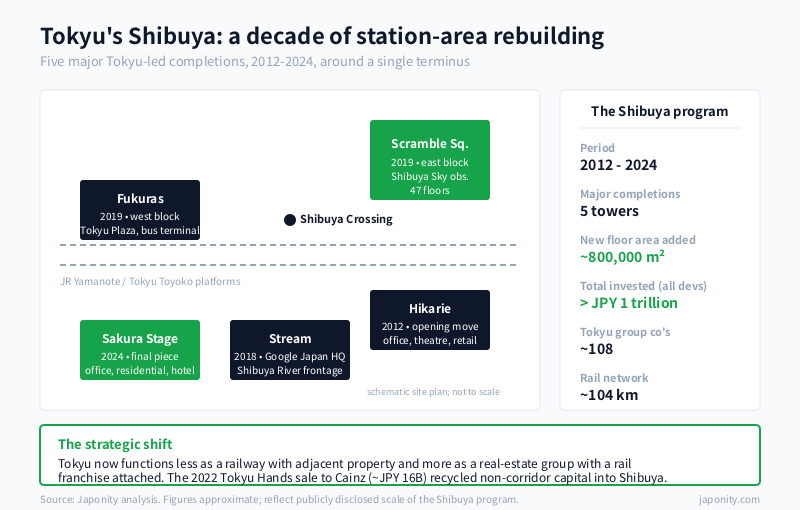

Tokyu Corporation is the only major Japanese private railway whose name has, over the past decade, become almost interchangeable with the redevelopment of a single railway station. Between 2014 and 2024 the company anchored what is collectively the largest single-station redevelopment program in Japanese history — Shibuya Stream, Shibuya Scramble Square, Shibuya Sakura Stage, and a string of supporting towers around the station the company has called home since the 1930s — at a cumulative price tag estimated at well above one trillion yen across all participating developers. That program sits on top of an operating business that already encompassed approximately 104 kilometres of southwestern Tokyo private railway, the Tokyu Department Store chain, the Tokyu Hotels group, the Tokyu Plaza shopping malls, the Bunkamura culture complex, and approximately 108 consolidated group companies spanning real estate, retail, hotels, advertising, and supermarket operations. In 2022 the group sold the Tokyu Hands variety-store chain to home-center operator Cainz for approximately sixteen billion yen — a transaction that signalled, more than any redevelopment ribbon-cutting, how seriously the new Tokyu was willing to trim non-core assets to fund what comes next.

From a Mekama tram line to a Shibuya conglomerate

The company that became Tokyu Corporation began in 1922 as Mekama Electric Railway — Meguro-Kamata Electric Railway — a single suburban tram line opening the southwestern corridor between Meguro and Kamata to commuter traffic. Its founder, Keita Goto, was a former Ministry of Railways bureaucrat who left government service to acquire and develop the line, and his career thereafter is one of the foundational case studies in Japanese post-war business history. Goto’s playbook was elementary in retrospect and revolutionary at the time: buy a railway, develop the land along it for residential housing, anchor the terminus stations with department stores and entertainment venues, and capture every layer of the resulting commuting and shopping economy.

Through a sequence of acquisitions and mergers during the 1920s and 1930s — including the Tokyo Yokohama Electric Railway, which gave the group what is now the Toyoko Line connecting Shibuya to Yokohama — the operation consolidated into Tokyu Corporation in 1942. The same period saw the establishment of what would become Tokyu Department Store at the Shibuya terminus and the early commercial development of the surrounding station area, a relationship between rail operator and station-front commercial property that has structurally defined the company ever since. Headquarters sit in Shibuya, immediately above and adjacent to the station the company has been redeveloping at scale since the early 2010s.

The post-war decades added the Den-en-toshi Line — literally the “garden-city line” — running southwest from Shibuya through Setagaya into the planned Tama Den-en-toshi development, one of the most ambitious private-sector new-town projects in post-war Japan. The Meguro, Setagaya, Oimachi lines and smaller branches filled out a network now covering approximately 104 kilometres across central and southwestern Tokyo and the northern suburbs of Yokohama.

The Shibuya thesis

The single most important strategic fact about Tokyu Corporation today is that it is, in commercial-property terms, the principal landlord of Shibuya. Other developers — Mitsui Fudosan, Mitsubishi Estate, Tokyu Land Corporation as a sister entity, and the East Japan Railway Company that owns the JR Yamanote Line platforms — are all present in the station area, but no other single corporate group has the multi-decade horizontal and vertical control of the immediate station environs that Tokyu does. The company’s headquarters, its flagship department store, its hotel inventory, its bus terminals and its principal rail platforms all sit within a roughly five-minute walking radius of Shibuya Crossing.

Between 2014 and 2024 the group orchestrated a sequence of redevelopment projects that, taken together, constitute the most aggressive single-station rebuilding effort in Japanese real-estate history. Shibuya Hikarie, completed in 2012 on the former site of the Tokyu Bunka Kaikan, was the opening move. Shibuya Stream opened in 2018 on a long, narrow site recovered from the realignment of the underground Toyoko Line tracks, anchored by a Google Japan tenancy and a riverside promenade along the Shibuya River. Shibuya Scramble Square, opened in 2019, rebuilt the eastern station block as a forty-seven-story tower whose Shibuya Sky observation deck — three open-air decks at roughly 230 metres above grade — quickly became one of the most-photographed views in Tokyo. The Shibuya Fukuras tower on the western station block opened in late 2019. Shibuya Sakura Stage, the final piece on the southern station block, completed in 2024.

The cumulative effect is a station functionally rebuilt around the original Yamanote Line stop. Pedestrian flow has been re-engineered through new underground concourses and elevated walkways; office inventory in the immediate station area has roughly doubled. For an investor or partner, the practical implication is that Tokyu Corporation has become not principally a railway company that happens to own real estate but a real-estate group with a railway franchise attached. The fiscal contribution of real estate and adjacent property businesses to consolidated operating profit has grown commensurately.

What the 108 group companies actually do

The Tokyu group’s consolidated structure, with approximately 108 group companies, looks at first glance like a classic diversified Japanese conglomerate. On closer inspection it is something more disciplined: a vertically and horizontally integrated portfolio organised around the rail network’s catchment area. The major business segments break down approximately as follows.

| Segment | Principal businesses | Strategic role |

|---|---|---|

| Transportation | Tokyu railway (Toyoko, Den-en-toshi, Meguro, Setagaya, Oimachi, Ikegami, Tokyu-Tamagawa lines); Tokyu Bus | Demand generator and corridor anchor |

| Real estate | Tokyu Land Corporation (sister listed); office, retail and residential development around Shibuya, Futako-Tamagawa, Musashi-Kosugi | Principal profit engine post-redevelopment |

| Retail | Tokyu Department Store; Tokyu Store supermarkets; Tokyu Plaza shopping malls (Ginza, Omotesando-Harajuku, Shibuya, Akasaka); 109 fashion buildings | Station-anchored consumer capture |

| Hotel & resort | Tokyu Hotels chain; Tokyu Stay business-travel brand; resort hotels in Hokkaido, Karuizawa, Hakone | Cross-sell with rail and inbound tourism |

| Life services & ICT | Tokyu Security, its.communications (cable TV and broadband), Tokyu Power Supply (retail electricity) | Last-mile household relationship along the line |

| Construction | Tokyu Construction (listed separately) | Internal redevelopment delivery capacity |

| Advertising & cultural | Tokyu Agency; Bunkamura culture complex; theaters and event venues | Brand and demand-shaping infrastructure |

The shape of this portfolio is not accidental. It is the same Goto playbook scaled across a century: control the rail corridor, develop the residential catchment, anchor the terminus stations with commercial property, and capture the household relationship through retail, broadband, electricity, and security services. The 108 group companies are mostly variations on those themes, not unrelated diversification.

The Tokyu Hands divestiture

In 2022 Tokyu Corporation sold the Tokyu Hands variety-store chain to Cainz, the home-center operator owned by the Beisia group, for approximately sixteen billion yen. The transaction was modest in absolute size by Japanese M&A standards but symbolically significant. Tokyu Hands had been acquired in 2010 and operated as one of the more visible consumer-facing brands in the group portfolio, with flagship stores in Shibuya, Shinjuku, Ikebukuro, Yokohama and a string of regional capitals.

The sale signalled that the new Tokyu was prepared to part with brand-name consumer assets that did not fit the geographic logic of the rail corridor. Tokyu Hands had national reach by design; the reorganised strategic frame is increasingly oriented around dense corridor capture and station-anchored property economics. Capital recycled from the divestiture has funded redevelopment commitments. The brand has continued under Cainz ownership, rebranded simply as “Hands” in 2022.

Tokyu compared with Hankyu Hanshin, Seibu and Keio

Tokyu sits within a small cohort of major Japanese private rail operators that have, over the post-war decades, all evolved into integrated rail-real-estate-retail conglomerates. The comparison with peers is instructive because the strategic shapes diverge meaningfully despite the apparent similarity of the business model.

| Operator | Network base | Distinctive strategic axis |

|---|---|---|

| Tokyu Corporation | Southwestern Tokyo, Yokohama (~104 km) | Shibuya station-area redevelopment; Tokyu Hotels; ~108 group companies |

| Hankyu Hanshin Holdings | Osaka-Kobe-Kyoto Kansai corridor | Umeda redevelopment; Hanshin Tigers baseball; Takarazuka Revue; integrated Kansai consumer franchise |

| Seibu Holdings | Northwestern Tokyo, Saitama, Chichibu | Prince Hotels chain; Saitama Seibu Lions baseball; post-bankruptcy financial discipline |

| Keio Corporation | Western Tokyo (Shinjuku-Hachioji axis) | Shinjuku terminal anchor; tighter geographic focus; smaller group footprint |

Hankyu Hanshin is the closest peer in breadth — its Umeda redevelopment is the western counterpart to Shibuya, and its entertainment assets including the Hanshin Tigers baseball team and the Takarazuka Revue give it a consumer-brand portfolio Tokyu lacks. Seibu carries a different inheritance — Prince Hotels, the Saitama Seibu Lions, and a more turbulent corporate history including a delisting and relisting in the late 2000s. Keio is structurally tighter, a single principal rail corridor terminating at Shinjuku, proportionately more dependent on rail and station-front retail.

What distinguishes Tokyu among this cohort is the unusual concentration on a single terminus — Shibuya — and the willingness to commit a decade of capital and management attention to rebuilding it. Umeda is comparable in scale but distributed across multiple operators including JR West and Hankyu itself; Shinjuku’s redevelopment is led by multiple parties with no single dominant landlord. Shibuya, post-2024, is arguably the most concentrated single-operator station-area redevelopment outcome in Japan.

The principal Shibuya redevelopment projects

For readers tracking the specific projects that constitute the Shibuya program, the principal completed works since 2012 are summarised below. Tokyu Corporation is the lead or co-lead developer on each.

| Project | Opened | Anchor use |

|---|---|---|

| Shibuya Hikarie | 2012 | Office, retail (ShinQs), theatre, restaurants |

| Shibuya Stream | 2018 | Google Japan HQ, hotel, retail along Shibuya River |

| Shibuya Scramble Square (East) | 2019 | Office, retail, Shibuya Sky observation deck |

| Shibuya Fukuras | 2019 | Office, retail (Tokyu Plaza Shibuya), bus terminal |

| Shibuya Sakura Stage | 2024 | Office, residential, retail, hotel on the south station block |

Phased completion of the Shibuya Scramble Square central and western blocks remains in progress beyond 2024. The total floor area added across the program is approximately 800,000 square metres of new office and mixed-use space, against a roughly comparable amount of older inventory that has been demolished or substantially refurbished. The financial commitment, across all developers including Tokyu, JR East, the Tokyo Metro, and Tokyu Land Corporation as a separate listed entity, is estimated at well above one trillion yen.

The dual structure with Tokyu Land Corporation

Anyone researching Tokyu encounters two listed entities that share the Tokyu name: Tokyu Corporation (Tokyo Stock Exchange code 9005) and Tokyu Fudosan Holdings, the listed parent of Tokyu Land Corporation. The relationship is collaborative rather than fully consolidated. Tokyu Corporation is the rail operator and the original Goto-era core; Tokyu Land Corporation, established in 1953 as a separately listed real-estate development company, is the larger pure-play property arm. The two operate as separately listed companies with overlapping but distinct shareholder bases, and they frequently co-develop projects — particularly in and around Shibuya — but neither controls the other.

For investors and partners, the practical implication is that exposure to “Tokyu real estate” can be obtained through either entity, with somewhat different risk-and-return profiles. Tokyu Corporation carries the rail and infrastructure businesses alongside its property book; Tokyu Land Corporation is a closer comparable to Mitsui Fudosan or Mitsubishi Estate as a pure-play developer. The Shibuya redevelopment program involves both companies in different roles on different sites.

Leadership and governance

Tokyu Corporation’s senior leadership through the late 2010s and into the 2020s has been organised around the dual figures of Hirofumi Nomoto, the long-serving executive who led the company through much of the Shibuya redevelopment period and who has served as chairman, and Toshikiyo Hori, who has held senior operating roles including the presidency through the post-pandemic phase. Specific role assignments evolve year to year and the company communicates them through standard listed-company disclosures; current officeholders should be verified against the most recent disclosure documents.

Governance follows standard Japanese listed-company practice with a board including outside directors, a nomination and compensation advisory body, and ordinary shareholder meeting cycles. There is no controlling shareholder block; ownership is distributed across Japanese trust banks acting on behalf of institutional investors, retail shareholders along the rail corridor, and cross-shareholdings of modest scale with selected business partners.

Why Tokyu matters to non-Japanese counterparties

For commercial-property investors and tenants, Tokyu is the largest single landlord with which to negotiate office or retail space in the Shibuya station area — an area that, post-2024, hosts a disproportionate share of the Tokyo offices of foreign technology and creative companies. For hotel operators and travel groups, the Tokyu Hotels and Tokyu Stay chains are mid-market consolidation candidates with strong corridor distribution. For consumer-brand companies, the Tokyu Department Store, Tokyu Plaza and 109 platforms remain meaningful retail distribution channels in central Tokyo, particularly for inbound-tourist-facing categories. For infrastructure suppliers, the rail network’s modernisation and continued through-running integration with Tokyo Metro and other operators creates ongoing procurement opportunities in signalling, rolling stock, and station systems.

What makes Tokyu distinctive among Japanese private rail operators is the unusual coherence of its strategic frame. The company has spent a decade rebuilding a single station while quietly trimming the brand assets — Tokyu Hands most visibly — that did not fit the geographic logic. The result is a more focused, more property-centric, and arguably more investable group than the sprawling early-2000s version. The Goto playbook, a century in, is being run with more discipline than at any prior point in the company’s history.

FAQ

Who founded Tokyu Corporation and when?

Tokyu Corporation traces its origins to 1922, when Mekama Electric Railway — Meguro-Kamata Electric Railway — opened the original tram line between Meguro and Kamata in southwestern Tokyo. The driving figure was Keita Goto, a former Ministry of Railways official who left government service to acquire and develop the line and who built, through subsequent acquisitions and mergers including the 1939 absorption of the Tokyo Yokohama Electric Railway, what consolidated formally as Tokyu Corporation in 1942. Goto’s “rail plus residential development plus terminus department store” playbook is the foundational template for the modern integrated Japanese private-rail conglomerate.

What rail lines does Tokyu operate?

Tokyu operates approximately 104 kilometres of railway across southwestern Tokyo and northern Yokohama, organised into seven principal lines: the Toyoko Line (Shibuya to Yokohama), the Den-en-toshi Line (Shibuya southwest into Tama Den-en-toshi and onward to Chuo-Rinkan), the Meguro Line (Meguro to Hiyoshi), the Oimachi Line, the Setagaya Line, the Ikegami Line, and the Tokyu-Tamagawa Line. Several of these lines through-run onto Tokyo Metro and other operators’ networks, materially extending the practical commute reach. Tokyu Bus operates the principal bus network within the same corridor.

How big was the Shibuya redevelopment program?

Between 2012 and 2024, Tokyu Corporation and its co-developers — including Tokyu Land Corporation, JR East and Tokyo Metro — completed a sequence of major projects in and around Shibuya station: Shibuya Hikarie in 2012, Shibuya Stream in 2018, Shibuya Scramble Square’s east tower with the Shibuya Sky observation deck in 2019, Shibuya Fukuras in 2019, and Shibuya Sakura Stage in 2024. The combined floor area added across the program is approximately 800,000 square metres of new office and mixed-use space, and the cumulative investment across all participating developers is estimated at well above one trillion yen, making it the largest single-station redevelopment effort in Japanese history.

What happened with Tokyu Hands?

Tokyu Hands, the variety-store chain, had been operated as part of the Tokyu group since 2010. In 2022 Tokyu Corporation sold the chain to Cainz, the home-center operator owned by the Beisia group, for approximately sixteen billion yen. The brand has continued under Cainz ownership, rebranded simply as “Hands” in 2022. The sale was a relatively rare divestiture of a well-known consumer brand by a major Japanese private-rail conglomerate, and signalled Tokyu’s willingness to trim non-corridor assets to fund the Shibuya redevelopment commitments.

How does Tokyu compare with Hankyu Hanshin and Seibu?

All three are major Japanese private-rail conglomerates with diversified rail-real-estate-retail-hotel portfolios, but the strategic axes differ. Hankyu Hanshin Holdings, anchored in the Osaka-Kobe-Kyoto Kansai corridor, has a comparable redevelopment program around Osaka’s Umeda station and adds entertainment assets including the Hanshin Tigers baseball team and the Takarazuka Revue theatre company. Seibu Holdings, operating northwestern Tokyo and Saitama, owns the Prince Hotels chain and the Saitama Seibu Lions baseball team and carries a more turbulent post-2000s corporate history. Tokyu is distinguished by the unusual concentration of its strategic effort on a single terminus — Shibuya — and the resulting depth of property exposure there.

Working with Tokyu Group

For commercial property tenants, the practical entry point to Tokyu is the company’s office leasing organisation in Shibuya, which handles the post-2024 inventory across Shibuya Scramble Square, Shibuya Stream, Shibuya Sakura Stage, Shibuya Fukuras and Shibuya Hikarie. For hospitality partners and travel groups, Tokyu Hotels and Tokyu Stay handle corporate contracting, franchise and management agreements, and group-tour relationships. For consumer brands seeking retail distribution in central Tokyo, the Tokyu Department Store, the Tokyu Plaza shopping malls in Ginza, Omotesando-Harajuku and Shibuya, and the 109 fashion buildings offer some of the most location-specific consumer-facing real estate in the country. For infrastructure suppliers, Tokyu’s procurement organisation handles rolling stock, signalling, station systems, and bus-fleet contracts on cycles that align with rail-industry norms.

If your company provides commercial real-estate services, hospitality management, consumer retail brands, rail infrastructure technology, station-area mobility solutions, or culture and entertainment programming relevant to Tokyu’s Shibuya estate and corridor — or if you are evaluating Tokyo southwestern corridor exposure as part of a Japan investment strategy — Japonity’s business matching service can help structure a credible first conversation with the right counterparty inside the Tokyu group.

Related from Japonity — Japan’s passenger railways & rail conglomerates

- JR East — The world’s largest railway by passengers — and Japan’s biggest station-retail empire

- JR Central — The Tokaido Shinkansen monopoly and the maglev moonshot

- Hankyu Hanshin Holdings — Kansai’s railway-real-estate-entertainment empire

- Seibu Holdings — Tokyo’s western-suburb rail empire + Prince Hotels + Lions

- Kintetsu Group Holdings — Japan’s longest private railway — Osaka-Nara-Ise-Nagoya

Want to source Japanese products beyond these company profiles? Japonity also runs a Japan Sourcing Hub — a research-grade catalogue of 1,185 verified Japanese food products and 200+ overseas EC stores, ready for B2B procurement.

Interested in Japanese business opportunities?

Whether you're looking for technology partners, engineering talent, or market insights — we can help connect you with the right Japanese organizations.

Get in Touch →