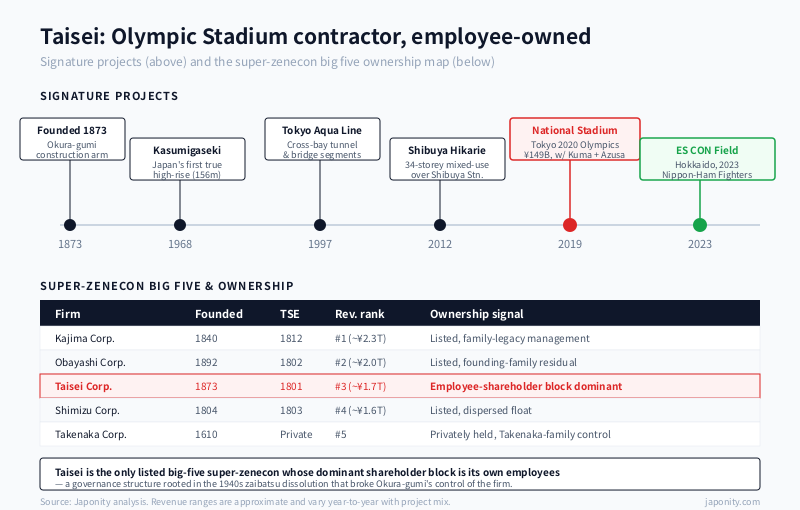

The defining image of Tokyo in 2021 was not a skyscraper but a stadium. The New National Stadium — the 60,000-seat oval that hosted the opening and closing ceremonies of the delayed 2020 Olympic Games — was designed by a team led by Kengo Kuma with Azusa Sekkei and Taisei Design, and constructed under a Taisei-led joint venture. Its laminated timber roof, ringed by Japan-sourced cedar and larch, was deliberately set lower than the rejected Zaha Hadid scheme to defer to the trees of Meiji Jingu Gaien. The stadium was completed in November 2019 on a fixed-price contract, on time, and within budget, after a procurement reset that reduced the original ¥252 billion design to ¥149 billion. For Taisei Corporation — the Shinjuku-headquartered general contractor that took the lead constructor’s role — the project was a national showcase and a reaffirmation of a business model that sets the firm apart inside Japan’s “super-zenecon” big five. Alongside Kajima, Obayashi, Shimizu and the unlisted Takenaka, Taisei is one of the five general contractors that build Japan’s largest, tallest and most technically demanding structures. Unlike its peers, it has no dominant founding family, no controlling sogo shosha shareholder and no anchor institutional block. Its largest single shareholder is its own employee shareholding association — an ownership pattern that quietly shapes how the firm decides, how it pays, and how it absorbs episodes such as the 2023 Sapporo subsidiary affair that has tested its governance reputation.

From Edo trading house to listed contractor

Taisei’s origin is more often told as a trading-house history than a construction one. In 1873, Kihachiro Okura — a Meiji-era merchant already trading guns, leather, food and machinery between Yokohama and the new imperial capital — established Okura-gumi Shokai, a diversified mercantile combine. Within it he set up a construction arm to build the warehouses, dock facilities and government offices Okura’s trading business needed in Tokyo, Osaka and the treaty ports. By the mid-1880s the unit was winning public works of national importance: the Rokumeikan Western-style reception hall (1883), elements of the first Imperial Hotel, and railway, tunnel and harbour projects that defined Meiji modernisation.

In 1917 the construction unit was spun out and incorporated as Taisei Doboku, later renamed Taisei Construction Co. Ltd and then Taisei Corporation. The decisive break with founder-family control came in the late 1940s, when the Allied occupation’s zaibatsu dissolution programme broke up the Okura group and the residual family shareholding in the construction successor was sharply diluted. By the time Taisei re-emerged as a fully reorganised listed contractor, its capital structure had been reshaped around employees, banking partners and the public float — with no single bloc capable of imposing founder-family direction of the kind that still defines Takenaka and, to a lesser degree, Kajima and Obayashi. That history is the reason Taisei today carries Tokyo Stock Exchange code 1801 — the lowest of the listed super-zenecon, allocated in the postwar reorganisation that placed it first among the listed general contractors, ahead of Obayashi (1802), Shimizu (1803) and Kajima (1812).

The super-zenecon big five, mapped

Inside Japan’s contracting industry, “super-zenecon” — the prefix attached to general contractors with the deepest balance sheets and the broadest technical certifications — describes the five firms that can credibly bid on Japan’s most demanding categories: high-rise towers above 200 metres, nuclear and hydroelectric works, mass-transit civil engineering, and cleanroom-grade semiconductor fabrication plants. The five differ in heritage, ownership and emphasis, but they are similar enough in scale and capability that Japanese clients, regulators and lenders treat them as a peer cluster.

| Super-zenecon | Founded | Listing | Signature project | Ownership profile |

|---|---|---|---|---|

| Takenaka Corporation | 1610 | Unlisted | Tokyo Tower (1958), Abeno Harukas | Founding-family controlled |

| Shimizu Corporation | 1804 | TSE 1803 | Harumi Flag (Olympic Village) | Listed, dispersed float |

| Kajima Corporation | 1840 | TSE 1812 | Tokyo Sky Tree, Azabudai Hills | Listed, family legacy in management |

| Taisei Corporation | 1873 | TSE 1801 | New National Stadium (2020 Olympics) | Employee-shareholder-led, no anchor |

| Obayashi Corporation | 1892 | TSE 1802 | Tokyo Sky Tree (JV with Kajima) | Listed, founding-family residual |

The cluster’s relative position has been stable for decades. Annual revenues across the listed four range from roughly ¥1.5 trillion to ¥2.3 trillion, with Taisei in the middle — typically ¥1.6 to 1.8 trillion in a normal year, depending on the timing of large building handovers. Order-book mix, segment emphasis and overseas exposure differ more sharply, and it is at that level that Taisei’s distinctive shape becomes visible.

The employee-ownership characteristic is the clearest single differentiator. Taisei’s largest single shareholder is consistently disclosed as the Taisei Employee Shareholding Association — the in-house ESOP-style vehicle through which thousands of current employees hold company stock — sitting above any institutional or banking holding. Among the super-zenecon this pattern is uniquely entrenched: peers either retain founding-family stakes, anchor cross-shareholdings with main banks, or both. For overseas counterparties used to reading Japanese corporates through the keiretsu lens, Taisei does not quite fit the template.

Segment portfolio: building, civil, development, energy, leisure

Taisei reports through five operating segments — Building Construction, Civil Engineering, Real Estate Development, Energy and Environment, and Leisure and Others — covering a wider functional remit than most peers. Building Construction accounts for roughly 60 to 65 per cent of revenue and includes offices, hotels, hospitals, education facilities, distribution centres and the stadium portfolio. Civil Engineering — tunnels, dams, expressways, rail infrastructure and coastal works — accounts for around 20 per cent. Real Estate Development holds investment positions in central Tokyo office, mixed-use and logistics projects, often where Taisei has also acted as contractor. Energy and Environment groups renewables engineering, remediation, waste-treatment plants and nuclear-decommissioning support. Leisure and Others — historically including resort, golf and recreational operations inherited from bubble-era diversification — is the smallest and most likely to be rationalised under any future portfolio review.

The cumulative effect is more breadth than the average super-zenecon, with slightly less depth in any single specialism. Kajima leads on high-rise towers and nuclear; Obayashi on civil engineering and international diversification; Shimizu on R&D-led building engineering; Takenaka on design-led architectural buildings. Taisei’s positioning has been to be credible across all of these without dominating any one — a trade-off that can mean fewer single-segment leadership awards, but also less concentration risk when any one segment cools.

Signature projects: from Kasumigaseki to the Olympic Stadium

Taisei’s portfolio of completed projects is the most visible argument for its industrial standing. The New National Stadium (2019) is the marquee credit of the recent decade, but it sits within a longer list:

- New National Stadium (2019) — Lead contractor (joint venture with Azusa Sekkei and design lead Kengo Kuma Architects). The 60,000-seat Olympic main stadium, completed on a fixed-price ¥149 billion contract after the reset of the original Hadid scheme, with a laminated-timber roof structure of Japan-sourced cedar and larch.

- Kasumigaseki Building modernisations — Successor refurbishment work on Japan’s first modern high-rise (originally completed in 1968 by Kajima), including seismic retrofit and tenant fit-out programmes that have extended the building’s working life.

- Yokohama Bay Quarter — Mixed-use development adjacent to Yokohama Station, integrating retail, office and transit interface in one of the city’s most heavily used rail nodes.

- Tokyo Bay Aqua-Line — Tunnel sections of the cross-bay road link between Kanagawa and Chiba, one of the most demanding immersed-tunnel and undersea-bored projects in Japanese civil engineering history.

- Tomei Expressway and Shin-Tomei works — Long-running participation in the Tokyo-Nagoya expressway corridor, including bridge, tunnel and interchange sections delivered in joint ventures with peers.

- Shibuya Hikarie (2012) — The 34-storey mixed-use tower above Shibuya Station that anchored the area’s redevelopment ahead of the broader Shibuya remake of the 2010s.

- ES CON Field Hokkaido (2023) — The new Sapporo-area baseball stadium for the Hokkaido Nippon-Ham Fighters, delivered in March 2023 as the first ballpark in Japan’s professional league built around a hospitality-led mixed-use district. The project was widely regarded as a managed-delivery success and underpins Taisei’s continued credibility in large stadium work.

- Nuclear power construction history — Earlier-decade civil and structural work at multiple Japanese nuclear stations, retained certifications, and continued involvement in decommissioning and seismic-safety upgrade programmes.

The stadium portfolio is especially distinctive. Few global contractors have delivered both an Olympic main venue and a privately financed mixed-use ballpark of ES CON Field’s scale within four years of each other. The combination has reinforced Taisei’s standing in large-span, large-roof, high-public-profile work — even as one parallel Sapporo project tested the firm’s governance.

The 2023 Sapporo Dome and subsidiary affair

In late 2023 and into 2024, attention shifted from the Olympic Stadium and ES CON Field to a smaller and more difficult Sapporo story. A Taisei subsidiary engaged in subcontracted civil and renovation work in the broader Sapporo metropolitan area became the subject of disclosures concerning improper accounting and contract administration, with knock-on questions about subcontracting governance and the chain of accountability between the parent and its specialist construction subsidiaries. The episode coincided with the operational distress of the old Sapporo Dome — the city-owned multi-purpose facility largely vacated when the Nippon-Ham Fighters moved to ES CON Field in March 2023 — and the resulting headlines blurred the distinction between the subsidiary’s specific conduct and the broader Sapporo Dome operating issues.

For Taisei the affair forced a renewed focus on subsidiary oversight, internal-audit reach, and the boundary between parent-company execution and subsidiary-led specialist work. Disclosed corrective actions emphasised tighter compliance reviews, leadership rotation in affected units, and additional reporting between subsidiary management and the parent’s risk and compliance functions. None of these are unusual measures, but they carry particular weight at Taisei because the firm’s governance reputation has historically rested on its employee-shareholding structure as a counterweight to the family-aligned or main-bank-aligned governance arrangements that have failed at other Japanese conglomerates. The episode has not unwound that reputation, but it is a reminder that employee ownership is not a substitute for active subsidiary supervision.

Governance, leadership and the employee-shareholder model

Taisei’s senior leadership has rotated within a relatively small group of long-serving executives drawn from inside the firm. President Yoshiyuki Aikawa, in the chief-executive role since 2024, succeeded Tsutomu Shimokai, who led the firm during the National Stadium delivery and the early ES CON Field period. The presidency has not been held by a member of the Okura family for many decades — Taisei’s chief executives have been career engineers and project managers risen from inside the company.

The employee-shareholder structure beneath this leadership is the firm’s quietest but most distinctive feature. The Taisei Employee Shareholding Association — the formal vehicle through which employees hold company stock under payroll-deduction terms — has been the disclosed largest single shareholder for years. The mechanism is straightforward: employees contribute a fraction of monthly pay, the association purchases Taisei shares, and the aggregated position is voted consistently with the long-run interests of the firm. The economic effect is that several thousand current employees hold meaningful equity stakes — modest individually, substantial in aggregate — and no single external bloc can shape strategic decisions without consulting an ownership group that is, in effect, also the workforce.

For outsiders the structure is occasionally misread. It is not formal worker control of the German co-determination type; the board is conventional, with the usual mix of executive, non-executive and independent directors. Nor is it employee ownership in the John Lewis sense, where employees collectively own the underlying firm. It is, more precisely, an unusually high standing concentration of employee shareholding inside an otherwise standard listed-company structure. But for a Japanese super-zenecon — where the alternatives are founding-family control (Takenaka), family-legacy management (Kajima, Obayashi) or dispersed float with cross-shareholdings (Shimizu) — the pattern is genuinely distinctive, and it is the single most-cited reason analysts give for the firm’s historically conservative capital allocation, stable dividend policy and reluctance to pursue debt-funded overseas acquisitions.

Capital allocation, R&D and what comes next

Two structural pressures are reshaping the industry around Taisei. The first is labour scarcity: Japan’s construction workforce has shrunk by roughly a quarter over two decades, and the overtime regulation tightened in 2024 — the so-called “2024 problem” — has further compressed effective capacity. The second is the redirection of capital expenditure toward semiconductor fabs, data centres, decarbonisation infrastructure and Tokyo redevelopment under the special urban-renewal framework. Taisei’s R&D response has emphasised automation, prefabrication and digital-twin construction-management platforms — the Yokohama Technology Centre develops anti-seismic systems, robotic site equipment, large-span roof systems (directly applicable to the stadium portfolio) and the proprietary T-iDigital toolkit. Capital allocation has tilted toward real-estate development positions where Taisei is also the contractor, capturing both construction and ownership margin. Overseas expansion remains modest, concentrated in selected Asian and US engagements rather than a federation of regional businesses — consistent with the conservative, employee-shareholder-driven capital posture.

The Tokyo redevelopment cycle, the semiconductor-fab build-out across Kumamoto and Hokkaido, the nuclear-restart and replacement-reactor pipeline, the stadium and arena cycle ahead of national sporting events, and the energy-transition civil-engineering pipeline all imply continued super-zenecon demand into the late 2030s. Taisei is positioned to capture a share of each. The risks are visible too — labour scarcity may compress margin faster than automation offsets, subsidiary compliance will remain under scrutiny, and international expansion is likely to remain incremental rather than transformative.

FAQ

Who founded Taisei Corporation and when?

Taisei traces its origins to 1873, when Meiji-era merchant Kihachiro Okura established Okura-gumi Shokai, a diversified trading combine that included a construction arm. The construction unit was spun out and incorporated separately in 1917, eventually becoming Taisei Corporation. The Okura family’s controlling shareholding was diluted through the postwar zaibatsu dissolution programme in the late 1940s, after which Taisei reorganised as a fully listed contractor with no dominant founder-family ownership — a structure that remains uniquely distinctive among Japan’s “super-zenecon” big five.

Why is Taisei described as “employee-owned”?

The Taisei Employee Shareholding Association — the in-house vehicle through which thousands of current employees hold company stock under payroll-deduction terms — has consistently been disclosed as the firm’s largest single shareholder. While Taisei is a conventionally governed Tokyo-listed company with a standard board structure, the unusual scale of aggregated employee shareholding sits above any institutional, banking or family bloc. Among Japan’s five super-zenecon, only Taisei carries this pattern; the others rely on founding-family control (Takenaka), family-legacy management (Kajima, Obayashi) or dispersed float with cross-shareholdings (Shimizu).

What is Taisei’s role in the 2020 Tokyo Olympic Stadium?

Taisei led the construction joint venture that built the New National Stadium, the 60,000-seat Olympic main venue completed in November 2019. The architectural design was led by Kengo Kuma in collaboration with Azusa Sekkei and Taisei Design, after the original Zaha Hadid scheme was abandoned in a procurement reset. The final fixed-price contract was approximately ¥149 billion, down from the original ¥252 billion projection, and the stadium’s laminated-timber roof was constructed using cedar and larch sourced from across Japan. The project remains Taisei’s most internationally visible recent credit.

What was the 2023 Sapporo subsidiary affair?

In late 2023 and into 2024, a Taisei subsidiary engaged in subcontracted civil and renovation work in the Sapporo metropolitan area became the subject of disclosures regarding improper accounting and contract administration, with related questions about parent-subsidiary oversight. The episode coincided with the operational distress of the old Sapporo Dome, which had been largely vacated after the Hokkaido Nippon-Ham Fighters moved to Taisei-built ES CON Field Hokkaido in March 2023. Taisei has since strengthened subsidiary compliance, audit reach and reporting; the affair has not unwound the firm’s overall reputation but has reinforced the need for active subsidiary supervision alongside the employee-shareholder governance model.

What are Taisei’s main business segments?

Taisei reports through five operating segments: Building Construction (roughly 60-65% of revenue, including offices, hotels, hospitals, education facilities and stadiums); Civil Engineering (around 20%, including tunnels, dams, expressways and rail infrastructure); Real Estate Development (investment positions in central Tokyo office, mixed-use and logistics); Energy and Environment (renewables engineering, remediation, waste-treatment plants, nuclear decommissioning); and Leisure and Others (resort, recreational and ancillary operations inherited from the bubble-era diversification). The breadth of this segment mix is wider than most super-zenecon peers, though depth in any single specialism is slightly below the cluster leader in that segment.

Working with Taisei

For overseas developers, infrastructure investors, sports-venue operators, semiconductor and energy clients, and corporate occupiers planning major construction or facility programmes in Japan, the super-zenecon — and Taisei in particular, given its stadium, civil-engineering and energy-environment credentials — are essential counterparties. Japonity introduces qualified overseas companies to Japanese general contractors, real estate developers and infrastructure operators through its business matching service. If you are exploring a Japan-market stadium, mixed-use, civil-engineering or energy facility build, a public-procurement joint venture, or a co-investment alongside a super-zenecon, get in touch to start a conversation.

Related from Japonity — Japan’s super-general contractors (zenecon)

- Kajima Corporation — Japan’s super-zenecon — Tokyo Sky Tree, Azabudai Hills, TSMC Kumamoto

- Obayashi Corporation — The 1892 super-zenecon — Tokyo Sky Tree, Marina Bay Sands, Burj Khalifa

- Shimizu Corporation — The 1804 super-zenecon — Tokyo Sky Tree, Akashi-Kaikyo, Lunar Ring

- Takenaka Corporation — The 1610 super-zenecon — Tokyo Tower, Tokyo Dome, Roppongi Hills (unlisted)

Want to source Japanese products beyond these company profiles? Japonity also runs a Japan Sourcing Hub — a research-grade catalogue of 1,185 verified Japanese food products and 200+ overseas EC stores, ready for B2B procurement.

Interested in Japanese business opportunities?

Whether you're looking for technology partners, engineering talent, or market insights — we can help connect you with the right Japanese organizations.

Get in Touch →