East Japan Railway Company — JR East, ticker 9020 on the Tokyo Stock Exchange — is the largest railway operator on the planet by passenger volume, carrying approximately seventeen million people each day across roughly seven thousand four hundred kilometres of track that stretch from the Yamanote Line ring inside central Tokyo to the Shinkansen platforms in Aomori, Niigata, and (via the Hokuriku corridor) Kanazawa and Tsuruga. Yet describing JR East as a railway is, at this point, an analytical category error. The company also operates Tokyo Station and Shinjuku Station — two of the busiest railway stations in the world — and through them controls a real-estate and retail empire that includes the Lumine fashion mall chain, the Atre family of station shopping centres, the ecute upscale food-hall network, and a substantial residential and office portfolio. Suica, the contactless IC card introduced in 2001 and now extended into mobile wallets, gives JR East a payments rail that runs in parallel to the steel ones. For an investor or partner trying to understand modern Japan, JR East is one of the most consequential and most under-appreciated companies in the country.

How a national railway became seven private companies

JR East was created on 1 April 1987 as part of the largest privatisation in Japanese postwar history — the breakup of Japanese National Railways (JNR), which by the mid-1980s had accumulated debts in excess of twenty-five trillion yen and a labour-relations situation that had become politically untenable. The Nakasone administration split JNR into six regional passenger railway companies plus JR Freight for nationwide rail cargo. Each took on the rolling stock, track, and stations within its geography; legacy debt was parked in a separate settlement entity and worked down over subsequent decades.

JR East inherited the densest and most lucrative slice of that map: the entire Kanto region — Tokyo, Saitama, Chiba, Kanagawa, Gunma, Tochigi, Ibaraki — together with Tohoku to the north, Niigata to the west, and parts of Yamanashi and Nagano. That meant the Yamanote Line, one of the most heavily trafficked rail corridors on earth, plus the trunk lines radiating out from Tokyo Station, plus three Shinkansen lines. The company listed on the Tokyo Stock Exchange in October 1993, the state progressively divested its remaining stake, and by 2002 JR East was a fully privately owned company with no government shareholding.

The headquarters sit in Yoyogi, Shibuya ward, next to the Shinjuku station complex. Wakui Mineyuki has served as president and CEO since 2024, succeeding Yuji Fukasawa; the group employs approximately thirty-eight thousand people across rail, retail, real-estate, and IT subsidiaries.

What the network actually looks like

The railway runs across two distinct tiers. The Shinkansen network is JR East’s high-speed franchise: the Tohoku Shinkansen from Tokyo to Shin-Aomori, opened in stages from 1982 and reaching its current northern terminus in 2010; the Joetsu Shinkansen from Tokyo to Niigata, opened in 1982; the Hokuriku Shinkansen from Tokyo to Nagano (1997), extended to Kanazawa in 2015 and to Tsuruga in March 2024 in a transfer that gradually hands operating control westward to JR West; plus the Yamagata and Akita mini-Shinkansen branches that share track with the Tohoku trunk.

The conventional network is the part most foreign analysts miss. The Yamanote Line carries roughly three to four million passengers a day on a single twenty-nine-station loop. The Chuo, Sobu, Keihin-Tohoku, Saikyo, Joban, Yokosuka, and Shonan-Shinjuku lines move the Greater Tokyo workforce in and out of the central business districts. Outside the Kanto core, conventional lines reach across Tohoku to Sendai and the Pacific coast rebuilt after the 2011 earthquake and tsunami, along the Sea of Japan through Niigata and Akita, and into the resort areas of Nagano and Yamanashi. The route map is the densest network outside central Europe operated by a single company.

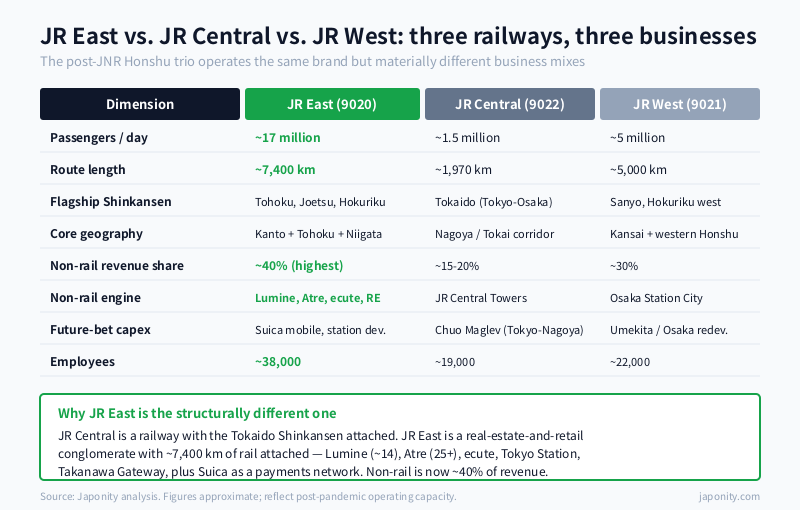

Three JRs, three different businesses

Although the JR group looks like one brand to the casual user, the three Honshu passenger companies — JR East, JR Central, JR West — run materially different businesses. The table below sketches the comparison.

| Dimension | JR East (9020) | JR Central (9022) | JR West (9021) |

|---|---|---|---|

| Passengers per day (approx.) | ~17 million | ~1.5 million | ~5 million |

| Route length (approx.) | ~7,400 km | ~1,970 km | ~5,000 km |

| Flagship Shinkansen | Tohoku, Joetsu, Hokuriku | Tokaido (Tokyo-Shin-Osaka) | Sanyo, Hokuriku (Kanazawa west) |

| Geography | Kanto + Tohoku + Niigata | Nagoya / Tokai corridor | Kansai + western Honshu |

| Revenue mix (railway share) | ~60% railway / 40% non-rail | ~80%+ railway | ~70% railway |

| Non-rail engine | Lumine, Atre, ecute, real estate | JR Central Towers, hotels | Osaka Station City, hotels |

| Future-bet capex | Suica mobile / station retail | Chuo Maglev (Tokyo-Nagoya) | Umekita / Osaka redevelopment |

| Employees (approx.) | ~38,000 | ~19,000 | ~22,000 |

The single most important difference is the revenue mix. JR Central is a railway company with retail attached — its Tokaido Shinkansen between Tokyo and Osaka is so profitable that diversification has always been a side project, and its capital is now overwhelmingly committed to the Chuo Shinkansen maglev project. JR East, by contrast, has spent thirty years deliberately building out non-rail revenue, and that revenue is now closer to forty percent of the total. The economics that follow from that shift — lower cyclicality, higher land-value capture, more consumer touchpoints — make JR East a genuinely different equity story.

The station as platform: Lumine, Atre, and ecute

JR East’s retail strategy starts from a deceptively simple observation. The company already owns the most valuable retail real estate in Japan — the floors directly above and adjacent to every major commuter station in Kanto — and it already has the highest-frequency consumer audience of any business in the country. The strategic question was whether that audience could be monetised by JR East itself rather than rented out at flat per-square-metre rates to third-party department stores. Beginning in the late 1990s and accelerating through the 2000s and 2010s, the answer was emphatically yes.

Lumine is the most visible of the chains. A fashion-led shopping mall format aimed primarily at women in their twenties and thirties, Lumine operates approximately fourteen stores at the largest JR East stations — Shinjuku (the flagship, in three connected buildings), Ikebukuro, Yurakucho, Yokohama, Omiya, Kita-Senju, Tachikawa, Machida, Ogikubo, Fujisawa, and others — together with a Lumine est. format and the EST and NEWoMan upscale variants near Shinjuku. Each store curates several hundred brand tenants under JR East’s commercial direction, with revenue captured through a combination of rent, percentage-of-sales fees, and selected directly operated concepts.

Atre is the broader station-shopping format, operating at twenty-five or more stations from Ueno and Shinagawa in central Tokyo out to Kichijoji, Ebisu, Kameido, Akihabara, and the suburban commuter belt. Where Lumine is fashion-led and aimed at a specific demographic, Atre is broader: food, cosmetics, daily-life retail, restaurants, and services aligned to commuter patterns. Ecute is the higher-end food-and-gift format that occupies the inside of the station gates at locations like Shinagawa, Tokyo, Ueno, Omiya, and Tachikawa — designed for the impulse purchase of premium take-home dinners, sake, sweets, and bento boxes by passengers crossing platforms on their way home from work. Together with the larger station building developments — Granduo, Lumine the Yoshimoto, the Tokyo Station Marunouchi complex — these formats produce the retail revenue that lifts JR East’s non-rail share to its current level.

Real estate: the part that nobody pays attention to

Below the station retail sits a substantial pure-play real-estate business. JR East owns the air rights above many of its commuter and Shinkansen stations and has progressively redeveloped them as office towers, hotels, and residential complexes. The Tokyo Station Marunouchi reconstruction — restoring the 1914 station building alongside the JP Tower and the GranTokyo towers — is the highest-profile example, but the same playbook has been applied at Shinjuku, Shinagawa, Shibuya, Yokohama, Omiya, and Sendai. The Takanawa Gateway station, opened in 2020 between Shinagawa and Tamachi, anchors a thirteen-hectare redevelopment of former rail yards into one of the largest single projects in central Tokyo.

The economics of these projects are unusual. JR East already owns the land and the air rights; the marginal capital is for the building itself rather than for site acquisition. The retail and office tenants are anchored by the station’s own foot traffic. The hotels — including JR East’s own Metropolitan and Hotel Mets chains — sell rooms partly on the basis of direct station access. And the residential developments capture the long-term land-value appreciation that runs through the Tokyo commuter network as a whole. For a railway company, real estate at this scale is not a side business. It is a structural complement to the rail asset.

Suica: the IC card that became a payments network

In November 2001, JR East launched Suica — Super Urban Intelligent Card — as a contactless IC card replacing the magnetic-strip stored-value commuter passes that had been the standard for decades. The card used the FeliCa contactless chip developed by Sony, allowed tap-to-pay travel through ticket gates, and within a few years had become near-universal across the Kanto commuter network. Mutual interoperability agreements with the IC cards of the other JR companies, the major private railways, and the bus operators followed; by the late 2000s a single Suica card worked on essentially any public transport in Japan.

The strategically important step came when Suica was extended beyond transit. Convenience-store chains accepted Suica payments. Vending machines accepted Suica payments. By the mid-2010s, Suica functioned as a small-ticket electronic-money network with hundreds of thousands of merchants nationwide. Mobile Suica integration — first through Osaifu-Keitai feature phones, then through Apple Pay from 2016 and Google Wallet subsequently — moved the card into the smartphone, with top-ups happening through credit cards rather than cash at machines. JR East publishes Suica issuance and transaction figures that put it among the largest electronic-money networks in Japan by transaction count.

What makes Suica strategically interesting is that the network sits inside JR East rather than in a separate payments subsidiary spun off long ago. The company controls the standard, sets the merchant fee, owns the consumer relationship, and has integrated Suica into its loyalty program, mobile app, and station retail. For an infrastructure investor, this is closer to owning a payments network than to owning a transit pass.

The pandemic, and what came after

COVID-19 hit Japanese commuter railways harder than most foreign observers expected. Daily ridership on the Yamanote Line and trunk commuter lines dropped by between thirty and forty percent at the trough, as Tokyo employers shifted to remote and hybrid work arrangements. Shinkansen ridership dropped further, particularly on the business-traveller-heavy Tokyo-Sendai and Tokyo-Niigata routes. JR East posted its first full-year loss as a listed company in fiscal 2020 — approximately five hundred and eighty billion yen — and a second consecutive loss in fiscal 2021. The non-rail businesses, particularly station retail through the periods of soft commercial activity, took proportional damage.

The recovery has been steady but not symmetric. By fiscal 2024 ridership on the conventional network had returned to roughly ninety percent of pre-pandemic levels, with the missing ten percent attributable to durable hybrid-work adoption rather than to lingering caution. Shinkansen ridership has recovered more fully, supported partly by domestic leisure travel and very materially by the inbound-tourism boom. Inbound visitors to Japan exceeded thirty-five million in 2024, a record, and JR East has been one of the largest direct beneficiaries through the JR East Pass and Japan Rail Pass products, the Tokyo Station and Shinjuku Station shopping traffic, and the Tohoku and Hokuriku tourism corridors that the Shinkansen serves.

The fiscal 2024 results returned JR East to substantive profitability, with operating income recovering toward pre-pandemic levels and the dividend restored. The strategic priorities since articulated — accelerated station-anchored urban development, expansion of Suica and the JRE Point loyalty program, and deeper digital integration through the JR East app — all assume the pre-pandemic ridership baseline will not fully return but the non-rail revenue base will continue to grow.

The case for JR East as Japan’s most overlooked infrastructure investment

Most non-Japanese investors who look at Japanese infrastructure default to the trading houses — Mitsubishi, Itochu, Mitsui — or to the electric utilities. JR East rarely makes the shortlist, partly because the railway label undersells the real business and partly because the company is not in the headline indices that global allocators track most closely. But the underlying asset is unusual. JR East owns irreplaceable land directly under the most valuable real estate in Japan, captures roughly seventeen million daily customer interactions, operates a payments network, and runs three Shinkansen routes that — through inbound tourism — are effectively long-dated options on Japan’s attractiveness as a destination. The dividend has been restored, the balance sheet came through the pandemic intact, and the capital programme is increasingly tilted toward station-development projects with clear unit economics rather than incremental rail expansion.

The risk factors are visible: demographic decline outside the Kanto core, regulatory constraints on rail fares, the cost trajectory of the conventional network in lower-density Tohoku, and the long-term capital commitment to maintaining mountain lines and coastal infrastructure exposed to seismic and weather events. The pandemic demonstrated that the demand base for the central commuter network is not perfectly inelastic. None is fatal.

FAQ

Who owns JR East?

JR East — East Japan Railway Company — is a publicly listed company on the Tokyo Stock Exchange under ticker 9020. The Japanese government’s residual ownership stake was progressively divested through public offerings between 1993 and 2002, after which JR East became a fully privately owned company. Ownership is now distributed across Japanese trust banks acting on behalf of institutional investors, global asset managers, and individual shareholders, with no controlling shareholder and no continuing state ownership.

How is JR East different from JR Central and JR West?

The three Honshu JR companies operate different geographies and different business mixes. JR Central runs the Tokaido Shinkansen between Tokyo and Shin-Osaka — the single most profitable rail corridor in Japan — and is overwhelmingly a railway business. JR West runs the Sanyo Shinkansen onward to Hakata and serves the Kansai region. JR East is the largest by passengers and route length, covers the entire Kanto region together with Tohoku and Niigata, and has the highest non-rail revenue share of the three, with retail, real estate, and Suica payments contributing approximately forty percent of total revenue.

What is Suica and how does JR East benefit from it?

Suica is the contactless IC card JR East launched in November 2001 for transit fare payment on its commuter network. The card was progressively extended to accept payments at convenience stores, vending machines, restaurants, and a broad range of small-ticket merchants, and was integrated into Apple Pay in 2016 and Google Wallet subsequently. JR East benefits from Suica through merchant fees on non-transit transactions, prepaid float balances, integration with the JRE Point loyalty program, and the consumer-data and engagement value of operating one of Japan’s largest electronic-money networks directly rather than through a spun-off subsidiary.

What is JR East’s largest non-rail business?

The largest non-rail revenue contribution comes from the station-retail and real-estate segments combined. Station retail includes the Lumine fashion mall chain at approximately fourteen of the largest stations, the Atre format at over twenty-five stations, and the ecute upscale food-and-gift format inside the ticket gates at major locations. Real estate covers office and hotel developments above and adjacent to major stations — Tokyo, Shinjuku, Shinagawa, Yokohama, Sendai — including the multi-phase Takanawa Gateway development around the new Yamanote Line station opened in 2020.

How did JR East come through the pandemic?

JR East posted its first full-year loss as a listed company in fiscal 2020 — approximately five hundred and eighty billion yen — and a second consecutive loss in fiscal 2021 as commuter and Shinkansen ridership fell by between thirty and forty percent at the trough. The recovery has been steady. By fiscal 2024 conventional-line ridership had returned to roughly ninety percent of pre-pandemic levels and Shinkansen ridership had recovered further, supported by record inbound tourism. The company has returned to profitability, restored the dividend, and re-anchored its strategy around station-anchored urban development, Suica expansion, and digital integration.

Working with JR East

For retail brands, restaurant operators, and consumer-services companies, the practical entry point into JR East is through the leasing and tenant-acquisition organisations at Lumine, Atre, ecute, and the station-development subsidiaries that handle the standalone projects. Tenancy decisions involve format fit, foot-traffic projections, and operating-model alignment with the station’s commuter patterns; the qualification cycle is slower than at a typical Japanese shopping centre but the customer base is materially captive.

For real-estate investors and construction partners, JR East participates in joint-venture redevelopments around major stations and engages with overseas operators in hotels and serviced residences. For technology suppliers, the company operates a substantial in-house IT organisation alongside JR East Information Systems and is increasingly open to overseas vendors in rolling-stock telematics, station automation, and payments infrastructure. For tourism operators, the JR East Pass and Japan Rail Pass distribution networks are direct channels into one of the largest inbound-traveller flows in Asia.

If your company provides station-retail concepts, hospitality and hotel operations, real-estate development capital, railway technology, payments and loyalty infrastructure, or inbound-tourism services relevant to JR East — or if you are evaluating Japanese commuter-rail and station real estate as part of a regional investment strategy — Japonity’s business matching service can help structure a credible first conversation with the right counterparty inside the JR East group.

Related from Japonity — Japan’s passenger railways & rail conglomerates

- JR Central — The Tokaido Shinkansen monopoly and the maglev moonshot

- Tokyu Corporation — The Shibuya-redeveloping rail conglomerate

- Hankyu Hanshin Holdings — Kansai’s railway-real-estate-entertainment empire

- Seibu Holdings — Tokyo’s western-suburb rail empire + Prince Hotels + Lions

- Kintetsu Group Holdings — Japan’s longest private railway — Osaka-Nara-Ise-Nagoya

Want to source Japanese products beyond these company profiles? Japonity also runs a Japan Sourcing Hub — a research-grade catalogue of 1,185 verified Japanese food products and 200+ overseas EC stores, ready for B2B procurement.

Interested in Japanese business opportunities?

Whether you're looking for technology partners, engineering talent, or market insights — we can help connect you with the right Japanese organizations.

Get in Touch →