 will find it more receptive to partnership conversations than five years ago.

For airlines and aerospace customers, the relevant entity is Panasonic Avionics inside Panasonic Connect. The market position is near-monopolistic, switching costs are high, and long-term ownership of the unit is an open strategic question. Procurement teams should price both points into their negotiating posture.

For industrial B2B buyers — factory automation, logistics, supply-chain software, professional displays — the counterparty is Panasonic Connect as a whole, increasingly positioned as an integrated solutions vendor with Blue Yonder layered on top of its hardware portfolio. The conversation has shifted from component selection to outcomes.

The thread running through all three is that the holdco structure makes Panasonic legible in a way the old conglomerate was not. A foreign counterparty no longer has to triangulate which “division” owns the contract; the operational subsidiary is the contract owner. That clarity, more than any single business move of the last five years, is what makes the group easier to do business with in 2026.

The wider point

Japanese conglomerates have spent the last decade under sustained pressure — from activist investors, foreign analysts, and a domestic Corporate Governance Code that has tightened disclosure expectations — to either justify their breadth or unbundle. Hitachi has unbundled aggressively. Toshiba has been broken up. Sony reorganised around content and sensors. Panasonic’s response is the quietest but in some ways the most interesting: rather than break the group apart, it has chosen to operate the parts independently while keeping the parent. Whether that proves the right call will depend on whether the subsidiaries — Energy chasing the 4680, Connect monetising Blue Yonder, Avionics defending its IFE moat — can each compete as standalone businesses while drawing on the holdco’s balance sheet. The next five years of segment-by-segment disclosure will tell whether the structure written about as housekeeping is what Kusumi has insisted it is: the foundation of a more disciplined, more enterprise-facing Panasonic.

FAQ

Who owns Panasonic Holdings, and is it still independent?

Panasonic Holdings Corporation is listed on the Tokyo Stock Exchange (ticker 6752) with a broadly distributed shareholder base — domestic and foreign institutional investors, cross-shareholdings with Japanese financial institutions, and retail holders. There is no controlling shareholder. The founder’s Matsushita family no longer plays a governance role of any significance.

Is Panasonic still primarily a TV and consumer-electronics company?

No, and this is the most common foreign misconception. Consumer appliances (the legacy “TV company” identity) account for roughly a third of group revenue. Energy, Connect, Industry, and Housing Solutions together account for materially more. The group’s strategic centre of gravity has moved decisively to B2B.

What is the practical difference between dealing with Panasonic Energy and dealing with Panasonic Corporation?

Panasonic Energy is the operational subsidiary that handles automotive batteries and energy storage; Panasonic Corporation (the subsidiary, not the old listed parent) handles lifestyle appliances. They have separate CEOs, separate balance-sheet accountability under the holdco, and very different customer bases. A procurement team should make sure it is engaging the correct entity from the start.

Is Panasonic Avionics being sold?

There has been persistent speculation in the Japanese financial press since 2023 that the avionics unit could be carved out, but as of recent disclosure the group has not announced a divestiture. Aerospace customers should nonetheless account for the possibility of an ownership change in long-cycle procurement decisions.

How does the US Inflation Reduction Act affect Panasonic Energy’s North American strategy?

The IRA’s clean-vehicle and advanced-manufacturing tax credits materially improve the economics of domestic battery cell production in the US. Panasonic Energy’s Kansas plant, alongside the existing Reno gigafactory, positions the company to supply IRA-compliant cells to North American–assembled EVs — a structural advantage versus suppliers without US manufacturing.

Working with Panasonic

Looking to partner with Panasonic group subsidiaries — whether on automotive batteries, aerospace IFE, supply-chain software, factory automation, or appliance distribution — or evaluating Japanese industrial conglomerates as part of a broader Asia strategy? Get in touch via Japonity’s business-matching service — we connect foreign buyers, brands, and operating partners with the right Japanese counterparties.

Related from Japonity — Japan’s electronics & IT services

- Sharp Corporation — The Foxconn rescue eight years on — pivot from large-TV LCDs

- Fujitsu — The PC giant that bet its future on services — Fugaku to Uvance

- NEC Corporation — Defence, biometrics, undersea cable — Japan’s under-appreciated tech infra

Want to source Japanese products beyond these company profiles? Japonity also runs a Japan Sourcing Hub — a research-grade catalogue of 1,185 verified Japanese food products and 200+ overseas EC stores, ready for B2B procurement.

Interested in Japanese business opportunities?

Whether you're looking for technology partners, engineering talent, or market insights — we can help connect you with the right Japanese organizations.

Get in Touch →