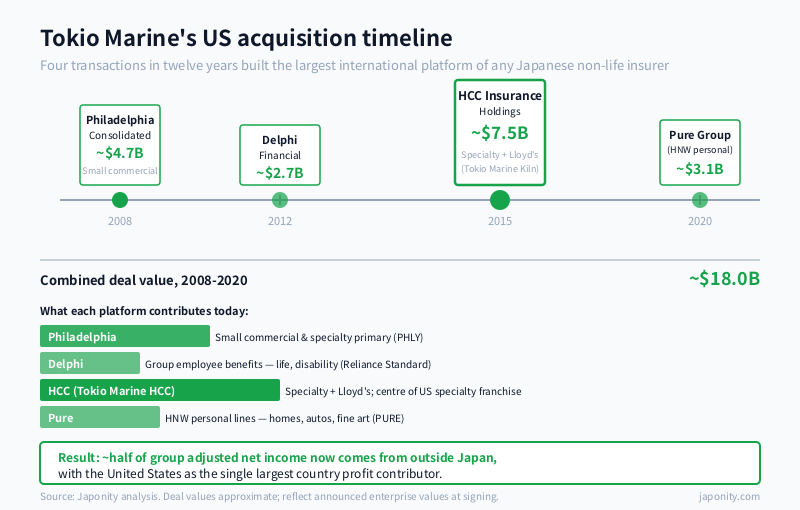

Approximately half of Tokio Marine Holdings’ adjusted net income now comes from outside Japan, and the largest single contributor inside that international stack is the United States — a fact that would have read as fantasy to anyone reading the company’s accounts in 2007. Three landmark acquisitions explain the shift: Philadelphia Consolidated Holding (Philadelphia Insurance Companies) in 2008 for approximately $4.7 billion, HCC Insurance Holdings in 2015 for approximately $7.5 billion, and Pure Group in 2020 for approximately $3.1 billion, with Delphi Financial in 2012 (approximately $2.7 billion) connecting them. Layered underneath is a domestic story: the 2004 merger with Nichido Fire & Marine that produced Tokio Marine & Nichido, and a post-merger “loss profit” reform — the deliberate decision to walk away from underpriced policies that the Japanese non-life market had been writing for decades — that helped reshape Japan’s three-way oligopoly alongside SOMPO Holdings and MS&AD. For foreign reinsurers, brokers, and corporate risk buyers trying to read Japan’s insurance market, Tokio Marine is the firm whose structure to understand first.

An 1879 marine insurer that became Japan’s largest non-life group

Tokio Marine Insurance was founded in 1879 as Japan’s first marine insurance company, established during the Meiji era when Japan was building the institutional scaffolding — banks, exchanges, insurers, joint-stock companies — that an industrialising economy demands. The original mandate was narrow: to underwrite the cargo and hull risks of Japanese shipping. The firm grew with the trade flows, added fire and casualty lines through the early twentieth century, and emerged from the post-war reconstruction as one of the dominant Mitsubishi-affiliated financial institutions, headquartered in Marunouchi, Tokyo — the central business district built around Tokyo Station that houses most of the keiretsu-linked corporate headquarters.

The structure that exists today — Tokio Marine Holdings, Inc., listed on the Tokyo Stock Exchange under code 8766, with Tokio Marine & Nichido Fire Insurance Co., Ltd. as its principal domestic operating subsidiary — took shape in two stages. In 2002 the firm reorganised under a financial holding company called Millea Holdings; in 2004 that vehicle merged with Nichido Fire & Marine to form Tokio Marine & Nichido, and in 2008 the holding company was renamed Tokio Marine Holdings. Satoru Komiya has served as President and Group CEO since June 2019. The group employs approximately 45,000 people globally and operates in roughly forty-five countries and regions.

The Nichido merger, and Japan’s three-way non-life oligopoly

The 2004 merger with Nichido Fire & Marine matters for reasons that extend well beyond Tokio Marine’s perimeter. It was one move in a broader consolidation that, over the following decade, reduced Japan’s non-life industry from a fragmented field of mid-sized mutuals and joint-stock insurers into a three-way oligopoly. Tokio Marine & Nichido, formed in 2004, was the first of the three. SOMPO Holdings emerged from the 2010 combination of Sompo Japan and Nipponkoa (the latter itself a merger of older firms) and the subsequent 2014 integration into a single operating company. MS&AD Insurance Group Holdings was formed in 2010 through the combination of Mitsui Sumitomo with Aioi Insurance and Nissay Dowa General Insurance, producing Aioi Nissay Dowa Insurance as one of its principal subsidiaries.

The result is a market in which three groups — Tokio Marine, SOMPO, MS&AD — together hold a share of Japan’s non-life premium consistently reported in the high eighty to low ninety per cent range. For foreign reinsurers and brokers, that concentration matters in practical ways. Reinsurance placements for the largest Japanese property catastrophe programmes are negotiated with these three counterparties more than any other; broker access to Japanese commercial risk pools runs predominantly through the three groups’ commercial divisions; and the pricing cycle in domestic non-life is driven by the underwriting discipline inside those three. A foreign carrier deciding whether to open a Tokyo branch is, in practice, deciding whether it can build a distribution relationship around — not against — the three groups.

| Group | Formed | Approx. domestic non-life share | International footprint | Distinctive character |

|---|---|---|---|---|

| Tokio Marine Holdings | 2004 (Tokio Marine & Nichido); 2008 holdco rename | ~25-27% | US-led: Philadelphia, HCC, Pure, Delphi; ~50% of group profit international | Mitsubishi-affiliated; the international leader of the three |

| SOMPO Holdings | 2010 (Sompo Japan + Nipponkoa) | ~24-26% | Endurance Specialty acquisition 2017; Sompo International platform; nursing care domestic diversification | The diversification leader; large Himawari Life and nursing care exposures |

| MS&AD Insurance Group | 2010 (Mitsui Sumitomo + Aioi Nissay Dowa) | ~30-33% | Amlin (Lloyd’s, 2016); MS Amlin platform; Asia regional emphasis | Largest domestic share; strong Lloyd’s and Asia presence |

Comparing the three side by side makes Tokio Marine’s distinctive choice visible. SOMPO bought a Lloyd’s-and-Bermuda specialty reinsurer and built nursing care at home; MS&AD bought a Lloyd’s franchise in Amlin and leaned into Southeast Asia; Tokio Marine bought into the US middle-market and specialty primary market. Of the three, Tokio Marine’s strategy has produced the largest single-country international profit pool.

The US transformation, in four acquisitions

Tokio Marine’s US strategy is best read not as a single deal but as a sequence — four transactions over twelve years, each one buying a different shape of US underwriting franchise, with each subsequent purchase tightening the portfolio.

Philadelphia Consolidated Holding (2008, approximately $4.7 billion). The first and, in some ways, still the most important. Philadelphia Insurance Companies (PHLY), based in Bala Cynwyd, Pennsylvania, was at the time one of the most consistently profitable US property and casualty insurers in the small commercial and specialty segments — non-profits, religious organisations, schools, fitness centres, condominium associations. Long-tenured underwriters, sticky niche distribution, and a disciplined growth track record gave Tokio Marine a US platform that did not depend on price-cutting to grow. Closed in December 2008, into the teeth of the global financial crisis, the deal looks contrarian in hindsight.

Delphi Financial Group (2012, approximately $2.7 billion). Delphi added group employee benefits insurance — group life, disability, dental, vision — through Reliance Standard and Matrix Absence Management. The strategic logic was diversification away from the property-and-casualty cycle into a steadier, fee-and-premium-based business with structurally different loss patterns. Delphi remains the smallest of the four US acquisitions but the one that most clearly addresses underwriting cycle correlation.

HCC Insurance Holdings (2015, approximately $7.5 billion). The largest of the four. HCC, headquartered in Houston, was a specialty insurer covering professional liability, surety, agricultural insurance, medical stop-loss, marine, energy, and other niche lines. Struck in June 2015 and closed that October, it vaulted Tokio Marine into the front rank of US specialty insurers and added a Lloyd’s syndicate (now under the Tokio Marine Kiln brand) plus a substantial international specialty book. HCC is now branded as Tokio Marine HCC and remains the centre of gravity of the group’s US specialty franchise.

Pure Group (2020, approximately $3.1 billion). Pure (Privilege Underwriters Reciprocal Exchange) is a US high-net-worth personal lines insurer — homes, autos, fine art, jewellery, watercraft for households whose insured assets run from several million to tens of millions of dollars. Closed in February 2020, it gave Tokio Marine a US personal lines franchise positioned at the only segment of US personal lines that has consistently grown profitably — the wealthy household — while avoiding the volatile, capital-intensive standard auto market.

The “loss profit” reform: how Japanese non-life learned to underwrite again

The international story is the headline, but the domestic story is what funded it. In the late 1990s and through the early 2000s, Japan’s non-life market suffered from a structural defect that foreign analysts often described in plain terms: insurers were writing policies that, on a risk-adjusted basis, were priced to lose money. The phrase that circulated inside the industry, sometimes translated loosely as “loss profit” or “underwriting loss compensated by investment income”, captured the pattern. Premium rates on automobile, fire, and certain commercial lines were held below their actuarially fair levels by competitive pressure and by a long-standing assumption that investment income on the float would absorb the shortfall. As Japanese long-term interest rates fell toward zero through the 2000s and 2010s, that assumption collapsed.

The post-merger Tokio Marine & Nichido was among the first large insurers to commit visibly to walking away from underpriced policies — declining renewals where the loss ratio could not be justified, repricing auto books, exiting distribution arrangements where commission economics made profitability impossible. The discipline was easier to enforce inside a recently merged firm with a new top team than inside the older legacy carriers. As SOMPO and MS&AD completed their own mergers and faced the same arithmetic, the entire market moved toward more rational pricing. The combined ratio of Tokio Marine & Nichido’s domestic non-life book, which had hovered close to or above 100% in the worst years of the early 2000s, settled in the mid-to-high nineties through most of the 2010s and has fluctuated with natural catastrophe years (notably the 2018 typhoons Jebi and Trami, and 2019’s Hagibis) ever since.

Life insurance, and the part of the group that quietly compounds

Tokio Marine & Nichido Life Insurance is the principal life operating subsidiary. Japan’s life insurance market is one of the largest in the world by premium and one of the most mature by penetration; structural growth rates are low and the demographic trajectory is unfavourable, but the in-force book generates substantial spread and fee income, and the regulatory framework rewards the conservative asset-liability management that Japanese life insurers have historically practised. The international life business is smaller and concentrated in Asia, but the segment as a whole is the most steadily compounding part of the group, with profit volatility lower than either domestic non-life or US specialty. For foreign asset managers and private credit firms looking at Japan, the life subsidiaries of the three big non-life groups are an important institutional pool — they allocate to private credit, infrastructure, real estate, and alternative credit strategies as part of their ALM mix, driven by domestic regulatory capital rules and yen-hedging cost.

Reinsurance and the global catastrophe book

Tokio Marine is one of the largest single buyers of property catastrophe reinsurance in the world, reflecting the concentration of Japanese earthquake and typhoon exposure on its domestic balance sheet plus the international catastrophe exposure that HCC, Pure, and the Lloyd’s franchises have added. The group’s main catastrophe placement is among the largest that Japanese-domiciled cedents bring to the global market each renewal, and its structure — retention layers, occurrence vs aggregate covers, alternative capital participation through cat bonds — is closely watched by other Japanese cedents as a market signal. The group also writes reinsurance through Tokio Marine Kiln and other international units, and the internal cession structure at this scale is sufficiently complex that net retained positions on a given peril can differ substantially from the gross picture at any individual entity.

What this means for foreign reinsurers, brokers, and corporate risk buyers

For foreign reinsurers, Tokio Marine is both a customer (buying property catastrophe and casualty cover into its Japan book and the international platforms) and a competitor (writing specialty reinsurance from Bermuda, London, and Houston); the relationship needs to be sized to both sides. For brokers, Tokio Marine’s Japan commercial divisions plus Tokio Marine HCC, Tokio Marine Kiln, Philadelphia, Pure, and Delphi internationally represent six distinct buying centres with different underwriting authorities and lines of business — a relationship at one does not automatically extend to the others. For corporate risk buyers — foreign multinationals operating in Japan, or Japanese multinationals operating overseas — Tokio Marine is the most internationally fluent of the three Japanese non-life groups, both because of the depth of its US operations and because it has lived inside US regulatory and rating-agency frameworks for nearly two decades. For programmes that need a Japan-domiciled lead with the technical and commercial capacity to negotiate as a global insurer rather than as a domestic distributor, Tokio Marine is the natural starting point in most categories.

The strategic question for the next five years

Tokio Marine is now a group in which the United States is the single largest profit contributor and Japan is the largest premium contributor, and the management challenge over the coming five years is keeping that split productive rather than tense. The US platforms — Philadelphia, HCC, Pure, Delphi — have produced returns substantially above the cost of capital deployed to acquire them, but they have also created the question of what the next acquisition or platform looks like, and whether the international stack should diversify further from the US or deepen inside it. The group has signalled selective interest in additional specialty acquisitions globally, in Asian growth markets, and in adjacent capabilities (data, claims technology, embedded distribution) rather than transformative single transactions of the HCC or Philadelphia scale.

Domestically, the work is more incremental. Japan’s automobile market is the largest single non-life premium pool inside the group, and the long shift toward EVs, telematics-based pricing, and ride-sharing changes both the loss profile and the distribution economics. The post-merger underwriting discipline is now nearly two decades old and faces the natural test of any long-lived organisational reform: whether it survives the next generation of underwriters and the next downturn in pricing. The foreign capital looking at Tokio Marine as partner, counterparty, or benchmark is largely betting that it does.

FAQ

How large is Tokio Marine Holdings’ international business relative to Japan?

Approximately half of the group’s adjusted net income now comes from international business, with the United States as the single largest country contributor. Domestic Japan remains the largest source of premium income, but profit contribution from outside Japan has risen sharply since the Philadelphia, Delphi, HCC, and Pure acquisitions, and is now broadly comparable in scale to the domestic non-life profit pool.

What did Tokio Marine acquire in the United States and when?

Four principal acquisitions: Philadelphia Consolidated Holding (Philadelphia Insurance Companies) in December 2008 for approximately $4.7 billion; Delphi Financial Group in 2012 for approximately $2.7 billion; HCC Insurance Holdings in October 2015 for approximately $7.5 billion; and Pure Group in February 2020 for approximately $3.1 billion. Together they produced what is now the largest international platform of any Japanese non-life insurer.

How does Tokio Marine compare to SOMPO Holdings and MS&AD?

The three groups together hold the substantial majority of Japan’s non-life market. MS&AD typically reports the largest domestic non-life share, Tokio Marine the largest international profit pool, and SOMPO the broadest domestic diversification (including nursing care). All three pursued international expansion through the 2010s, but Tokio Marine concentrated on the US primary specialty and high-net-worth personal lines markets, while SOMPO acquired Endurance Specialty and MS&AD acquired Amlin’s Lloyd’s franchise.

Who is the CEO and where is Tokio Marine headquartered?

Satoru Komiya has served as President and Group CEO since June 2019. The group is headquartered in the Marunouchi district of Tokyo. Tokio Marine Holdings, Inc. is listed on the Tokyo Stock Exchange under code 8766, with Tokio Marine & Nichido Fire Insurance Co., Ltd. as its principal domestic operating subsidiary.

What was the “loss profit” issue in Japanese non-life insurance?

Through the late 1990s and early 2000s, Japanese non-life insurers wrote policies whose technical underwriting result was negative, in the expectation that investment income on the premium float would compensate. As Japanese long-term interest rates fell toward zero, that assumption became untenable. The post-2004 Tokio Marine & Nichido led a return to disciplined underwriting — declining underpriced policies, repricing auto and commercial books, exiting unprofitable distribution arrangements — and the rest of the now three-group market followed.

Working with Tokio Marine

Japonity helps foreign reinsurers, brokers, and corporate risk buyers build relationships with Japan’s largest insurance groups, including Tokio Marine Holdings and its operating subsidiaries. We provide structured introductions to the right buying centres, market intelligence on the Japanese non-life and life markets, and support for the operational and regulatory work that sits behind any cross-border insurance or reinsurance relationship in Japan. Reach out via /business-matching/ to start a conversation.

Related from Japonity — Japan’s non-life insurers

- SOMPO Holdings — The Bigmotor scandal, the senior-care pivot, and the Endurance trade

- MS&AD Insurance Group — Japan’s most internationally-built non-life insurer

Want to source Japanese products beyond these company profiles? Japonity also runs a Japan Sourcing Hub — a research-grade catalogue of 1,185 verified Japanese food products and 200+ overseas EC stores, ready for B2B procurement.

Interested in Japanese business opportunities?

Whether you're looking for technology partners, engineering talent, or market insights — we can help connect you with the right Japanese organizations.

Get in Touch →