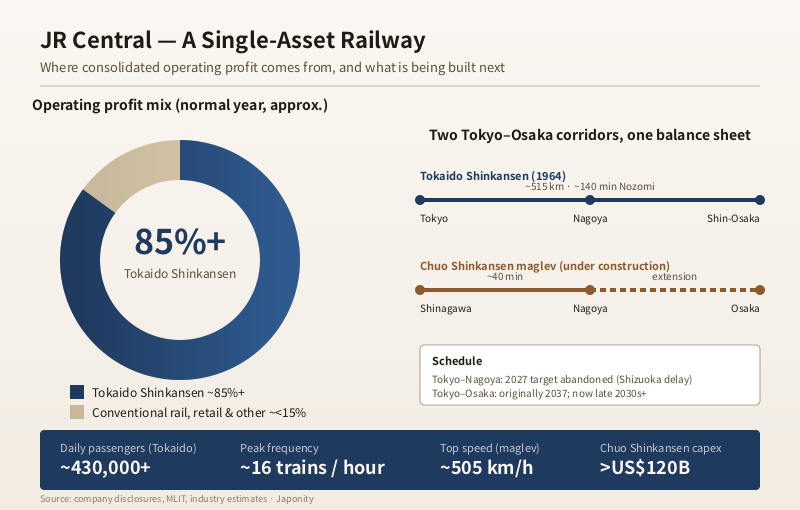

The Tokaido Shinkansen runs approximately 515 km between Tokyo and Shin-Osaka. It carries roughly 430,000 passengers a day, dispatches up to sixteen trains an hour at peak, and generates — depending on the year — somewhere between 85 percent and 95 percent of Central Japan Railway Company’s consolidated operating profit. JR Central (TSE: 9022) is, in the strictest financial sense, a single-asset company. That single asset happens to be the world’s first and most profitable high-speed rail corridor. It is now being doubled, at the company’s own expense, by an approximately ¥17 trillion (well over US$120 billion) superconducting maglev line called the Chuo Shinkansen, whose Tokyo-Nagoya segment was originally targeted for 2027 but has been pushed back indefinitely after Shizuoka Prefecture refused to permit tunnel works it argues will draw down flows in the Oi River. For foreign infrastructure investors, JR Central is not a diversified railway operator. It is a leveraged bet on one corridor, one technology, and one prefectural water-rights dispute.

One corridor, one company

Few large listed companies anywhere in the world derive as much of their economics from as little physical real estate as Central Japan Railway Company. The Tokaido Shinkansen, the line that JR Central inherited at the 1987 breakup of Japanese National Railways, runs broadly parallel to Japan’s old Tokaido highway and threads the Pacific-coast megalopolis that contains Tokyo, Yokohama, Nagoya, Kyoto, and Osaka. Roughly 60 percent of Japan’s gross domestic product is produced inside the catchment of stations served by this single line. The corridor is so dense, and the alternative — flying — so unattractive for distances of two hours or less, that JR Central has, in practice, an unregulated long-distance monopoly between the country’s two biggest economic regions.

That concentration is also the company’s central risk. JR East, headquartered in Tokyo, runs a sprawling commuter and regional network across the Kanto and Tohoku regions, plus the Tohoku, Joetsu, and Hokuriku shinkansen lines; its revenue mix is more retail-and-real-estate than pure rail. JR West, headquartered in Osaka, owns the western half of the Sanyo Shinkansen and a similarly diversified commuter footprint. JR Central, by contrast, runs a regional conventional-line business across Shizuoka, Aichi, Gifu, Mie, Nagano, and Yamanashi prefectures that is small, structurally loss-making in parts, and serves mainly as feeder traffic into Nagoya and the Shinkansen. The headquarters is in Nagoya, with a major secondary base in Tokyo near Shinagawa Station — itself the planned northern terminus of the maglev.

How the Tokaido Shinkansen became a cash machine

The line opened on 1 October 1964, nine days before the Tokyo Olympics, as the world’s first dedicated high-speed railway. Its commercial logic has barely changed in six decades. Distances are calibrated for trains rather than planes: Tokyo to Nagoya in roughly 100 minutes, Tokyo to Shin-Osaka in roughly 140 minutes on the fastest Nozomi services. Frequency is what makes the corridor structurally non-substitutable. At peak hour, JR Central runs trains at approximately three- to four-minute intervals, an operational rhythm closer to a metro than to intercity rail. Load factors on Nozomi services routinely exceed 70 percent.

The current rolling stock standard, the Series N700S, entered service in 2020. It is the seventh generation of train to run on the line, lighter and more energy-efficient than its predecessors, with batteries that let it self-rescue from a tunnel after an earthquake. Each train carries approximately 1,323 passengers in a fixed sixteen-car formation. JR Central does not vary capacity; it varies frequency. The trade-off is operational simplicity at near-airline punctuality, with average delays measured in seconds rather than minutes.

The financial result of this operating model is unusual for a railway anywhere in the world. JR Central’s consolidated operating margin in normal years sits in the high-twenties to low-thirties as a percentage of revenue, a level closer to a software business than to a transport company. Inside that figure, the Tokaido Shinkansen alone is materially more profitable; the regional and ancillary businesses are roughly break-even to slightly loss-making in aggregate. Stripped of accounting allocation, JR Central is the Tokaido Shinkansen with a small portfolio of orbiting businesses attached.

The Chuo Shinkansen maglev: a self-funded second corridor

The clearest signal of how JR Central views its own economics is the Chuo Shinkansen — a second Tokyo-Osaka line, this one based on superconducting magnetic levitation rather than wheel-on-rail technology. The project’s design speed is approximately 505 km/h, which would make it the fastest scheduled passenger train in the world. Tokyo Shinagawa to Nagoya is a 286 km route, of which roughly 90 percent runs in tunnel. Tokyo to Nagoya is meant to take approximately 40 minutes, less than half the Tokaido Shinkansen’s time. The Nagoya-Osaka extension would take the full journey to under 70 minutes.

What is most unusual is who is paying. The capital cost is now estimated at well over ¥7 trillion for Tokyo-Nagoya and a further ¥10 trillion or more for Nagoya-Osaka — together comfortably north of US$120 billion. JR Central is funding the project on its own balance sheet, supported by approximately ¥3 trillion in long-term loans from the Japan government-affiliated Japan Railway Construction, Transport and Technology Agency on relaxed terms but without taking on construction risk from the state. There is no farebox-revenue subsidy. The company is, in effect, mortgaging the cash flows of one Tokyo-Osaka corridor to build a second, faster one.

The Shizuoka problem

For most of the 2010s the Chuo Shinkansen’s official opening date was 2027 for Tokyo-Nagoya and 2037 for the full Tokyo-Osaka run. The 2027 target has now slipped indefinitely. The reason is not engineering. It is a roughly 9 km stretch of tunnel under the Southern Japanese Alps that crosses beneath the headwaters of the Oi River in Shizuoka Prefecture. The prefectural governor’s office argued, with backing from the prefecture’s tea-growing and water-utility constituencies, that excavation would drain the Oi River’s flow into the tunnel and impair downstream water supplies. JR Central has offered a series of engineering remedies — pumping water back up over the watershed, releasing it from reservoirs — but Shizuoka withheld permission to begin work on the local section for roughly seven years.

The dispute is now in a partial thaw following a change of prefectural governor in 2024, but the lost construction window cannot be made up. JR Central has stopped publicly committing to a Tokyo-Nagoya opening year and instead refers to the line opening “as soon as practicable” after Shizuoka tunneling resumes. Realistic industry estimates place a Tokyo-Nagoya opening in the very late 2020s or early 2030s, with the Osaka extension correspondingly delayed. For an asset whose net present value depends heavily on when revenue starts flowing, a five-year slip is material.

| Item | JR Central | JR East | JR West |

|---|---|---|---|

| Headquarters | Nagoya | Tokyo | Osaka |

| TSE code | 9022 | 9020 | 9021 |

| Flagship Shinkansen | Tokaido | Tohoku / Joetsu / Hokuriku | Sanyo |

| Network length (approx.) | ~1,970 km | ~7,400 km | ~4,900 km |

| Shinkansen share of profit | ~85%+ | moderate | moderate-high |

| Major non-rail business | limited | retail / real estate / Suica | retail / real estate / Icoca |

| Signature future project | Chuo Shinkansen maglev | Tohoku extension & commuter density | Hokuriku extension to Osaka |

What sits on top of the line

JR Central’s non-Shinkansen businesses fall into three rough buckets. The first is its conventional rail network, dominated by the Tokaido Main Line and the Chuo Main Line running into Nagoya, plus smaller lines such as the Takayama, Kisei, and Iida lines that thread Gifu, Mie, and Nagano. This network is unglamorous, structurally pressured by depopulation in the regional service areas it covers, and largely a feeder system. The second is station-related real estate and retail, anchored by JR Central Towers and JR Gate Tower above Nagoya Station, which form one of Japan’s largest integrated station complexes. The third is a smaller portfolio of hotels under the Associa brand, a travel agency business, and the company’s contract-manufacturing operations for rolling stock and railway equipment, sold to other operators and historically pitched to overseas buyers.

Overseas, JR Central’s most visible export attempt was Texas Central Railway, an effort over the 2010s and early 2020s to license the Tokaido Shinkansen system to a privately developed Dallas-Houston high-speed line in the United States. The project ran into land-acquisition fights along the Texas right-of-way and a fundamental U.S. financing model that JR Central could not, by itself, fix. By the mid-2020s the project was effectively shelved, and JR Central has substantially written down its exposure. The episode is instructive: the company’s operating excellence does not travel easily into jurisdictions without Japan’s planning, eminent-domain, and land-use frameworks.

The balance sheet behind the bet

JR Central runs a heavier balance sheet than its size would otherwise suggest, because the Chuo Shinkansen sits on it. Interest-bearing debt has risen materially through the 2010s and 2020s as maglev construction expenditure accelerated and revenue from the new line remained at zero. The company’s free cash flow from the Tokaido Shinkansen is, in effect, the collateral; if Tokaido Shinkansen passenger volumes were to fall sharply and persistently — through a major Nankai Trough earthquake disrupting the line, a permanent shift in Japan’s intercity travel patterns, or a successful aviation competitor — the maglev’s funding model would come under stress. This is the central single-asset risk that foreign investors price.

The counter-argument, and the reason JR Central trades as a quality compounder rather than as an infrastructure project equity, is that the Tokaido Shinkansen has a track record of resilience that few transport assets anywhere can match. Volumes recovered sharply after the 2011 Tohoku earthquake; they recovered again, more slowly, after the COVID-19 trough of 2020-2021. Through six decades of operations there has been no passenger fatality from train accidents. The line is overhauled and re-railed continuously without interrupting service. The company has, in industrial terms, a remarkably narrow but remarkably deep moat.

Leadership and governance

Yoji Kaneko serves as president and representative director, having taken the role in the early 2020s after a long career inside the company; the chairmanship has historically rotated through executives steeped in the line’s operating culture. JR Central’s board and senior management remain heavily engineer-led, with a noticeably lower proportion of outside finance hires than at JR East. Governance is conventional by Tokyo Stock Exchange standards, with a board including outside directors and audit committee structure. The company has historically preferred to fund growth from its own cash flow and modest leverage rather than from equity raises, which has kept the float relatively stable.

Why foreign investors should treat JR Central as a single-asset bet

The investor framing for JR Central is straightforward, and unusual. The equity is not a diversified Japanese transport operator. It is the present value of cash flows from the Tokaido Shinkansen, plus a long-dated, capex-heavy real option on the Chuo Shinkansen maglev, minus the risks of one prefectural water-rights dispute, one fault-line earthquake scenario, and one project execution timeline. The retail and station businesses round out the picture but do not change the centre of mass. For infrastructure investors who normally diversify across geographies, modes, and assets, owning JR Central is closer to owning a toll-road concession than a transport conglomerate. That clarity is both the bull case and the bear case.

FAQ

How much of JR Central’s profit comes from the Tokaido Shinkansen?

In a normal operating year, roughly 85 percent or more of JR Central’s consolidated operating profit is generated by the Tokaido Shinkansen alone. The proportion has fluctuated with the pandemic and recovery, but the line’s structural dominance of group economics is the central fact about the company.

When will the Chuo Shinkansen maglev open?

The original target was 2027 for Tokyo Shinagawa to Nagoya and 2037 for the full Tokyo-Osaka route. The 2027 target has been formally abandoned because Shizuoka Prefecture withheld permission to begin local tunnel construction for approximately seven years. JR Central now refers to the line opening “as soon as practicable” once construction resumes; industry observers expect the late 2020s to early 2030s for Tokyo-Nagoya, with the Osaka extension correspondingly later.

Why did Shizuoka Prefecture block construction?

The maglev’s planned route crosses under the Southern Japanese Alps near the headwaters of the Oi River, which supplies water for downstream agriculture and municipal use in Shizuoka. The prefecture argued that tunneling would draw water into the bore and reduce surface flows. JR Central has proposed mitigation including pumping water back over the watershed, and dialogue improved after a change of prefectural governor in 2024.

How does JR Central compare with JR East and JR West?

JR East is larger by revenue and has a much bigger commuter and retail business; JR West is intermediate and runs the Sanyo Shinkansen plus the Kansai commuter network. JR Central is smaller, more profit-dense, and far more concentrated in a single high-speed corridor. For investors, JR East is closer to a diversified transport-and-real-estate platform; JR Central is closer to a single high-speed asset.

What happened to Texas Central Railway?

Texas Central was the most ambitious overseas export of the Tokaido Shinkansen system, aimed at building a Dallas-Houston high-speed line in the United States. It ran into land-acquisition disputes and a financing model that did not match U.S. private-infrastructure norms, and the project was effectively shelved by the mid-2020s. The episode has tempered JR Central’s appetite for direct overseas system exports.

Working with JR Central

For foreign infrastructure investors, suppliers, and corporate partners interested in JR Central, the Tokaido Shinkansen ecosystem, or Japan’s high-speed rail and maglev supply chain, Japonity supports introductions via our business matching service. Areas of partner interest include rolling-stock components, tunneling and civil engineering for the Chuo Shinkansen, station-area real estate around Nagoya and Shinagawa, and travel and hospitality offerings designed for inbound visitors using the Tokaido corridor.

Related from Japonity — Japan’s passenger railways & rail conglomerates

- JR East — The world’s largest railway by passengers — and Japan’s biggest station-retail empire

- Tokyu Corporation — The Shibuya-redeveloping rail conglomerate

- Hankyu Hanshin Holdings — Kansai’s railway-real-estate-entertainment empire

- Seibu Holdings — Tokyo’s western-suburb rail empire + Prince Hotels + Lions

- Kintetsu Group Holdings — Japan’s longest private railway — Osaka-Nara-Ise-Nagoya

Want to source Japanese products beyond these company profiles? Japonity also runs a Japan Sourcing Hub — a research-grade catalogue of 1,185 verified Japanese food products and 200+ overseas EC stores, ready for B2B procurement.

Interested in Japanese business opportunities?

Whether you're looking for technology partners, engineering talent, or market insights — we can help connect you with the right Japanese organizations.

Get in Touch →