When Warren Buffett disclosed in August 2020 that Berkshire Hathaway had quietly accumulated stakes in Japan’s five general trading houses, the news rippled through Tokyo’s financial district. By 2023 he had increased those holdings, and by 2025 each position had moved beyond 9 percent. Among the five, Itochu Corporation occupied a peculiar place: less famous abroad than Mitsubishi Corporation, smaller in headline assets than Mitsui & Co., yet consistently more profitable on a per-employee basis and far more exposed to consumer-facing businesses. The same year that Buffett’s bet became public, Itochu was completing the take-private of FamilyMart, the convenience-store chain it had owned partially for decades. A few years earlier it had taken control of Dole Food’s global packaged-fruit operations. It licensed Converse in Japan, owned the jeans heritage brand Edwin, and held a strategic equity tie-up with CITIC and Charoen Pokphand spanning Greater China and Southeast Asia. For a sector that outsiders still associate with iron ore and LNG cargoes, Itochu looked different — and that difference, rooted in 168 years of merchant culture from Shiga Prefecture, is the reason it earned a place in Buffett’s portfolio.

The Omi merchant who became a sogo shosha

Itochu’s origin story begins in 1858, the same year the Tokugawa shogunate signed the Treaty of Amity and Commerce with the United States and the closed country began, reluctantly, to open. A young man named Chubei Itoh I, born into a family of itinerant cloth peddlers in the village of Toyosato in Shiga Prefecture, set out on his first solo trading journey carrying linen and hemp from Omi to wholesalers in Nagasaki and Osaka. He was seventeen.

The detail matters because Toyosato sits in the heartland of the Omi shonin — the Omi merchants — a centuries-old commercial tradition that produced an unusually large share of modern Japan’s great trading firms. Marubeni traces its roots to the same Itoh family. Takashimaya, Daimaru, Wacoal, Nippon Life and Toyota’s textile predecessor all carry Omi DNA. What the Omi shonin shared was not a particular product line but a philosophy summarized in the phrase sanpo yoshi: “good for the seller, good for the buyer, good for society.” That three-way balance, drilled into apprentices through generations, distinguished Omi traders from the more transactional Osaka and Edo merchant cultures. It also embedded a long-time-horizon, brand-protecting instinct that maps surprisingly well onto modern stakeholder capitalism.

Chubei Itoh’s linen business grew through the late Meiji period into a textile trader of national scale. By the early twentieth century it had split, recombined and split again, eventually crystallising as two houses — C. Itoh & Co. (today’s Itochu) and Marubeni — that still share a common ancestor and a quiet rivalry. After 1945, like every Japanese trading firm, C. Itoh was forced by Occupation antitrust authorities to dissolve and reassemble, using the rebuild to diversify aggressively beyond textiles without ever abandoning the consumer-goods core that the founder had planted.

What a sogo shosha actually does

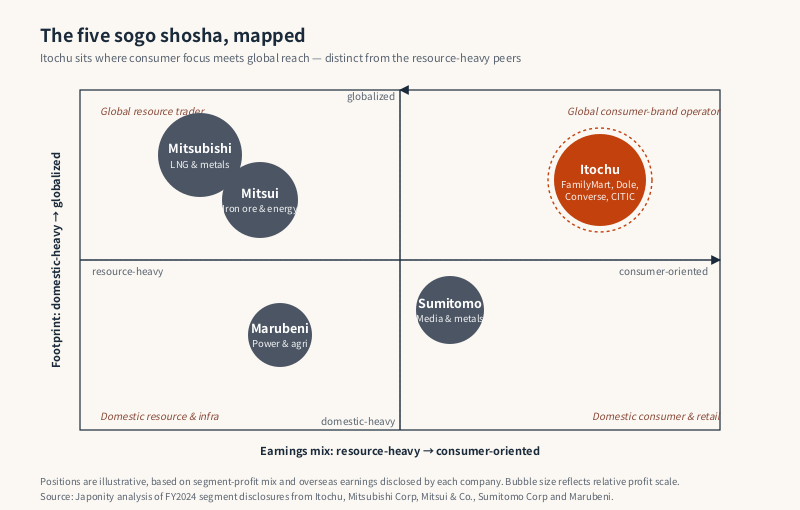

The Japanese term sogo shosha translates literally as “general trading company,” but the description is misleading. A modern sogo shosha is part commodity trader, part private-equity firm, part venture capital house, part project-finance arranger and part logistics operator. The five largest — Mitsubishi, Mitsui, Itochu, Sumitomo and Marubeni — collectively touch every link in the supply chains that feed, fuel, clothe and house the Japanese economy, and increasingly the wider Asian and global economies.

The business model has evolved in waves. In the 1960s and 1970s the houses were primarily middlemen, taking thin margins on enormous volumes. Squeezed by disintermediation in the 1980s and 1990s as manufacturer clients built direct supplier relationships, they pivoted toward investment. By the 2010s the dominant model was equity stakes in producing assets — iron ore mines, LNG fields, copper smelters — supplemented by trading flow those stakes generated. The 2020s have brought another shift: away from upstream resources and toward consumer, digital and decarbonisation plays.

Itochu was earliest and most committed to that pivot. The table below sketches how the five houses differ in segment emphasis.

| Sogo shosha | Heritage core | Modern center of gravity | Signature investee or asset |

|---|---|---|---|

| Mitsubishi Corporation | Heavy industry, resources | LNG, metals, mobility | Lawson, Mitsubishi Motors stake, Australian LNG |

| Mitsui & Co. | Mining, machinery | Iron ore, energy, healthcare | Vale iron ore stake, IHH Healthcare |

| Itochu Corporation | Textiles, Omi merchants | Consumer, food, distribution | FamilyMart, Dole, Converse Japan, CITIC alliance |

| Sumitomo Corporation | Copper, metals | Media, real estate, mobility | Jupiter Telecom, Summit supermarkets |

| Marubeni | Textiles (shared with Itochu) | Power generation, agri-inputs | Helena Agri, overseas IPP portfolio |

The simplification is uncomfortable for insiders, who will rightly note that every house has fingers in every pie. But the relative weighting matters, and it explains why analysts call Itochu the “non-resource sogo shosha.” Roughly two-thirds of its profit comes from non-resource segments in a typical recent year, against materially lower shares at Mitsubishi and Mitsui.

The consumer pivot, illustrated

If a single transaction symbolises Itochu’s strategy, it is the FamilyMart take-private completed in 2020. FamilyMart is Japan’s second-largest convenience store chain, with roughly 16,000 stores domestically and several thousand more across East and Southeast Asia. Itochu had held a minority stake since the 1990s, raised it to around 50 percent in 2018 after FamilyMart’s merger with the Uny conglomerate, and then launched a tender offer in 2020 to acquire the remaining shares. By the time the deal closed, FamilyMart was a wholly owned subsidiary, removed from the Tokyo Stock Exchange and re-engineered as the spine of Itochu’s domestic consumer ecosystem.

The strategic logic ran in several directions at once. As an owner rather than a partner, Itochu could redirect FamilyMart’s purchasing through Itochu-controlled food and apparel suppliers, lift private-label penetration, and harvest data from roughly 15 million daily customers. The chain became a distribution outlet for Itochu’s Dole-branded fresh fruit, a sales channel for textiles produced through Itochu’s apparel network, and a fintech platform via FamiPay. None of that synergy was new in concept — Mitsubishi has run the same playbook with Lawson — but Itochu executed it with unusual speed, partly because the company culture has always treated consumer touchpoints as the firm’s natural habitat rather than an awkward adjunct.

Dole tells a parallel story. In 2013 Itochu paid about 1.7 billion dollars for the global packaged-foods and Asian fresh-produce businesses of Dole Food Company, the iconic American pineapple-and-banana brand. Inside Itochu the deal was understood not as a commodity-agriculture play but as a brand acquisition — a way to attach a globally trusted consumer label to the fruit, vegetable and processed-food flows that Itochu was already moving. A decade on, Dole-branded products are visible across FamilyMart aisles, Japanese supermarkets and Itochu-supplied food-service kitchens, and the company has expanded fresh-produce sourcing through tie-ups in the Philippines, Thailand and Latin America.

Textiles, never abandoned

Most sogo shosha view their textile divisions as legacy operations to be quietly run down. Itochu treats textiles as a strategic franchise. Its Textile Company is the largest of any Japanese trading house and still contributes a meaningful share of group profit, despite the maturity of the domestic apparel market.

The portfolio is unusual. Itochu holds the master licence for Converse in Japan through a long-standing arrangement that has turned the All Star sneaker into a Japanese fashion staple distinct from its American sibling. It owns Edwin, the heritage jeans brand whose denim-mill output supplies Japanese boutiques and overseas premium retailers. It controls Master Brand, an apparel-licensing platform. It distributes a thicket of European luxury labels through joint ventures. And through capital relationships with mills in Okayama, Hiroshima and Wakayama it holds influence over the Japanese denim and uniform-fabric ecosystem that few outsiders ever see.

The textile bet matters strategically because it gives Itochu a competence that none of its rivals can match: brand stewardship in consumer goods. When the company looks at deals like Dole or FamilyMart, it is bringing not just capital and trading muscle but a cultural understanding of how to nurture a label over decades. Inside the sogo shosha cluster, only Itochu still hires textile specialists straight out of university into apparel-merchant career tracks.

The China bet and the CITIC alliance

In 2015, in one of the largest cross-border equity transactions ever executed between Japanese and Chinese corporates, Itochu and the Thai conglomerate Charoen Pokphand jointly invested roughly 1 trillion yen in CITIC Limited, the Hong Kong-listed flagship of China’s state-controlled CITIC Group. Itochu and CP each took around 10 percent of CITIC, giving the trio a tripartite alliance bridging Japan, Thailand and Greater China.

The deal raised eyebrows. CITIC’s portfolio at the time spanned banking, securities, real estate, resources, manufacturing and infrastructure across mainland China — a sprawl whose strategic coherence was opaque even to Beijing-watchers. For Itochu the rationale was relational rather than synergistic in the conventional sense. Through CITIC the firm gained a credentialed Chinese partner for deals across multiple sectors, a structural channel into mainland markets that closed-door foreign players struggle to access, and a co-investment platform with CP Group in food and retail across Southeast Asia. The alliance has produced several joint ventures and a steady flow of equity-method earnings, and it has insulated Itochu from some of the political friction that has buffeted other Japanese firms in China.

The deal is also a piece of evidence in the long-running debate about whether Itochu is run more as a network of relationships than as a balance sheet. Inside the firm, executives talk about “ningen-ryoku” — human capability, the capacity to build and sustain trust across cultures — as a core competence. The CITIC alliance, like the CP partnership and the family-style decision-making within FamilyMart and Dole, are expressions of that ethos.

Governance and culture: the family-business sogo shosha

Among the five major trading houses Itochu has the most distinctive corporate culture, and it shows up in unglamorous places. Headquarters splits between Tokyo and Osaka — a vestige of its Omi origins, since Osaka was historically closer to the Shiga merchant network. Office hours formally start at 8 a.m., an hour earlier than peers, with overtime past 8 p.m. discouraged through systematic monitoring. Cafeteria breakfasts are subsidised. Internal promotion remains the norm; lateral hires at senior levels are rare.

The leadership lineage reinforces the family-business feel. Masahiro Okafuji, who served as president from 2010 and then chairman, has been the dominant figure for more than fifteen years and is unusual in Japanese corporate governance for the duration and visibility of his influence. Keita Ishii currently serves as president and chief executive, having succeeded to operational leadership while Okafuji retained the chairmanship — a transition pattern that Japanese boards often use to bridge generations. The succession has been characterised by stability rather than rupture, and the firm continues to communicate strategy in the long-arc, narrative style associated with founder-led businesses rather than the quarterly cadence of typical Japanese blue chips.

That culture has its critics. Some governance specialists view the concentrated influence as a liability, and the firm’s response to investor pressure on board independence has been incremental rather than transformative. But the same characteristics underpin the patient capital allocation that makes Itochu a Buffett-style holding. The five-trading-house investment is a bet, in part, on cultures that look more like Berkshire than like a typical S&P 500 conglomerate.

The Buffett endorsement

Buffett’s August 2020 disclosure was timed to his ninetieth birthday and explicitly framed as a long-term commitment. He had bought roughly 5 percent of each of the five trading houses through Berkshire Hathaway, financed in part by yen-denominated bond issuance — an elegant carry trade that funded equity stakes with cheap Japanese liabilities. By April 2023 he had raised holdings above 7 percent, and subsequent disclosures pushed several stakes beyond 9 percent. In his 2023 annual letter Buffett singled out the trading houses for cultural praise, citing their compensation discipline, capital-allocation philosophy and willingness to repurchase shares.

Among the five, Itochu fits the Berkshire screen most snugly. It has the highest return on equity, the lowest exposure to volatile commodity prices, the most diversified non-resource earnings, the strongest consumer franchises and a culture that quietly resembles Berkshire’s own owner-operator ethos. None of that means Itochu is the best-performing stock in the basket on any given day, but it explains why analysts often describe it as the “Buffett-iest” of the five.

What comes next

Itochu’s medium-term challenges are familiar across Japanese conglomerates: a shrinking domestic consumer base, intensifying Chinese competition, decarbonisation pressure on energy and materials, and the persistent question of whether the trading-house model can keep generating excess returns as clients build direct supplier relationships. Management’s answer, articulated across recent investor days, is to lean harder into consumer brands, food-security supply chains, healthcare and renewable-energy infrastructure, while running resources for cash rather than growth.

The execution will determine whether the next decade rewards the patient capital that Buffett and a generation of Japanese retail investors have committed. For overseas companies seeking a distribution partner with consumer reach, Itochu remains the most accessible of the major sogo shosha — partly because its DNA was never about heavy industry, and partly because the Omi merchant philosophy still treats every transaction as something to be worked at for the long term.

FAQ

Why did Warren Buffett invest in Itochu and the other Japanese trading houses?

Berkshire Hathaway disclosed approximately 5 percent stakes in each of the five sogo shosha — Mitsubishi, Mitsui, Itochu, Sumitomo and Marubeni — in August 2020, subsequently raising them above 9 percent at each house. Buffett cited the trading houses’ diversified earnings, disciplined capital allocation, low valuations relative to free cash flow and willingness to return capital to shareholders. Itochu in particular fits the Berkshire model with its high return on equity, consumer-oriented portfolio and long-tenure leadership culture.

Why did Itochu take FamilyMart private in 2020?

Itochu had been a long-term minority shareholder in FamilyMart and lifted its stake to roughly 50 percent in 2018 following the chain’s merger with Uny. The 2020 tender offer brought it to wholly owned status, allowing Itochu to integrate FamilyMart’s roughly 16,000 stores with its food, apparel and digital ecosystems without the friction of minority-shareholder governance. The privatisation accelerated cross-business synergies in private-label sourcing, Dole-branded fresh produce distribution and FamiPay fintech, and it removed the chain from quarterly capital-markets pressure.

What did Itochu do with Dole Food after the 2013 acquisition?

Itochu paid approximately 1.7 billion dollars for Dole’s global packaged-foods and Asian fresh-produce divisions in 2013. Inside Itochu the asset is managed as a consumer-brand platform rather than as a commodity-agriculture operation: Dole-branded fruit, juice and packaged products are sold through FamilyMart, supermarkets and food-service channels across Japan and Asia, and the sourcing network has expanded into the Philippines, Thailand and Latin America. The deal is widely cited as a milestone in Itochu’s transition into branded consumer foods.

How does Itochu differ from Mitsubishi Corporation and the other sogo shosha?

All five major sogo shosha overlap heavily in scope, but their centres of gravity differ. Mitsubishi and Mitsui are weighted toward upstream resources — LNG, iron ore, copper, energy infrastructure — which makes their earnings more cyclical. Itochu derives roughly two-thirds of profit from non-resource segments including textiles, food, distribution, ICT and financial services, giving it the most consumer-oriented profile of the five. Sumitomo blends metals with media and real estate; Marubeni is heavy in power generation and agri-inputs.

What is the CITIC alliance and how is it linked to Charoen Pokphand?

In 2015 Itochu and the Thai conglomerate Charoen Pokphand jointly invested roughly 1 trillion yen to acquire equity stakes of around 10 percent each in CITIC Limited, the Hong Kong-listed flagship of China’s state-controlled CITIC Group. The tripartite alliance gives Itochu a credentialed mainland-China partner across banking, real estate, manufacturing and infrastructure, and a co-investment platform with CP Group for food, retail and consumer projects across Southeast Asia. It is one of the largest Japanese-Chinese cross-border equity transactions on record.

Working with Itochu and other sogo shosha

For overseas brands, exporters and capital partners seeking distribution into Japan or co-investment across Asia, the sogo shosha remain unmatched as relationship-led gateways — and Itochu, with its consumer-goods bias and Omi merchant heritage, is often the most natural fit for food, apparel, lifestyle and retail-tech businesses. Japonity introduces qualified overseas companies to Japanese trading houses, brand operators and distributors through its business matching service. If you are exploring a Japan-market entry, a brand licence, a supply-chain partnership or a co-investment with a sogo shosha, get in touch to start a conversation.

Related from Japonity — Japan’s sogo shosha (trading houses)

- Mitsubishi Corporation — The biggest sogo shosha — Lawson take-private and consumer pivot

- Mitsui & Co. — The trading house most exposed to the energy transition

- Sumitomo Corporation — The conservative shosha — steel distribution and J:COM

- Marubeni Corporation — The textile-to-electrons shosha — power IPP, Helena, Gavilon

Want to source Japanese products beyond these company profiles? Japonity also runs a Japan Sourcing Hub — a research-grade catalogue of 1,185 verified Japanese food products and 200+ overseas EC stores, ready for B2B procurement.

Interested in Japanese business opportunities?

Whether you're looking for technology partners, engineering talent, or market insights — we can help connect you with the right Japanese organizations.

Get in Touch →