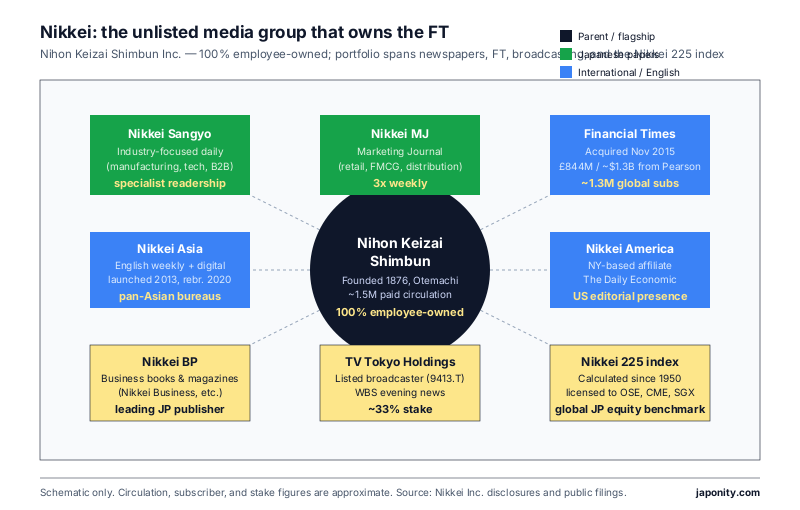

In November 2015, a 139-year-old Japanese newspaper company that no foreign investor could buy a single share in walked into Pearson’s London headquarters and walked out the owner of the Financial Times. The price was approximately £844 million in cash — roughly $1.3 billion at the prevailing exchange rate — and the deal remains, a decade later, the largest acquisition of a foreign media property by any Japanese newspaper. The buyer was Nihon Keizai Shimbun, Inc., known globally by the brand on its English-language properties: Nikkei. It is, in 2026, an institution that is at once instantly recognisable to anyone who has ever traded a Japanese-equity portfolio — the Nikkei 225 stock index it owns is the country’s most cited price level — and almost completely opaque as a corporate entity. There is no listed stock, no founder shareholder, no foreign capital, and no possibility of a hostile bid. The company is owned, every share of it, by its current and former employees.

From a commodity bulletin to Japan’s financial newspaper of record

The company traces its origins to 1876, when Mitsui Bussan — the trading-house ancestor of today’s Mitsui & Co. — began publishing a Tokyo broadsheet called Chugai Bukka Shimpo (“Domestic and Foreign Commodity Bulletin”) to circulate prices for rice, raw silk, cotton, and the other commodities that anchored Meiji-era trade. From that origin two features have proved durable: a primary readership of merchants, bankers, and industrial managers who needed numbers more than narrative, and an editorial centre of gravity squarely on the business of business.

The paper consolidated as Nihon Keizai Shimbun — literally “Japan Economy Newspaper” — in 1942, the wartime title that has carried ever since. Through the post-war reconstruction, the high-growth decades, the bubble and its long unwinding, and the deflationary 2000s, the Nikkei Shimbun became to corporate Japan what the Wall Street Journal was to corporate America: not the largest paper by circulation, but the one decision-makers actually read.

Today the flagship reports a paid circulation in the region of 1.5 million copies, combining print and digital — well below Japan’s mass-market dailies on raw volume but at the absolute top of any global ranking of paid financial newspapers. The Nikkei Shimbun’s online edition, Nikkei Denshiban, has been one of the very few Japanese newspaper digital products to build a paying subscriber base measured in seven figures.

The unlisted company nobody can buy

The single feature that most distinguishes Nikkei from every other major newspaper company in the developed world is its ownership structure. Nihon Keizai Shimbun, Inc. is a private joint-stock company (kabushiki kaisha) headquartered in Otemachi, central Tokyo, with no listed shares and no external capital. Every share is held by current employees, former employees, retirees, and senior management — collectively numbering several thousand individuals, all internal to the institution.

Concretely, this means that no media conglomerate, no private-equity firm, no sovereign-wealth fund, and no foreign newspaper group has the legal capacity to acquire a stake in Nikkei. Share transfers are governed by internal rules that route ownership exclusively among the employee-shareholder community; departing employees and retirees retain their holdings or sell them back into the internal pool. The result is a closed capital structure that resembles a partnership at a large professional services firm more than a conventional listed media company.

That structure is the single most important fact about how Nikkei behaves. Without an external shareholder demanding quarterly margin expansion, the company has been able to absorb the cost of a large foreign bureau network, sustain a slow-burn international expansion that took more than a decade to break even, and — most consequentially — write a £844 million cheque for the Financial Times without consulting a single outside investor. It is also why Nikkei does not face the periodic activist-investor pressure or private-equity capitulation that has hollowed out so many comparable Western titles.

The Nikkei 225: an index almost everyone uses, owned by a company almost no one can buy

Beyond the newspapers, Nikkei’s most globally recognised asset is the index that bears its name. The Nikkei Stock Average — universally called the Nikkei 225 — is a price-weighted average of 225 large-cap stocks listed on the Tokyo Stock Exchange’s Prime Market segment. It has been calculated continuously since 1950, with the methodology and brand owned by Nikkei and day-to-day calculation run by Nikkei’s index-services subsidiary.

The economics of index ownership have grown materially as ETFs, structured products, and futures markets have proliferated around the headline number. Licensing is now a small but high-margin recurring revenue line, with users including the Osaka Exchange, Chicago Mercantile Exchange (dollar- and yen-denominated Nikkei 225 futures), Singapore Exchange, and asset managers running Nikkei-linked passive vehicles. The index also remains the price level cited in every Japanese newscast — a soft-power asset impossible to replace.

The ownership asymmetry is striking: the index the entire global asset-management industry references to talk about Japanese equities is the trademarked property of a Japanese company whose shares no asset manager can buy.

The Nikkei properties: a portfolio few foreign observers see in full

The Nikkei Shimbun is the flagship, but the group operates a wider portfolio that defines its commercial and editorial reach. The table below sketches the principal assets.

| Property | What it is | Reach / role |

|---|---|---|

| Nihon Keizai Shimbun (Nikkei Shimbun) | Flagship financial daily, print + digital (Nikkei Denshiban) | ~1.5M paid circulation; Japan’s financial newspaper of record |

| Nikkei Sangyo Shimbun | Industry-focused daily for manufacturing, tech, and corporate strategy desks | Specialist B2B readership inside Japanese industrials |

| Nikkei MJ (Marketing Journal) | Distribution, marketing, and consumer-trends paper, three times weekly | Retail, FMCG, advertising readership |

| Financial Times (acquired 2015) | UK-based global financial daily, FT.com, FT Weekend, How To Spend It | ~1.3M paying subscribers globally; ~$520M reported acquisition consideration to net cash |

| Nikkei Asia (formerly Nikkei Asian Review, 2013) | English-language weekly + digital covering Asian business and politics | Nikkei’s primary English vehicle for non-FT international readers |

| Nikkei America, Inc. | US-based affiliate publishing The Daily Economic and US-facing editorial | Small but strategically positioned New York operation |

| Nikkei BP | Business book, magazine, and digital media publisher (Nikkei Business, etc.) | Largest Japanese-language business publisher by output |

| TV Tokyo Holdings (~33% stake) | Listed broadcaster (9413.T) operating TV Tokyo and BS TV Tokyo | Business-oriented terrestrial broadcaster; WBS evening programme |

| Nikkei 225 index franchise | Index brand, methodology, licensing to futures and ETF markets | Globally referenced Japanese equity benchmark since 1950 |

The interesting feature of this portfolio is not its size but its shape: Nikkei is the only Japanese media group that owns a fully developed international flagship, runs its own English-language platform for Asia, holds a controlling-influence stake in a national broadcaster, and operates a leading business book publisher — all at once.

The Financial Times deal: why Nikkei paid $1.3 billion in 2015

The defining transaction of Nikkei’s modern history is the FT acquisition, announced 23 July 2015 and completed that November. Pearson, which had owned the FT since 1957, was repositioning around higher-education and assessment and had concluded that a global financial newspaper, however prestigious, no longer fitted the portfolio. A short and intense auction followed; Axel Springer of Germany was widely reported as the underbidder. Nikkei prevailed at approximately £844 million in cash, equivalent at the time to roughly $1.3 billion.

The strategic logic was unusually clear. The Japanese newspaper market was already shrinking on every demographic metric, and building an international platform organically had proved slow: Nikkei Asian Review, launched in 2013, was still establishing itself when the FT opportunity surfaced. The FT offered, in one transaction, a fully developed brand with global advertiser relationships, an established digital subscription operation, and a paying subscriber base in the high six figures and growing.

The price drew sceptical commentary at the time, with analysts arguing Nikkei had paid a strategic premium no purely financial buyer would have justified. The decade since has tilted the verdict in Nikkei’s favour: the FT has continued to grow its paying digital subscriber base, has reported operating profits in successive post-acquisition years, and now sits as one of the very few quality-news properties to have demonstrably built a sustainable subscription business at scale.

Editorial independence was the other test. Nikkei committed publicly to a non-interference posture, retaining the FT’s existing editorial leadership and London-based newsroom. A decade of subsequent FT coverage critical of Japanese corporate governance failures and of the Japanese government has provided the practical evidence that the commitment has held — the most important non-financial deliverable of the deal.

Nikkei Asia, Nikkei America, and the international subscription thesis

The FT acquisition sits alongside a quieter but equally important move: building Nikkei’s own English-language platforms targeted at non-Japanese readers. The principal vehicle is Nikkei Asia, launched in 2013 as Nikkei Asian Review and rebranded under the shorter name in 2020. Editorial sits primarily in Tokyo, with bureau presence across Bangkok, Singapore, Jakarta, Hong Kong, Taipei, Hanoi, Manila, and other Asian capitals. The product is positioned not as a translation of the Nikkei Shimbun but as a separate weekly and digital operation reporting on Asian business and political economy for an international readership.

Nikkei America, Inc. is a smaller US-based affiliate publishing English-language business and Japanese-community content from New York, including The Daily Economic. Its role is less about subscriber scale than about maintaining an editorial and commercial presence in the US business-news ecosystem.

Nikkei is the only Japanese media group to have built — and sustained — a multi-platform international subscription business. Other Japanese newspapers have attempted English sites and translated newsletters, but none has produced a paying international subscriber base of meaningful scale. Nikkei Asia plus the FT, taken together, give Nikkei a roster of paying non-Japanese subscribers no other Japanese media organisation comes close to matching.

The wider group: Nikkei BP, TV Tokyo, and the index franchise

Three further assets shape the wider group. Nikkei BP dominates Japanese-language business books, MBA-style management titles, and corporate biographies, alongside flagship magazines including Nikkei Business and Nikkei Computer — the print-and-digital reference shelf for the Japanese corporate manager.

TV Tokyo Holdings, in which Nikkei holds approximately a one-third stake, operates the TV Tokyo terrestrial network and BS TV Tokyo. TV Tokyo’s editorial identity has always been business-tilted — its flagship evening programme World Business Satellite (WBS) is one of the few prime-time television properties anywhere globally to lead with corporate and market news — and the symbiosis with the Nikkei Shimbun newsroom is unusually deep for a broadcaster-newspaper relationship.

The Nikkei 225 franchise is structurally different from the publishing and broadcasting businesses but commercially significant. Index licensing, futures-related revenue, and ETF-tied fee streams have grown into a stable recurring revenue line — small in absolute terms next to subscription and advertising, but high-margin and largely insulated from the cyclical pressures on traditional publishing.

Editorial independence under closed ownership: an unusual experiment

It is a counterintuitive feature of media economics that Nikkei’s closed, employee-owned structure has produced one of the more editorially robust newspaper groups in the developed world. No external shareholders means no quarterly pressure to chase clicks at the expense of editorial standards, no activist demanding cost cuts that would gut the bureau network, and no controlling family imposing personal politics on coverage. The internal-only share register also means senior editorial leadership cannot be removed by a hostile bidder.

The counter-risks are real but containable. Employee ownership can produce its own conservatism — reluctance to disrupt internal hierarchies and under-investment in technical platforms because the culture is print-first. Defenders argue, fairly, that the same closed structure that produces those weaknesses is what made it possible to absorb a thirteen-figure FT acquisition without flinching and to sustain a decade of patient international platform-building incompatible with a listed company’s quarterly cadence.

Leadership and the next decade

The current president, Tsuyoshi Hasebe, succeeded Hiroaki Yoshida, who in turn followed the long-serving Tsuneo Kita — the figure most identified with the FT acquisition. The Nikkei presidency is a substantively powerful role overseeing both editorial direction and group strategy, but it operates within an institutional culture that places enormous weight on consensus and on continuity across leadership transitions. Strategic shifts tend to be slow, deliberate, and irreversible once committed; the FT deal itself was the product of internal discussions stretching back years before Pearson formally put the paper up for sale.

The defining questions for the next decade are well understood inside the company. Can the FT continue to compound its paying digital subscriber base against the Wall Street Journal, New York Times, Bloomberg, and Reuters? Can Nikkei Asia move from a respected niche to a meaningful paying-subscriber business across Southeast Asia, India, and the wider Asian diaspora? Can the Japanese-language flagship convert another generation of digital readers as the print base inevitably declines? And can the closed employee-ownership structure continue to fund the patient capital required without producing creeping institutional inertia?

None has an obvious answer. The relevant point is that Nikkei is the only Japanese newspaper group for which these are interesting questions at all. The other major dailies — Yomiuri, Asahi, Mainichi, Sankei — face structural decline in their core market without a comparable international platform, index franchise, or acquired global asset. Nikkei is the outlier, and the FT deal is the reason.

FAQ

Who owns Nihon Keizai Shimbun, and can a foreign investor buy in?

Nihon Keizai Shimbun, Inc. is a private joint-stock company wholly owned by its current and former employees, retirees, and senior management — collectively numbering several thousand individual internal shareholders. There is no listed stock, no external capital, and no mechanism by which a foreign investor, a private-equity firm, or another media group can acquire shares. The structure has been in place for decades and is one of the defining features of how Nikkei behaves strategically and editorially.

How much did Nikkei pay for the Financial Times, and was the deal worth it?

Nikkei agreed in July 2015 to acquire the Financial Times from Pearson for approximately £844 million in cash — roughly $1.3 billion at prevailing exchange rates — making it the largest acquisition of a foreign media property by any Japanese newspaper. A decade on, the FT has continued to grow its paying digital subscriber base into seven figures and has reported operating profits in successive post-acquisition years. The price drew scepticism at the time but is now widely viewed as a strategically sound bet, particularly relative to comparable global newspaper deals that have not aged as well.

What exactly is the Nikkei 225, and how does Nikkei make money from it?

The Nikkei 225 is a price-weighted average of 225 large-cap stocks listed on the Tokyo Stock Exchange Prime Market, calculated continuously since 1950 with the methodology owned by Nikkei. Revenue from the franchise comes principally from index licensing to futures markets (Osaka Exchange, Chicago Mercantile Exchange, Singapore Exchange) and to asset managers running Nikkei 225-linked ETFs and structured products. It is a small but high-margin recurring revenue line, separate from the publishing and broadcasting operations.

How is Nikkei Asia different from the Financial Times?

The Financial Times is the global financial newspaper Nikkei acquired from Pearson in 2015, with editorial sitting in London and a worldwide subscriber base. Nikkei Asia is a separate English-language weekly and digital platform launched by Nikkei in 2013 (originally as Nikkei Asian Review, rebranded in 2020), with editorial sitting primarily in Tokyo and Asian bureau cities, focused specifically on business and political coverage of Asia for an international readership. The two operate as distinct editorial products under common ownership rather than as a single integrated newsroom.

What is Nikkei’s relationship with TV Tokyo?

Nikkei holds approximately a one-third stake in TV Tokyo Holdings, the listed parent of TV Tokyo and BS TV Tokyo. The broadcaster has an unusually business-tilted editorial identity for a terrestrial network — its evening business programme World Business Satellite (WBS) is one of the longest-running prime-time business shows globally — and there is a deep symbiosis with the Nikkei Shimbun newsroom on coverage and talent. The remaining shareholding is widely held by other Japanese institutions and public investors via the Tokyo Stock Exchange listing.

Working with Nikkei

Looking to advertise across Nikkei’s print and digital properties, license Nikkei 225 index data into a fund or structured product, syndicate Financial Times or Nikkei Asia content into a Japanese-market vehicle, or scope research partnerships with Nikkei BP and TV Tokyo’s business newsroom? Get in touch via Japonity’s business-matching service — we connect foreign media, financial institutions, and corporate counterparties with the right partners inside Japan’s most internationally positioned newspaper group.

Related from Japonity — Japan’s media & broadcasting

- The Asahi Shimbun Company — Japan’s #2 newspaper and the politicized media question

- The Yomiuri Shimbun — Japan’s #1 newspaper by circulation — the conservative-establishment paper

- Fuji Media Holdings — The 2025 governance reset activists forced on Japan’s Daiba broadcaster

- Nippon Television Holdings — Japan’s #1 commercial broadcaster + Studio Ghibli + Hulu Japan

Want to source Japanese products beyond these company profiles? Japonity also runs a Japan Sourcing Hub — a research-grade catalogue of 1,185 verified Japanese food products and 200+ overseas EC stores, ready for B2B procurement.

Interested in Japanese business opportunities?

Whether you're looking for technology partners, engineering talent, or market insights — we can help connect you with the right Japanese organizations.

Get in Touch →