When the Hanshin Tigers clinched the 2023 Japan Series, breaking decades of near-misses against the Tokyo-based Yomiuri Giants, the celebration was not merely about baseball. It was a corporate moment for Hankyu Hanshin Holdings (TSE: 9042) — the Osaka-headquartered conglomerate that owns the Tigers, the all-female Takarazuka Revue theatre, the Umeda Hankyu Department Store (Japan’s single-largest department store by annual sales, at approximately JPY 250 billion), and roughly 150 kilometres of private railway across the Kansai region. Formed in October 2006 when Hankyu Holdings acquired roughly half of Hanshin Electric Railway — a defensive merger triggered by the Murakami Fund’s 2005 hostile stake-build — Hankyu Hanshin today operates the most complete embodiment of a uniquely Japanese invention: the integrated rail-and-everything-else conglomerate.

The Kobayashi model: a Japanese invention that travelled the world

To understand Hankyu Hanshin, one must understand Ichizo Kobayashi (1873–1957), arguably the most consequential business architect modern Japan produced outside of the zaibatsu founders. In 1907, Kobayashi founded the Minoo Arima Electric Railway — the company that would become Hankyu — and over the following two decades he assembled a playbook that would be copied by every major private railway in Japan and, eventually, by transit-oriented developers from Hong Kong to Houston.

The Kobayashi model worked on a simple but radical premise: a railway company should not merely sell tickets. It should buy farmland at the terminals, build housing for the new middle class, anchor each end of the line with destinations that generate two-way traffic — a department store at the urban terminus (Umeda), a leisure attraction at the suburban terminus (Takarazuka hot springs, then the Revue, then the baseball stadium at Koshien on the Hanshin line). Each business reinforced the others. The trains carried customers to the stores; the stores funded the trains; the entertainment drew weekend riders into off-peak capacity.

A century later, MTR in Hong Kong, Mitsui Fudosan, Tokyu, Seibu and Odakyu all run variations of the Kobayashi playbook. None, however, runs it with quite the cultural weight that Hankyu Hanshin still carries in Kansai — where the Tigers, the Revue and the Umeda terminal are not merely subsidiaries on an org chart but pillars of regional identity.

1899 and 1907: two railways, two cultures

Hanshin Electric Railway, founded in 1899, was the older of the two. It ran along the coast between Osaka and Kobe, hugging the industrial belt and serving working-class neighbourhoods. Hankyu, founded in 1907 and incorporated under its present railway charter shortly after, ran inland through the elevated middle-class suburbs Kobayashi himself helped to plan. The cultural distinction persisted for the entire twentieth century — Hanshin was the railway of factory workers and the Tigers, Hankyu the railway of department-store shoppers and the Takarazuka stage.

For nearly a hundred years the two competed bitterly for the Osaka-Kobe corridor. They ran parallel tracks, parallel department stores in Umeda, parallel real estate operations. By the early 2000s both had matured into solid but unspectacular regional operators, with Hanshin in particular suffering from a depressed share price relative to its Koshien Stadium real estate and Tigers brand value.

The Murakami Fund and the 2006 merger

In September 2005, Yoshiaki Murakami’s activist fund — the most aggressive value investor Japan had yet seen — disclosed a stake of approximately 27% in Hanshin Electric Railway. Murakami’s thesis was straightforward: Hanshin’s hidden assets, particularly its Tigers stake and its Koshien-adjacent landholdings, were worth far more than the stock market recognised. He pressed for a Tigers IPO and asset disposals.

The Hanshin board, alarmed at the prospect of the Tigers and Koshien being unbundled from the railway, sought a friendly counterparty. Hankyu Holdings — culturally adjacent, geographically overlapping, financially stronger — was the natural choice. In June 2006 Hankyu launched a tender offer for Hanshin shares; by October 2006 it had secured roughly 50% and the two companies merged to form Hankyu Hanshin Holdings, listed on the Tokyo Stock Exchange under code 9042. Murakami was subsequently arrested on unrelated insider-trading charges in 2006, ending the activist chapter — but the merger he involuntarily triggered fundamentally reshaped the Kansai corporate landscape.

The structural logic of the merger went beyond defence. The combined entity could rationalise overlapping operations in Umeda, where both companies owned prime terminal real estate adjacent to Osaka Station; it could combine purchasing across two department-store chains; and it could anchor a unified Kansai entertainment portfolio that no other regional player could match.

The seven-segment empire today

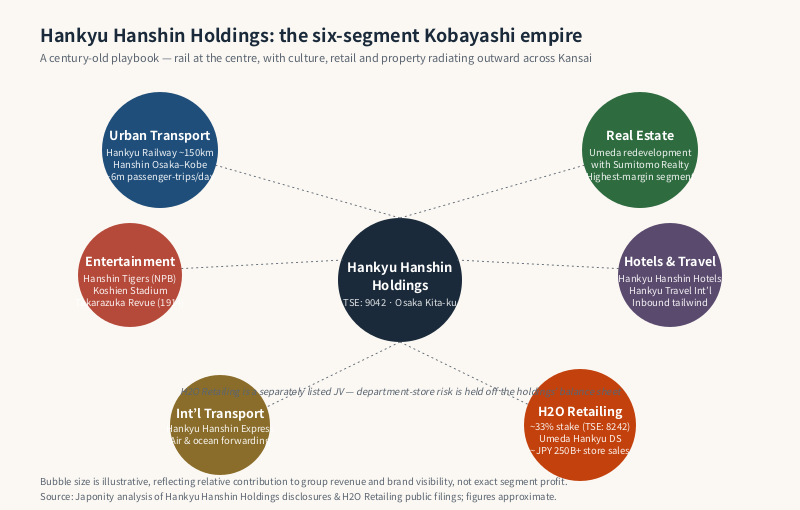

Hankyu Hanshin Holdings now organises itself into seven reporting segments. Together they generate consolidated revenue in the range of JPY 950 billion to JPY 1 trillion annually, with Urban Transportation and Real Estate providing the stable cash flows and Entertainment providing the brand halo.

| Segment | Core businesses | Profile |

|---|---|---|

| Urban Transportation | Hankyu Railway (~150 km), Hanshin Railway (Osaka–Kobe), Hokushin Kyuko, bus operations | Stable cash flow; ~6 million passenger-trips per day pre-pandemic; backbone of the group |

| Real Estate | Hankyu Hanshin Properties; Umeda redevelopment (with Sumitomo Realty); residential, office, leasing | Highest-margin segment; concentrated in Osaka Kita-ku terminal estate |

| Entertainment | Hanshin Tigers (NPB), Koshien Stadium, Takarazuka Revue, Umeda Arts Theater | Cultural anchor; modest direct margin but enormous brand and traffic-generation value |

| International Transportation | Hankyu Hanshin Express (forwarding), air & ocean cargo, logistics | Global B2B segment; counter-cyclical to domestic rail |

| Travel | Hankyu Travel International; inbound and outbound tourism | Heavily exposed to inbound recovery; benefiting from weak yen tailwinds |

| Hotels | Hankyu Hanshin Hotels — Osaka, Kobe, Tokyo, Kyoto properties | Mid-to-upscale urban hotel chain; rebounding strongly post-pandemic |

| Information & Media | Cable TV, advertising, publishing, digital services | Smaller scale; supports cross-promotion across other segments |

Notably absent from the segment table is one of the group’s most visible assets: the department stores. That is because Hankyu Department Store and Hanshin Department Store are operated through H2O Retailing (TSE: 8242), a separately listed entity in which Hankyu Hanshin Holdings retains a roughly 33% stake. The H2O JV partition, executed alongside the 2006 merger, allowed the retail business to consolidate independently — including the eventual acquisition of Izumiya and Kintetsu Department Store equity — while keeping department-store risk off the holdings’ balance sheet.

The Umeda terminal: the most valuable square kilometre in Kansai

Walk out of Osaka Station on the Kita (“north”) side and almost every building visible is, directly or indirectly, a Hankyu Hanshin asset. The Umeda Hankyu Department Store, fully rebuilt and reopened in 2012 after a decade-long redevelopment, occupies roughly 84,000 square metres of retail floor space — and consistently ranks as the single-highest-grossing department store in Japan, with annual sales of approximately JPY 250 billion (and in recent post-pandemic periods, reportedly above JPY 290 billion). For context, that is roughly twice the revenue of Isetan Shinjuku, the long-time Tokyo benchmark.

Adjacent to the department store sit the Umeda Hankyu Building, the Hankyu Sanbangai retail complex, Umeda Arts Theater, and the Grand Front Osaka mixed-use towers, co-developed with Sumitomo Realty and other partners. To the west, the former Umeda freight yard — Osaka’s “last big land” — is being redeveloped under the Umekita Phase 2 plan, with Hankyu Hanshin again playing a central role. By the late 2020s, Hankyu Hanshin will have shaped the skyline of Osaka’s most valuable district for more than a century.

For investors, the implication is structural: Hankyu Hanshin is not merely a railway company that happens to own real estate. It is one of Japan’s largest urban landlords whose holdings are concentrated in arguably the highest-growth metropolitan submarket of the country outside of central Tokyo.

The Tigers, the Revue and the limits of cultural valuation

No analyst can value the Hanshin Tigers fairly. The team, founded in 1935, has the most passionate fan base in Nippon Professional Baseball — a fan base that fills the 47,000-seat Koshien Stadium night after night, that buys Tigers-branded everything, that effectively treats the team as a public good of the Kansai region. The 2023 Japan Series victory, the team’s first in 38 years, was front-page news for a week.

From a reporting standpoint, the Tigers and Koshien generate modest revenue (a few tens of billions of yen annually in ticket, broadcast and merchandise income) and modest direct margin. But the indirect value — to the Hanshin railway line’s ridership, to Hankyu Hanshin’s recruitment, to the group’s bargaining position with retailers, sponsors and politicians — is enormous. The same logic applies to the Takarazuka Revue, founded by Kobayashi himself in 1914. The all-female musical theatre troupe is an institution of Japanese popular culture, with its own Grand Theater in Takarazuka (a town the railway literally built), its own academy, and a fan base that spans generations.

Peer comparison: how Hankyu Hanshin sits among Japan’s major private railways

| Group | Core region | Distinctive assets | Strategic posture |

|---|---|---|---|

| Hankyu Hanshin Holdings (9042) | Kansai (Osaka–Kobe–Kyoto) | Tigers, Takarazuka, Umeda Hankyu, H2O JV | Asset-heavy; cultural and terminal-real-estate concentration |

| Tokyu Corporation (9005) | Tokyo southwest (Shibuya) | Shibuya redevelopment, Tokyu Department Store, Tokyu Hotels | Asset-heavy; Tokyo urban-renewal pure play |

| Seibu Holdings (9024) | Tokyo northwest (Ikebukuro) | Lions baseball, Prince Hotels, Karuizawa resort estate | Asset-heavy but slimmed post-restructuring |

| Kintetsu Group Holdings (9041) | Kansai (Nara–Ise) | Largest private rail network by km; Buffaloes baseball history; Abeno Harukas | Distance-network heavy; tourism-led |

| Odakyu Electric Railway (9007) | Tokyo west (Shinjuku–Hakone) | Hakone tourism cluster; Odakyu Department Store | Tourism + commuter balance |

Among these, Hankyu Hanshin stands out for the breadth of its entertainment portfolio (no other private railway owns both a top-tier baseball team and a flagship musical theatre), and for the concentration of its real estate in a single ultra-prime submarket (Umeda).

Why this matters now: inbound tourism, weak yen, Osaka 2025

Two macro tailwinds make Hankyu Hanshin a strategically interesting story in 2026. First, the persistent weakness of the yen has driven inbound tourism to Japan well past pre-pandemic levels, with Osaka — gateway to Kyoto, Kobe and Nara — capturing a disproportionate share. Hankyu Hanshin’s travel, hotel, rail and retail segments all benefit. Second, Expo 2025 Osaka has accelerated public and private investment in the Kansai region’s transport and tourism infrastructure, with knock-on effects visible in Umeda redevelopment, hotel pipeline and convention demand.

For overseas businesses, the implication is concrete. A Western consumer brand seeking flagship retail presence in Kansai will sooner or later negotiate with the Umeda Hankyu Department Store buying team. A logistics operator entering the Japanese forwarding market will encounter Hankyu Hanshin Express. A hospitality group seeking development sites in Osaka will at some point share a table with Hankyu Hanshin Properties. The conglomerate is, for Kansai, the table at which many deals are eventually closed.

Governance and the next chapter

Hankyu Hanshin Holdings is led by a chairman and a president drawn from the legacy Hankyu side of the house, in line with the original 2006 merger arrangement under which Hankyu was the senior partner. The board has been progressively professionalised since the merger, with independent directors and clearer separation of supervisory and executive roles than in many comparable Japanese groups. The dividend policy is conservative, reflecting the capital-intensive nature of railway and urban-development operations.

The strategic questions facing the group through the late 2020s are familiar to any asset-heavy conglomerate: how aggressively to redevelop the remaining Umeda landbank; how to monetise the H2O Retailing relationship as Japan’s department-store sector continues to consolidate; how to scale international transport in a fragmented global forwarding market; and how to manage the Tigers and Takarazuka as cultural institutions in an era of shifting entertainment consumption. None of these is a near-term existential question. All of them shape what the next twenty years of the Kobayashi model will look like.

FAQ

Q1. Does Hankyu Hanshin own the Hanshin Tigers outright?

Yes. The Hanshin Tigers baseball team is a wholly-owned subsidiary of Hanshin Electric Railway, which is itself part of Hankyu Hanshin Holdings. The Tigers and Koshien Stadium are operated as part of the group’s Entertainment segment.

Q2. What is the Takarazuka Revue and why does a railway company own it?

The Takarazuka Revue is an all-female musical theatre troupe founded in 1914 by Hankyu founder Ichizo Kobayashi. It was originally created as a destination attraction at the end of the Hankyu line, drawing weekend ridership; over a century it became one of Japan’s most distinctive cultural institutions. Today it operates the Takarazuka Grand Theater and Tokyo Takarazuka Theater, with its own academy and a multi-generational fan base.

Q3. Why is the department-store business in a separate company (H2O Retailing) rather than inside Hankyu Hanshin Holdings?

At the time of the 2006 Hankyu-Hanshin merger, the two groups’ department stores were spun into a jointly held entity — H2O Retailing — to allow the retail business to consolidate and pursue M&A (including Izumiya and Kintetsu Department Store equity) independently of the parent. Hankyu Hanshin Holdings retains a strategic stake of approximately one-third.

Q4. How does Hankyu Hanshin compare to Tokyu in Tokyo?

Both are asset-heavy private-railway-and-real-estate conglomerates running variations of the Kobayashi model. Tokyu is the dominant operator in southwest Tokyo around Shibuya, where it is the lead developer of one of Asia’s most ambitious urban-renewal programmes. Hankyu Hanshin is the equivalent operator in Osaka–Kobe, with the added cultural assets of the Tigers and the Takarazuka Revue, which Tokyu does not have direct analogues for.

Q5. How can a non-Japanese company approach Hankyu Hanshin for a partnership?

Each segment has its own commercial team — retail buying for the department stores (via H2O Retailing), leasing for the real-estate portfolio, freight for international transport, and inbound tourism partnerships through the travel and hotels businesses. Japonity can help overseas companies map the relevant counterparty within the group and structure an introduction.

Working with Hankyu Hanshin

Hankyu Hanshin Holdings is one of the most important commercial counterparties in western Japan. Brands seeking Kansai retail presence, hospitality and tourism operators expanding into Osaka, logistics partners assessing the Japanese forwarding market, and real-estate developers evaluating Umeda-area sites all eventually have reason to engage with the group.

If you are exploring a partnership, retail buying conversation, real estate negotiation, or inbound-tourism collaboration with any part of the Hankyu Hanshin group, Japonity can help you map the right entity, prepare a Japanese-language briefing, and structure a first meeting. Start at /business-matching/.

Related from Japonity — Japan’s passenger railways & rail conglomerates

- JR East — The world’s largest railway by passengers — and Japan’s biggest station-retail empire

- JR Central — The Tokaido Shinkansen monopoly and the maglev moonshot

- Tokyu Corporation — The Shibuya-redeveloping rail conglomerate

- Seibu Holdings — Tokyo’s western-suburb rail empire + Prince Hotels + Lions

- Kintetsu Group Holdings — Japan’s longest private railway — Osaka-Nara-Ise-Nagoya

Want to source Japanese products beyond these company profiles? Japonity also runs a Japan Sourcing Hub — a research-grade catalogue of 1,185 verified Japanese food products and 200+ overseas EC stores, ready for B2B procurement.

Interested in Japanese business opportunities?

Whether you're looking for technology partners, engineering talent, or market insights — we can help connect you with the right Japanese organizations.

Get in Touch →