In December 2020, Nippon Telegraph and Telephone Corporation paid approximately JPY 4.3 trillion (roughly USD 40 billion) to buy out the public minority of NTT Docomo, its mobile subsidiary and Japan’s largest mobile carrier with around 80 million subscribers. It was the largest take-private in Japanese corporate history, and it consolidated under one roof what is arguably the world’s largest privately held telecommunications operator by capital expenditure. The Japanese government still owns approximately one-third of NTT itself — a residue of the 1985 privatization that broke up the postwar telecom ministry — and uses that stake to nudge NTT toward national-priority projects. The most ambitious of these is IOWN, the Innovative Optical and Wireless Network: an attempt to rebuild the global communications and compute stack around photons rather than electrons, with a 2030 deadline. NTT Data, the group’s global IT services arm, has meanwhile bolted on Dimension Data, Keane, and NTT Limited to build a multi-continent integrator that competes with Accenture and Tata Consultancy Services. For foreign buyers, investors, and licensors, NTT is no longer a domestic monopoly — it is a Japanese champion that has chosen to bet on a particular vision of the next computing era.

From state monopoly to listed champion

NTT’s lineage runs through the Japanese postwar settlement. The Nippon Telegraph and Telephone Public Corporation (Denden Kosha) was carved out of the Ministry of Communications in 1952, charged with rebuilding the country’s destroyed copper telephone network and extending it to every household. For three decades it held a statutory monopoly. By the early 1980s, with the network largely built and the rest of the OECD experimenting with telecom liberalization, the Nakasone administration moved to break it open. In April 1985 — the same year that brought the breakup of Japanese National Railways into the JR companies — Denden Kosha was converted into a joint-stock company, Nippon Telegraph and Telephone Corporation, and listed on the Tokyo Stock Exchange under code 9432.

The initial public offering, in 1987, was at the time the largest in world history. The Japanese government retained majority ownership for years afterward, gradually selling down to comply with NTT Law, which today requires the state to hold at least approximately one-third of outstanding shares. That floor is more than ceremonial. It gives the Ministry of Internal Affairs and Communications (MIC) a permanent regulatory and political handle, and it ensures that questions of national infrastructure — submarine cables, 6G research, semiconductor sovereignty — pass through NTT’s boardroom whether NTT seeks them or not. The arrangement is sometimes uncomfortable for activist investors but it is also the reason NTT can credibly underwrite a fifteen-year research bet like IOWN without quarterly shareholder mutiny.

The group: a federation, not a unitary firm

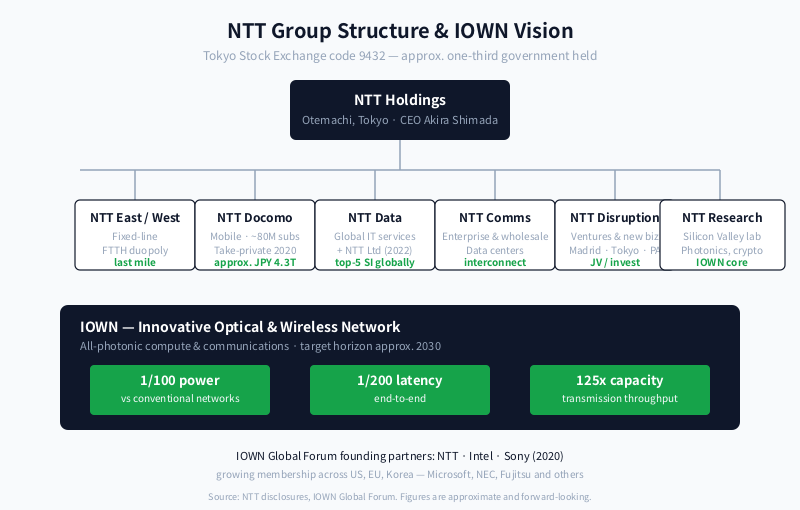

Most foreign observers underestimate how federated NTT is. The Tokyo Otemachi holding company sits atop a constellation of operating subsidiaries that were, in many cases, mandated by regulators to remain structurally separate to preserve competition.

| Entity | Role | Foreign-buyer relevance |

|---|---|---|

| NTT East / NTT West | Regional fixed-line monopolists (FTTH, copper). Mandatory east-west split for competition. | Last-mile access for any Japanese on-premise deployment. |

| NTT Docomo | Mobile carrier, ~80M subscribers, #1 in Japan. Wholly owned since 2020. | 5G/6G partnerships, MVNO wholesale, IoT SIM at scale. |

| NTT Data | Global IT services integrator, dual-listed (TSE 9613 prior to 2025 consolidation). | Direct M&A target / vendor for enterprise IT, banking, public sector. |

| NTT Communications | Enterprise, wholesale long-distance, data center operator. | Carrier-neutral interconnect, Japan colocation, SD-WAN. |

| NTT Disruption | Venture & new-business unit (Madrid, Tokyo, Palo Alto). | Startup investment, joint ventures outside legacy telecom. |

| NTT Research | Silicon Valley basic-science lab (cryptography, biocomputing, photonics). | Academic and licensing partnerships, IOWN R&D. |

This federation has consequences. A foreign software vendor selling into NTT East does not, by default, have a foothold in NTT Docomo. Procurement, technical standards, and even office buildings are different. The 2020 Docomo take-private and the 2022 integration of NTT Limited into NTT Data were the two biggest moves of the past decade toward simplifying this map, but the federated structure remains the default mental model for anyone selling to or partnering with the group.

The Docomo take-private: why it mattered

NTT Docomo was spun off as a separate listed company in 1998 and rode the 2G/3G boom to become a household name globally — i-mode, in the late 1990s, was for a brief moment the most-used consumer internet service in the world. By the late 2010s, however, the strategic logic of separation had inverted. Mobile and fixed networks were converging on IP, capex on 5G was unforgiving, and the Japanese government — under both Abe and Suga administrations — was openly pressuring carriers to cut consumer mobile tariffs. A separately listed Docomo would have had to fight that political battle while defending its own minority shareholders. Inside the wholly owned NTT group, the math was easier: cross-subsidize, integrate, and use NTT’s balance sheet to fund the 6G and IOWN research that no pure-play mobile carrier could afford.

The tender offer launched in September 2020 and closed in December. The price, approximately JPY 3,900 per share, was a roughly 40% premium to the pre-announcement market price. Total deal value reached approximately JPY 4.3 trillion. At the time it was the largest tender offer ever recorded in Asia. Foreign investors who held Docomo as a yield play exited; foreign investors who held NTT itself saw their indirect exposure to Japan’s mobile market reconcentrate. The take-private is now the cleanest single explanation for why NTT’s reported capex and R&D lines look the size they do.

NTT Data: the global integrator most foreigners have heard of

If a foreign executive has heard of any NTT subsidiary, it is usually NTT Data. Founded in 1988 as the data-processing arm of the parent, NTT Data spent the 2000s acquiring its way into Europe (Itelligence, the SAP integrator) and the 2010s acquiring its way into North America, most consequentially through the 2016 purchase of Dell Services, the former Perot Systems business that Dell had inherited and decided to divest. That single transaction, at approximately USD 3 billion, gave NTT Data a credible US public-sector and healthcare-IT footprint.

In 2022, NTT announced the integration of NTT Limited — itself the product of merging Dimension Data, NTT Communications’ international arm, and NTT Security — with NTT Data, creating a single global brand for enterprise IT services. The combined entity competes directly with Accenture, Capgemini, Tata Consultancy Services, and Infosys for outsourcing, application development, SAP implementation, and increasingly cloud migration work. NTT Data is now in the global top five IT services firms by revenue. For foreign software vendors, this matters because NTT Data is both a channel (selling foreign products into Japan’s keiretsu-bound enterprise market) and a competitor (bidding for the same outsourcing contracts). For foreign acquirers, it has historically been a buyer rather than a seller — a hunter of mid-cap regional integrators.

IOWN: the all-photonic bet

IOWN, the Innovative Optical and Wireless Network, is the project that most clearly distinguishes today’s NTT from any other global telecom incumbent. Announced in 2019 and codified through the IOWN Global Forum (co-founded with Intel and Sony in 2020), it is an architectural proposal: replace the electronic interconnects inside data centers, between data centers, and ultimately between compute elements on a chip, with photonic ones. The pitch numbers are striking. NTT targets approximately one-hundredth the power consumption of conventional networks, approximately two-hundredth the end-to-end latency, and a 125-fold increase in transmission capacity, all by approximately 2030.

The strategic logic is twofold. First, electricity. AI workloads — and especially inference at scale — are now constrained by power and heat, not by transistor density. If photons can do at the rack and data-center scale what they already do over long-haul fiber, the energy curve of compute bends. Second, sovereignty. Japan is not going to out-compete Taiwan in leading-edge silicon foundry capacity in this decade. But it has, through NTT and a small number of universities, a deep bench in optical communications, integrated photonics, and silicon photonics packaging. IOWN is, in part, an industrial-policy bet to position Japan in a stack where it can lead rather than follow. The Global Forum membership — which includes Intel, Sony, NVIDIA-adjacent ecosystem players, Microsoft, NEC, Fujitsu, and a growing list of European and Korean partners — is the leading indicator of whether this thesis travels.

The honest caveat: IOWN is, today, more a research program with deployments at the periphery (data-center interconnect trials, optical compute prototypes) than a deployed product line. The 2030 target dates are real but ambitious. Foreign investors should treat IOWN the way they treat any moonshot from a balance-sheet-rich incumbent: optionality with a long fuse, not a near-term cash flow.

The competitive map: NTT versus KDDI versus SoftBank

Japanese mobile is, structurally, a three-way oligopoly. NTT Docomo is the largest by subscriber count; KDDI (au brand) is second; SoftBank is third. A fourth entrant, Rakuten Mobile, has tried since 2020 to break in with a cloud-native open-RAN architecture but has struggled to reach profitability. The three incumbents differ in instructive ways. KDDI is the most enterprise-and-IoT focused, with a strong DX and connected-car position. SoftBank is the most consumer-and-platform focused, with deep ties to Yahoo Japan / LY Corporation and to founder Masayoshi Son’s broader investment vehicle. NTT, post-Docomo-buyout, is the most vertically integrated — owning the fixed network, the mobile network, the data centers, the integrator, and the photonic-network research program in one corporate group.

For a foreign technology vendor entering Japan, this map dictates go-to-market. Selling an AI inference platform? NTT’s IOWN partnerships and NTT Data’s enterprise channel are the natural fit. Selling a consumer payment app? SoftBank/LY Corp is the natural partner. Selling industrial IoT to factories? KDDI and NTT both bid for those deals, often as systems integrators on top of their own connectivity.

Governance, regulation, and the one-third stake

The Japanese government’s approximately one-third holding in NTT is held by the Minister of Finance. Several proposals have surfaced in recent years — most prominently from politicians associated with defense-budget financing — to sell down or eliminate the stake. In 2024 the LDP convened a working group to revisit NTT Law itself, with the most ambitious option being full repeal. Two arguments structure that debate. The reform argument is that NTT, as a globally competing telecom-and-IT group, should not be hamstrung by Japan-specific board-composition and R&D-disclosure obligations that its rivals (KDDI, SoftBank, Verizon, Deutsche Telekom) do not face. The conservation argument is that NTT controls assets — the fixed-line backbone, the submarine cable landing stations, the IOWN research — that are inseparable from national security and should not be entirely market-governed.

Akira Shimada, who became president and CEO in 2022, has navigated this debate by emphasizing global competitiveness without openly campaigning for repeal. His predecessor Jun Sawada was the architect of both the Docomo take-private and the original IOWN announcement; Shimada inherited those bets and is now responsible for execution. Foreign investors should expect the NTT Law debate to continue throughout this decade and to be the single largest non-operational driver of NTT’s equity story.

What this means for foreign counterparties

NTT is not a single counterparty. It is a holding company with a global IT services arm that will sell to you, a mobile carrier that may distribute your consumer product, a research lab that may license your IP, and a venture unit that may invest in your startup. For foreign software vendors, the cleanest entry point is usually NTT Data, which has a procurement process recognizable to anyone who has sold into a global SI. For foreign hardware and photonics players, the IOWN Global Forum is the cleanest entry point — membership is open, the technical working groups are productive, and being inside the standards conversation early is more valuable than chasing individual pilots. For foreign acquirers, NTT itself is rarely a seller; NTT Data is occasionally a buyer of mid-sized integrators. For foreign investors, the equity story is governance-heavy and capex-heavy: it rewards patience and rewards a specific view on whether the IOWN bet pays out by approximately 2030.

FAQ

Who owns NTT, and how much does the Japanese government hold?

NTT is listed on the Tokyo Stock Exchange under code 9432. The Japanese government, via the Ministry of Finance, holds approximately one-third of outstanding shares — a floor mandated by NTT Law. The remainder is held by institutional investors (Japanese and foreign), retail investors, and through index inclusion.

What exactly is IOWN and when will it be real?

IOWN — Innovative Optical and Wireless Network — is NTT’s proposal to replace electronic interconnects with photonic ones across networks, data centers, and eventually compute itself. Headline targets are approximately one-hundredth the power consumption and approximately two-hundredth the latency of conventional networks by approximately 2030. Early deployments (long-haul interconnect, data-center fabric trials) are ongoing through the IOWN Global Forum.

How is NTT Data different from NTT Communications?

NTT Data is a global IT services and systems integration business — it builds and runs IT for banks, governments, and large enterprises worldwide. NTT Communications is the enterprise and wholesale arm of the connectivity business — long-distance, data centers, interconnect. Since 2022, NTT Limited (the former international arm of NTT Communications) has been integrated into NTT Data, simplifying the global brand architecture.

Why did NTT take Docomo private in 2020?

To consolidate strategy and capex under a single roof. The publicly listed Docomo would have had to balance Japanese government pressure on consumer mobile tariffs against minority-shareholder returns. Inside the wholly owned group, NTT can cross-subsidize 6G and IOWN research and absorb tariff pressure without that conflict.

How does NTT compare to KDDI and SoftBank in Japan?

The three are a structural oligopoly in Japanese mobile. NTT Docomo is the largest by subscriber count (approximately 80 million). KDDI is enterprise-and-IoT focused; SoftBank is consumer-platform focused via LY Corporation; NTT is vertically integrated across fixed, mobile, data centers, integration, and research. Rakuten Mobile is a smaller challenger entrant.

Working with NTT Group

If your business intersects with NTT — as a software vendor selling into NTT Data’s global delivery, a hardware or photonics partner exploring the IOWN ecosystem, an enterprise buyer evaluating NTT Communications data-center capacity, or a foreign investor mapping Japan’s telecom equity landscape — Japonity can help you identify the right counterparty inside the group and prepare a credible English-language approach. Japan’s enterprise procurement remains relationship-mediated, and entering through the wrong subsidiary can cost a year of cycles. Visit our business matching service to start a conversation grounded in the actual map of how NTT is structured today.

Related from Japonity — Japan’s telecom & digital ecosystems

- SoftBank Group — From PHS reseller to Arm + Stargate AI infrastructure giant

- Rakuten Group — The points-economy empire and the mobile bet that almost broke it

- LY Corporation (LINE Yahoo) — Japan’s super-app holding company — SoftBank + Naver under government pressure

- DeNA — From Mobage to BayStars to Pococha to MaaS — Japan’s most under-appreciated reinvention

- KDDI Corporation — Japan’s #2 mobile carrier and the Mitsubishi-shosha-linked telco

Want to source Japanese products beyond these company profiles? Japonity also runs a Japan Sourcing Hub — a research-grade catalogue of 1,185 verified Japanese food products and 200+ overseas EC stores, ready for B2B procurement.

Interested in Japanese business opportunities?

Whether you're looking for technology partners, engineering talent, or market insights — we can help connect you with the right Japanese organizations.

Get in Touch →