Step out of Kamiyacho station in central Tokyo and the skyline that has reshaped the capital over the past decade is visible in a single arc. To the east rises Toranomon Hills, Mori Building’s gleaming office cluster anchored by the country’s tallest pre-pandemic tower. A short walk south stands Azabudai Hills, the 64-storey Mori JP Tower that briefly took the title of Japan’s tallest building when it opened in 2023. Further across the river, the Tokyo Sky Tree’s 634-metre lattice has dominated the eastern horizon since 2012. The three projects are separated by a decade, different developers, and architectural styles ranging from postmodern glass to neo-traditional spire. They share one common contractor on their primary build records: Kajima Corporation, the 186-year-old Tokyo-listed construction house that, alongside Obayashi, Taisei, Shimizu and the unlisted Takenaka, forms Japan’s “super-zenecon” — the five general contractors that build the country’s largest, tallest, most seismically demanding and most politically sensitive structures. Kajima is the second-oldest of the five, traces its origins to a single carpenter’s shop opened in Edo in 1840, and today carries an order book that exceeds two trillion yen, with overseas subsidiaries from Los Angeles to Sydney to Singapore. For foreign investors trying to read Japan’s mega-redevelopment cycle, semiconductor-fab construction boom and decarbonisation infrastructure pipeline, Kajima is one of the most concentrated single bets available.

From Edo carpenter to super-zenecon

Kajima’s founding date — 1840 — is older than most of the firms it works with, older than Japan’s modern state, and older than any other listed super-zenecon by several decades. In that year a carpenter named Iwakichi Kajima opened a small construction shop in central Edo, the city that would be renamed Tokyo in 1868. The business specialised in traditional wooden buildings: merchant townhouses, warehouses, the kind of structures that defined the city before Meiji-era industrialisation. It survived the political collapse of the shogunate, the fires that periodically gutted the wooden capital, and the migration of artisanal trades into industrial firms.

The transition into modern construction came in the second generation. Kajima moved into railway tunnels and bridges during Japan’s first wave of rail building in the 1880s, then into reinforced-concrete office buildings and government works as Tokyo rebuilt after the 1923 Great Kanto Earthquake. The company was formally incorporated as Kajima Construction in 1930, retaining family leadership while professionalising its engineering and project-management capabilities. By the late twentieth century it had grown into one of Japan’s “big five” general contractors, a designation that has remained remarkably stable since.

The Japanese term zenecon — abbreviating “general contractor” — describes firms that take single-prime responsibility for design, engineering, procurement and construction of large projects. The prefix super is reserved for the five firms with the deepest balance sheets and the credentials to bid on Japan’s most demanding categories: high-rise towers above roughly 200 metres, nuclear and large hydroelectric works, mass-transit civil engineering, and cleanroom-grade semiconductor fabrication plants.

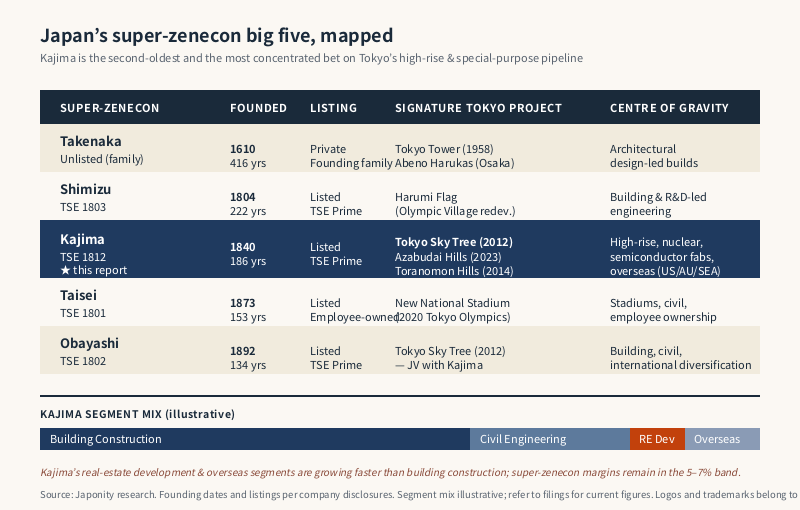

The super-zenecon big five, mapped

The five firms differ in heritage, ownership and emphasis, but they are similar enough in scale and capability that Japanese clients, regulators and lenders treat them as a peer cluster. The table below sketches the comparison.

| Super-zenecon | Founded | Listing | Signature Tokyo project | Centre of gravity |

|---|---|---|---|---|

| Shimizu Corporation | 1804 | TSE 1803 | Harumi Flag (Olympic Village redevelopment) | Building, R&D-led engineering |

| Kajima Corporation | 1840 | TSE 1812 | Tokyo Sky Tree, Azabudai Hills, Toranomon Hills | High-rise, nuclear, semiconductor fabs |

| Taisei Corporation | 1873 | TSE 1801 | New National Stadium (2020 Olympics) | Stadiums, civil engineering, employee-owned |

| Obayashi Corporation | 1892 | TSE 1802 | Tokyo Sky Tree (joint with Kajima) | Building, civil, international diversification |

| Takenaka Corporation | 1610 | Unlisted (family) | Tokyo Tower (1958), Abeno Harukas (Osaka) | Architectural buildings, design-led |

The cluster is unusual by global standards. No other developed economy has five comparably scaled domestic general contractors with this depth of in-house engineering talent. American construction is fragmented between regional builders and pure construction managers who subcontract execution. European peers — Bouygues, Vinci, Hochtief, Skanska — dominate national markets but rarely match the technical breadth of a Japanese super-zenecon, which keeps mechanical, civil, structural and digital engineering under one roof. The closest analogues are Korea’s Samsung C&T and Hyundai E&C, themselves modelled on the Japanese template.

Kajima’s position within the cluster is shaped by two long-standing emphases: high-rise and special-purpose construction. The firm built its reputation through landmark towers — Kasumigaseki Building, Japan’s first modern high-rise, in 1968 — and through nuclear and hydroelectric works that required certifications smaller contractors could not amass. Those credentials still drive its bid pipeline today.

The Tokyo redevelopment cycle

Modern Tokyo is in the largest urban redevelopment cycle since the postwar reconstruction. Behind the visible projects sits a regulatory mechanism — the tokutei toshi saisei or special urban redevelopment framework — that since the early 2000s has allowed developers to assemble large land parcels in central Tokyo and build to substantially higher floor-area ratios than ordinary zoning permits, in exchange for public-realm contributions such as plazas, transit upgrades, district heating and disaster-shelter capacity. It is the reason towers above 250 metres now line Toranomon, Roppongi, Yaesu and Shinagawa, where 150-metre limits applied a generation earlier.

For the super-zenecon, the framework is a structural windfall. Each project is engineered to bespoke seismic specifications, integrates basement-level transit interfaces, and is built on tight central-city sites where sequencing, neighbourhood liaison and crane logistics are themselves competitive advantages. Kajima has been the primary or joint contractor on a disproportionate share of the largest:

- Tokyo Sky Tree (2012) — Joint venture with Obayashi. At 634 metres the world’s tallest free-standing tower at the time of completion and a structural-engineering showcase, with a central-shaft tuned-mass damper system designed to keep the broadcast antenna stable through Tokyo’s seismic activity.

- Toranomon Hills Mori Tower (2014) — Joint venture for the original 247-metre tower anchoring Mori Building’s Toranomon redevelopment, with subsequent towers in the cluster following through the late 2010s and early 2020s.

- Azabudai Hills (2023) — Contractor on the 330-metre Mori JP Tower and surrounding podium structures, completing what is currently Japan’s tallest skyscraper and one of the most expensive private redevelopments ever delivered in central Tokyo.

- Tokyo Disneyland and DisneySea expansions — Long-running contractor relationship with Oriental Land Company for new attraction zones, the most recent being the Fantasy Springs expansion that opened in 2024.

- Semiconductor fabrication plants — Cleanroom-grade construction for TSMC’s JASM facility in Kumamoto and for Kioxia memory fabs in Yokkaichi and Kitakami, segments where only the super-zenecon hold the technical certifications to deliver at scale.

Inside Kajima, the building-construction segment that delivers these projects sits alongside three other reporting segments: civil engineering, real estate development and overseas. The mix has shifted modestly over the past decade as overseas earnings have grown faster than domestic, but Japan still accounts for the majority of group revenue and an even larger share of profit, reflecting both the redevelopment cycle and the higher margins available on technically demanding domestic work.

Civil engineering and the nuclear specialty

The civil-engineering segment is less visible than skyscrapers but commercially important. Kajima builds tunnels, dams, expressways and rail infrastructure, and is one of a small number of firms certified to construct nuclear power facilities. Its credentials include work on the Hamaoka, Tokai and Tomari plants across earlier decades, foundation engineering for fast-breeder reactor research, and decommissioning support at Fukushima Daiichi since 2011.

The nuclear pipeline is in a complicated transition. Most Japanese reactors have remained offline since the 2011 Tohoku earthquake, but policy direction since the 2022 energy crisis has shifted toward restart, life-extension and — for the first time since the disaster — replacement-reactor construction. Kajima’s certifications, retained nuclear engineering staff and specialised subsidiaries such as Kajima Foundation Engineering position the firm as one of the very few contractors that could deliver new domestic nuclear builds if and when policy converts into firm orders.

Adjacent civil-engineering pipelines are larger and more politically straightforward. The Linear Chuo Shinkansen — the Tokyo-Nagoya-Osaka maglev project led by Central Japan Railway — has assigned several tunnel and station packages to Kajima-led joint ventures. Tokyo’s continuing transit expansion, the Tohoku Shinkansen extension to Sapporo, and climate-adaptation programmes for river control and coastal protection all flow partially through super-zenecon work books.

The overseas franchise

Kajima’s international footprint is older and deeper than most of its domestic peers’. The firm established Kajima International in the United States in the 1960s, and through its subsidiary Kajima USA today operates regional offices in New York, Atlanta, Los Angeles and other markets. Kajima Australia, founded in the 1980s, is one of the larger Japanese-owned construction businesses in the country, with a portfolio that includes commercial and residential building in Sydney, Melbourne and Brisbane. Kajima Overseas Asia, headquartered in Singapore, leads activity across ASEAN markets including Vietnam, Indonesia, Thailand and the Philippines, where the firm pursues mixed-use, hospitality and industrial work.

Internationally, Kajima has positioned itself less as a single global brand than as a federation of regional construction businesses operating under common ownership, each tailored to local procurement norms. The US business builds primarily for industrial, distribution and Japanese-affiliate clients; the Australian business is more diversified into commercial and residential development; the ASEAN business follows Japanese manufacturing FDI and increasingly serves local developers as well.

For overseas infrastructure investors and developers, the implication is that Kajima behaves differently from a typical Japanese exporter. It is not selling a product into foreign markets; it is operating with local staff under local procurement rules in each jurisdiction, with the parent providing balance-sheet, technical, and reputational backing. That makes it a more accessible counterparty than firms whose international engagement is intermediated through Tokyo headquarters.

Real estate development and the diversification debate

The fourth Kajima segment — real estate development — has grown quietly. Through Kajima Real Estate and Kajima Sangyo, the firm holds investment stakes in office buildings, logistics facilities and residential complexes across Japan, often in projects where Kajima also acted as contractor. The model is structurally similar to that of Japan’s sogo shosha trading houses in property, and raises the same question: is the firm a builder that holds property, or a property holder that also builds?

The answer matters because real estate carries different return profiles than contract construction. Domestic construction margins have historically been thin — five to seven percent operating margin at the segment level — whereas development can deliver higher returns on equity when timed well, and worse during downturns. Kajima has tilted incrementally toward development exposure, especially in central Tokyo office and logistics, partly as a hedge against the eventual end of the current redevelopment cycle.

The semiconductor pipeline raises a related question. The construction of TSMC’s Kumamoto fabs and Kioxia’s expansions has been one of the most lucrative pockets of the domestic market since 2022, but each fab is built once and produces a multi-year revenue tail rather than a recurring stream. Kajima and its peers are exploring fab-adjacent infrastructure — substations, water treatment, cleanroom maintenance — to convert one-shot construction wins into longer-lived service relationships.

Governance, leadership and culture

Kajima’s leadership has historically rotated within a relatively small group of long-serving executives, and the firm has been led for much of the past two decades by members and successors of the founding family alongside professional managers. President Yoshikazu Amano, in post since 2024, succeeded Hiromasa Amano and continues the engineering-led leadership tradition that has characterised the firm.

The internal culture is engineering-heavy in ways that surprise visitors from finance-driven Western contractors. Site engineers spend years in field assignments before rotating into corporate roles. Specialist groups in seismic design, deep-foundation engineering and large-span structures retain hundreds of doctoral-level researchers, and the firm publishes original research in academic journals. Kajima Technical Research Institute, established in 1949 and one of the largest private construction-research facilities in the world, develops proprietary anti-seismic systems, automated construction equipment, and digital-twin platforms that are then deployed across the company’s project portfolio.

The cultural mix matters for investors thinking about the firm’s resilience. Construction is cyclical and labour-intensive, and the Japanese industry faces demographic pressure from a shrinking and ageing construction workforce. The super-zenecon are responding through automation — robotic welding, autonomous heavy equipment, AI-assisted scheduling — and Kajima’s R&D scale gives it a strong position in that transition. Its joint development of automated tunnel-boring systems with Komatsu, and its prefabricated modular building systems for hotels and logistics, are early signals of how the firm intends to defend margin as labour costs rise.

What comes next

The Tokyo redevelopment cycle still has visible runway. Mori Building, Mitsubishi Estate, Mitsui Fudosan and Tokyu have multi-decade master plans for Toranomon, Yaesu, Shibuya and Shinagawa that imply continued demand for super-zenecon capacity at least through the late 2030s. The semiconductor pipeline is in early innings, with TSMC’s second Kumamoto fab in active construction and additional capacity announced in Hokkaido. The Linear Chuo Shinkansen, despite environmental and political delays, will require sustained civil-engineering work into the 2040s. And the policy reopening toward nuclear, if it converts into firm orders, will favour the small group of contractors with retained nuclear capability.

The risks are visible too. The redevelopment cycle is concentrated in central Tokyo and exposed to interest-rate and office-demand shocks. Construction labour shortages may compress margin faster than automation can offset. International expansion has been steady but not transformative; overseas earnings depend heavily on Japanese FDI rather than independent franchise strength.

For now, Kajima sits in the rare position of being a 186-year-old company whose next decade looks more interesting than the last. The 1840 carpenter’s shop in Edo is now a multi-segment construction group with the technical credentials, balance sheet and overseas footprint to compete on projects that few other firms in the world could deliver.

FAQ

Who founded Kajima Corporation and when?

Kajima was founded in 1840 by Iwakichi Kajima as a carpenter’s shop in central Edo, the city later renamed Tokyo. The business transitioned into modern construction during the late nineteenth century, moving into railway and reinforced-concrete work, and was formally incorporated as Kajima Construction in 1930. Headquartered in Akasaka, Tokyo, it is today one of Japan’s “super general contractors” alongside Obayashi, Taisei, Shimizu and Takenaka.

What does it mean to be one of Japan’s “super-zenecon” big five?

The term super-zenecon is industry shorthand for the five Japanese general contractors with the deepest balance sheets, broadest in-house engineering capacity, and technical certifications to deliver Japan’s most demanding projects. The members are Obayashi (founded 1892), Kajima (1840), Taisei (1873), Shimizu (1804) and Takenaka (1610). The first four are listed on the Tokyo Stock Exchange; Takenaka remains privately held by its founding family. Together they dominate Japanese high-rise, nuclear, semiconductor-fab and large civil-engineering construction.

Which major Tokyo projects has Kajima delivered?

Kajima’s signature Tokyo credits include the Tokyo Sky Tree (completed 2012, joint venture with Obayashi), Toranomon Hills Mori Tower (2014, joint venture), Azabudai Hills and the 330-metre Mori JP Tower (2023, currently Japan’s tallest skyscraper), expansions at Tokyo Disneyland and DisneySea including the Fantasy Springs zone (2024), and Kasumigaseki Building (1968, Japan’s first modern high-rise). The firm is also active in semiconductor-fab construction for TSMC’s Kumamoto facility and Kioxia’s memory plants.

How large are Kajima’s overseas operations?

Kajima operates internationally through regional subsidiaries: Kajima USA (with offices across the United States), Kajima Australia (active in Sydney, Melbourne and Brisbane), and Kajima Overseas Asia (headquartered in Singapore, with activity across Vietnam, Indonesia, Thailand and the Philippines). Overseas revenue contributes a meaningful and growing share of group earnings, though Japan still accounts for the majority of revenue and profit. The firm positions itself internationally as a federation of locally embedded businesses rather than a single global brand.

What is Kajima’s exposure to nuclear and semiconductor construction?

Kajima is one of a small number of Japanese contractors certified to build nuclear power facilities, with historical work on the Hamaoka, Tokai and Tomari plants and decommissioning support at Fukushima Daiichi. The 2022 policy reopening toward reactor restart and replacement construction has improved the long-term outlook for nuclear orders. In semiconductors, Kajima has been involved in cleanroom-grade construction for TSMC’s Kumamoto fabs and Kioxia memory facilities, segments where only the super-zenecon hold the necessary technical certifications.

Working with Kajima

For overseas developers, infrastructure investors, semiconductor operators and corporate occupiers planning major construction or facility programmes in Japan or wider Asia, the super-zenecon — and Kajima in particular, given its high-rise, special-purpose and overseas credentials — are essential counterparties. Japonity introduces qualified overseas companies to Japanese general contractors, real estate developers and infrastructure operators through its business matching service. If you are exploring a Japan-market construction project, a semiconductor or industrial facility build, an overseas joint venture, or a co-investment alongside a super-zenecon, get in touch to start a conversation.

Related from Japonity — Japan’s super-general contractors (zenecon)

- Obayashi Corporation — The 1892 super-zenecon — Tokyo Sky Tree, Marina Bay Sands, Burj Khalifa

- Taisei Corporation — Employee-owned super-zenecon — Tokyo Olympic Stadium, Esconfield

- Shimizu Corporation — The 1804 super-zenecon — Tokyo Sky Tree, Akashi-Kaikyo, Lunar Ring

- Takenaka Corporation — The 1610 super-zenecon — Tokyo Tower, Tokyo Dome, Roppongi Hills (unlisted)

Want to source Japanese products beyond these company profiles? Japonity also runs a Japan Sourcing Hub — a research-grade catalogue of 1,185 verified Japanese food products and 200+ overseas EC stores, ready for B2B procurement.

Interested in Japanese business opportunities?

Whether you're looking for technology partners, engineering talent, or market insights — we can help connect you with the right Japanese organizations.

Get in Touch →