Subaru Corporation is the smallest of Japan’s mainstream automakers by global volume — and by some distance the most American by revenue. Roughly seven out of every ten Subarus sold in 2024 went to a U.S. customer, a geographic concentration with no parallel among the country’s car companies and one that has produced both the strongest brand affinity in the U.S. crossover market and the single most acute strategic vulnerability any Japanese carmaker carries into the late 2020s. The company that emerged from Nakajima Aircraft, the wartime maker of the Zero fighter, and rebranded itself from Fuji Heavy Industries to Subaru only in 2017, now finds itself rebuilding for an EV transition it cannot finance on its own — which is why the approximately 20% stake held by Toyota since 2019 has quietly become the most important strategic relationship in Subaru’s history.

A company that started in the sky

Subaru’s industrial DNA is aerospace, not automotive. Its direct predecessor, Nakajima Aircraft Company, was founded in 1917 and became one of imperial Japan’s two largest aircraft manufacturers. Nakajima built the Sakae radial engines that powered the Mitsubishi A6M Zero — the carrier-based fighter that dominated the early Pacific air war — as well as its own Ki-43, Ki-44, and Ki-84 fighters. The company employed several hundred thousand workers at its wartime peak across factories in Gunma, Saitama, Tokyo, and beyond.

Postwar dissolution under Allied occupation broke Nakajima into a dozen successor entities. Five of those small companies regrouped in 1953 as Fuji Heavy Industries, and Fuji Heavy launched the first Subaru-branded car — the diminutive Subaru 360 kei car — in 1958. The Subaru name was chosen by Kenji Kita, the founding president, after the open star cluster known in Japan as Subaru (昴) and in the West as the Pleiades. The six-star logo references the five member companies of Fuji Heavy plus the parent group.

The aerospace business never went away. Subaru’s Aerospace Company in Utsunomiya remains a Tier-1 partner on the Boeing 787 and is the prime contractor on the Bell-Subaru UH-2 helicopter for the Japan Ground Self-Defense Force. The segment is small relative to autos — typically a low single-digit percentage of consolidated revenue — but it provides engineering depth that pure-play automakers do not have.

The U.S. dependence: moat and mortgage

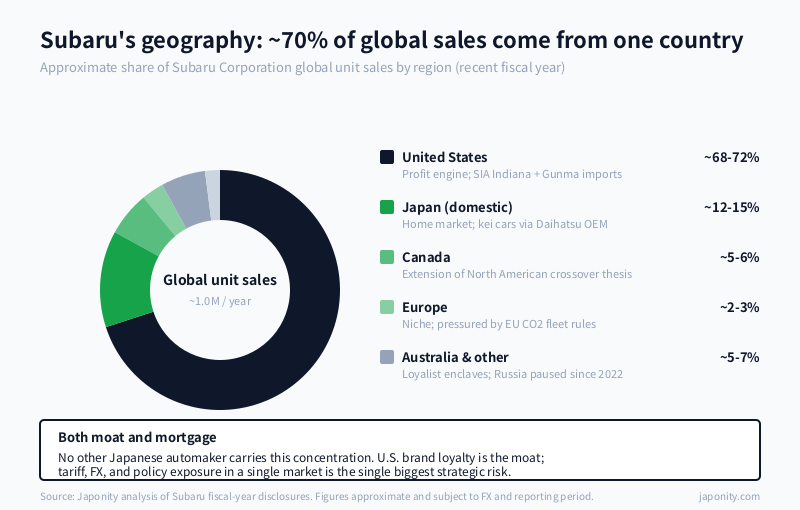

To understand Subaru, look at where its cars sell. The company produces roughly one million vehicles a year globally. The United States alone takes the lion’s share of that output. The table below shows the approximate regional mix, drawn from recent fiscal-year disclosures.

| Region | Approx. share of global unit sales | Strategic role |

|---|---|---|

| United States | ~68-72% | Profit engine, brand heartland, single largest exposure |

| Japan (domestic) | ~12-15% | Home market; kei cars sourced from Daihatsu under OEM arrangement |

| Canada | ~5-6% | Extension of North American crossover thesis |

| Europe | ~2-3% | Niche; pressured by EU CO2 fleet rules |

| China | <1% | Withdrawn from local manufacturing; minimal exposure to price war |

| Australia, Russia, other | ~5-7% | Loyalist enclaves; Russia paused since 2022 |

No other Japanese automaker carries this kind of geographic concentration. Toyota’s U.S. revenue share sits around a quarter of group sales. Honda is closer to forty percent. Nissan and Mazda are both meaningfully diversified across Europe and emerging markets. Subaru’s ~70% U.S. dependence is, in any conventional sense, a strategic weakness — a single tariff regime, a single emissions code, a single dollar-yen swing, and a single dealer network do most of the work of holding up the income statement.

And yet it is also the moat. Subaru in the United States is not a price-led brand. It is a values-led brand, with an unusually well-defined customer cohort: outdoor-oriented, college-educated, often female-skewed for an automaker, concentrated in the Pacific Northwest, the Mountain West, and New England. The company’s “Love” marketing platform, the long-running Subaru Loves Pets and Subaru Share the Love campaigns, and a dealer network that has stayed remarkably stable through the post-2008 industry consolidation have all reinforced a customer-lifetime-value profile that comfortably outperforms Subaru’s segment-share numbers would suggest.

The boxer engine and symmetrical AWD: a real differentiator

Most automakers’ platform stories are marketing dressed up as engineering. Subaru’s is closer to the reverse. The horizontally opposed “boxer” engine — used in nearly every Subaru passenger vehicle for sixty years — sits lower in the chassis than an inline or V-configuration engine, lowers the vehicle’s center of gravity, and pairs naturally with a longitudinally mounted all-wheel-drive transmission. The result is what Subaru calls Symmetrical All-Wheel Drive: a drivetrain layout in which the power transfer components are arranged on a single longitudinal axis, which engineers credit with better weight balance and more predictable behavior in low-traction conditions.

The engineering claims are debated at the margin; the brand consequences are not. In the United States, Subaru is synonymous with all-wheel drive in a way that no competitor has been able to dislodge. The Outback, the Forester, and the Crosstrek collectively define a vehicle category — affordable, capable, modestly outdoorsy crossovers — that other automakers entered late and have struggled to brand around. The boxer-and-AWD pairing is the technical scaffolding on which that brand sits, and it is genuinely difficult to replicate without a clean-sheet powertrain program.

It is also, awkwardly, electrification-resistant. An EV does not need a longitudinally mounted boxer engine. The brand promise survives the powertrain transition — symmetrical AWD is achievable with dual-motor configurations — but the engineering moat does not. This is one of the structural reasons Subaru’s EV strategy is so closely tied to Toyota’s.

EyeSight and the safety-first repositioning

Subaru’s second technical differentiator is EyeSight, the stereo-camera-based driver-assistance system first introduced in 2008 and now standard on most Subaru vehicles sold globally. The architecture uses two color cameras mounted near the rearview mirror to construct a stereoscopic depth map of the road ahead, supporting adaptive cruise control, pre-collision braking, lane-keeping, and lane-departure warnings. Independent insurance-industry studies, notably from the U.S. Insurance Institute for Highway Safety, have consistently rated EyeSight-equipped Subarus among the better performers in front-collision avoidance.

For a small automaker, owning a named safety technology — and earning IIHS Top Safety Pick + ratings across a disproportionate share of the lineup — has been one of the highest-leverage investments Subaru has made. It supports the brand premium, it justifies the pricing relative to mainstream Toyota and Honda crossovers, and it gives the dealer network a structural conversation point. EyeSight is being progressively upgraded toward more advanced driver-assist capability, including a next-generation system co-developed in part with Toyota’s safety-technology stack.

The Indiana plant: why SIA matters more than Gunma

Subaru of Indiana Automotive, in Lafayette, Indiana, is the structural answer to the U.S.-exposure problem — and it does not solve it. SIA, opened in 1989 originally as a joint venture with Isuzu and now wholly Subaru-owned, builds the Outback, Legacy, Ascent, and Impreza for the North American market, with annual capacity in the neighborhood of 370,000 to 400,000 vehicles. It is the only Subaru plant outside Japan, and it accounts for roughly half of Subaru’s U.S. deliveries.

The other half is exported from Gunma, Subaru’s historic manufacturing complex in Ota, Gunma Prefecture. The Crosstrek, Forester, and BRZ are built there for U.S. shipment. That import flow is exposed to U.S. trade policy, dollar-yen exchange rates, and shipping economics in ways the SIA-built vehicles are not. The 2018 USMCA renegotiation, the 2024-2025 round of tariff threats on Japanese auto imports, and the broader political shift toward domestic-content sourcing in U.S. EV incentives have all sharpened the question of how much more of Subaru’s U.S. volume needs to move onshore over the next decade.

Subaru has announced plans to build EVs at SIA from the late 2020s, retooling part of the Indiana facility for battery-electric production. The capital required is substantial, the timeline is tight, and the company is not large enough to amortize the cost across multiple platforms — which brings the Toyota relationship back into view.

The Toyota stake: a 20% relationship doing 80% of the work

Toyota Motor Corporation took an approximately 16.5% stake in Fuji Heavy Industries in 2008, increasing it to roughly 20% in 2019 in conjunction with a deepened technical alliance. Subaru in turn took a small reciprocal stake in Toyota. The capital tie is modest by the standards of corporate Japan — significantly smaller than Toyota’s controlling positions in Daihatsu and Hino — but the technical cooperation it underwrites has become essential to Subaru’s product roadmap.

The first joint product was the Subaru BRZ / Toyota 86 sports coupe, launched in 2012 and now in its second generation as the BRZ and the Toyota GR86. The second, and far more strategically significant, is the Subaru Solterra, Subaru’s first volume battery-electric vehicle, co-developed with the Toyota bZ4X on a shared e-TNGA-derived platform. Subaru contributed AWD calibration expertise; Toyota contributed the platform, battery sourcing, and scale. The Solterra is built at Toyota’s Motomachi plant in Toyota City, not at a Subaru facility.

This is a meaningful concession of vertical control, and Subaru has been candid about why it made the trade. A company producing roughly a million vehicles a year cannot independently amortize a clean-sheet EV architecture across the multiple body styles, battery sizes, and regulatory regimes that the late-2020s market will demand. Toyota provides scale that Subaru cannot manufacture internally; Subaru provides AWD calibration, EyeSight integration, and access to the most loyal customer base in U.S. crossovers. The next-generation Subaru EVs announced for the late 2020s, including a three-row utility intended as a Forester / Outback successor in BEV form, are expected to draw further on Toyota platform components.

The risk inside this arrangement is brand dilution. Subaru’s U.S. customers buy Subaru because it is Subaru — not Toyota. The Solterra and bZ4X are visibly close cousins, and the commercial reception of the first joint EV has been mixed. The product question for the second half of this decade is whether Subaru can maintain visual, dynamic, and emotional differentiation on a shared platform, or whether the partnership gradually flattens what made the brand distinct.

Management transition and the post-Nakamura era

Subaru is led by Atsushi Osaki, who became president and CEO in 2023, succeeding Tomomi Nakamura. Osaki’s career inside the company has been weighted toward manufacturing and quality, including extended periods at SIA in Indiana — which signals where the board sees the operational priorities. The Nakamura era (2018-2023) was defined by the rebrand from Fuji Heavy Industries to Subaru Corporation, the deepening of the Toyota relationship, and a public reckoning with quality-control issues in domestic factory inspection processes that surfaced in 2017-2018.

The current leadership question is execution: can Subaru deliver the SIA EV conversion, the next round of Toyota-platformed BEVs, and the EyeSight evolution without losing its dealer base or its U.S. customer cohort? The answer will not be visible until 2027 or 2028 in any clean way. In the meantime, Subaru is leaning harder on what is working — Forester and Outback refreshes, expanded EyeSight capability, and the long-running marketing platform that has held the brand together through two decades of industry turbulence.

The aerospace business: smaller than the slides suggest, more durable than they imply

It is easy to overlook Subaru’s aerospace segment because it is small in revenue terms. It is harder to overlook when the question is engineering credibility. The Utsunomiya plant builds the center wing box for every Boeing 787 — a structural component that is, in Boeing’s own assessment, one of the most demanding composite assemblies on the aircraft. Subaru is also the prime contractor on the UH-2 utility helicopter program for the Japanese Self-Defense Forces, license-builds the AH-64D Apache, and supplies components on multiple commercial aircraft programs. The business also provides engineering talent flows between the aerospace and automotive divisions, particularly in composite materials and lightweight structures — capability few automakers have in-house.

Why Subaru still warrants its own thesis

The strategic shape of Subaru is unusual enough that it cannot be analyzed by analogy. It is too small to play the global volume game, too brand-specific to be absorbed comfortably into a larger group, and too dependent on the U.S. crossover market to ride out a policy shock in that geography. The Toyota alliance gives it the scale it needs to electrify; the boxer-and-AWD heritage gives it a brand that cannot easily be replicated; the aerospace business gives it institutional engineering depth; and the Indiana plant gives it a partial hedge against the U.S. concentration that is otherwise the company’s defining risk.

The next five years will test whether all of those pieces still fit. The Solterra’s commercial trajectory, the SIA EV conversion, the next-generation EyeSight rollout, and the U.S. trade policy environment will each move independently of Subaru’s control. What is within the company’s control — product engineering quality, dealer relationships, marketing consistency, and the carefulness of how it manages the Toyota partnership without losing brand identity — is what Subaru has historically been good at. Whether that is enough in a market that is rewarding scale and Chinese cost structure above almost everything else is the open question.

FAQ

Who owns Subaru Corporation?

Subaru is publicly listed on the Tokyo Stock Exchange (ticker 7270). The largest single shareholder is Toyota Motor Corporation, with an approximately 20% stake acquired in stages from 2008 and increased in 2019 alongside a deepened technical partnership. The remainder of the shareholding is dispersed across Japanese trust banks, global asset managers, and individual investors, with no controlling family block. Subaru also holds a small reciprocal equity stake in Toyota.

What was Fuji Heavy Industries and when did it become Subaru?

Fuji Heavy Industries was the postwar holding company formed in 1953 from five successor entities of the prewar Nakajima Aircraft Company. It launched the Subaru brand in 1958 with the Subaru 360 kei car. The company formally renamed itself Subaru Corporation in April 2017, aligning the corporate name with what had long been its most recognizable brand globally. The aerospace and defense business, which traces directly to Nakajima, continues to operate as the Aerospace Company within Subaru Corporation.

Why is Subaru so dependent on the United States?

The concentration is a function of brand-market fit rather than deliberate strategy. Subaru’s all-wheel-drive crossovers and the values-led marketing platform built around them happen to resonate with a particular U.S. customer cohort — outdoor-oriented, safety-conscious, college-educated buyers concentrated in the Pacific Northwest, the Mountain West, and New England — in a way that has not transferred at scale to Europe, China, or other Asian markets. The company has not built equivalent demand in markets where the AWD use case is less central. The result is a structural ~70% U.S. revenue exposure that the company has not chosen to reduce, partly because the U.S. business is profitable enough to make diversification expensive in opportunity-cost terms.

What is the boxer engine and why does Subaru still use it?

The boxer, or horizontally opposed, engine arranges its cylinders in two banks lying flat on either side of the crankshaft, rather than in a vertical line or a V. The configuration sits lower in the chassis than alternatives, which lowers the vehicle’s center of gravity and pairs naturally with a longitudinally mounted all-wheel-drive transmission. Subaru has used boxer engines in nearly all of its passenger cars for sixty years, and it is one of only two volume automakers globally (alongside Porsche) that still does so. The configuration is central to Subaru’s Symmetrical All-Wheel Drive architecture and to the brand’s engineering identity, although it does not carry over directly into battery-electric powertrains.

How does the Toyota partnership work in practice?

Toyota holds approximately 20% of Subaru and provides scale and platform components that Subaru cannot independently amortize. The two companies have co-developed the BRZ / GR86 sports coupe and the Solterra / bZ4X battery-electric SUV, with further joint EV products announced for the late 2020s. Subaru contributes AWD calibration, EyeSight integration, and access to its U.S. customer base; Toyota contributes platform engineering, battery sourcing, and manufacturing scale. The arrangement is closer to a deep technical alliance than to a parent-subsidiary structure — Subaru retains operational independence, its own dealer network, and distinct brand positioning — but the dependency is real, especially for EV architecture.

Working with Subaru

For overseas suppliers, technology partners, and licensors, Subaru is a more concentrated point of entry than the larger Japanese automakers. The supplier base is smaller, the engineering centers are fewer (principally Ota in Gunma, with regional support at SIA in Indiana), and the procurement decision-making is correspondingly more direct. Live engagement categories include battery cells and modules for the upcoming SIA-built EVs, ADAS components and sensors for the EyeSight roadmap, lightweight materials and composites (where there are also crossover opportunities with the aerospace business), motor and inverter components, and software for next-generation cockpit and connectivity systems.

The aerospace business in Utsunomiya is a separate but adjacent entry point, particularly for composite materials, precision casting, avionics components, and defense electronics suppliers with prior Tier-1 or Tier-2 experience on Boeing or Lockheed programs. Subaru’s dual exposure — automotive and aerospace under one corporate roof — is unusual enough that suppliers with capability across both domains are rare and correspondingly attractive to the company.

If your company supplies battery materials, ADAS sensors, lightweight structures, motor components, or software relevant to Subaru’s EV and safety roadmap — or if you are looking to license Japanese technology or distribute Subaru-adjacent products in your home market — Japonity’s business matching service can help structure a credible first conversation with the right counterparty in Gunma, Tokyo, or Lafayette.

Related from Japonity — Japan’s automakers

- Toyota Motor Corporation — Multi-pathway powertrain strategy from the world’s #1 automaker

- Honda Motor — The motorcycle giant the auto press forgot

- Nissan Motor — Post-Ghosn, post-Honda — what the Renault entanglement still means

- Mazda Motor Corporation — The Hiroshima underdog that bet on internal combustion

- Suzuki Motor — India’s market king — Maruti Suzuki’s ~40%+ share

Want to source Japanese products beyond these company profiles? Japonity also runs a Japan Sourcing Hub — a research-grade catalogue of 1,185 verified Japanese food products and 200+ overseas EC stores, ready for B2B procurement.

Interested in Japanese business opportunities?

Whether you're looking for technology partners, engineering talent, or market insights — we can help connect you with the right Japanese organizations.

Get in Touch →