Of the roughly 250 anime titles produced in Japan each year, fewer than ten studios account for the bulk of the hours that actually travel — onto Netflix carousels, Crunchyroll seasonal slates, Disney+ Hotstar in Asia, Bilibili in China, and the licensed merchandise pipelines that flow through Los Angeles, Paris and Singapore. Industry estimates put their combined share at roughly 80% of foreign-licensed output. The list below is therefore not a fan ranking of “best studios”; it is a business map. For a foreign importer, broadcaster, investor or brand sponsor, these are the ten Japanese counterparties whose names you will see again and again on the deal sheet — and whose business models determine what you can actually buy.

Methodology

We ranked Japan’s anime studios on three weighted criteria: annual TV-and-film output volume (episode hours produced or co-produced); foreign-licensed hours (titles that secured overseas streaming or theatrical distribution in the past three seasons); and recent breakout titles capable of moving merchandise, theme-park and game licences abroad. Output data draws on trade-press aggregations (Oricon, Anime News Network production databases, Filmarks) cross-checked against studio annual reports where available. We deliberately excluded production-committee shell companies and pure CGI subcontractors. Where exact figures are not publicly disclosed — and most Japanese studios are privately held — we relied on industry estimates and signalled them as such.

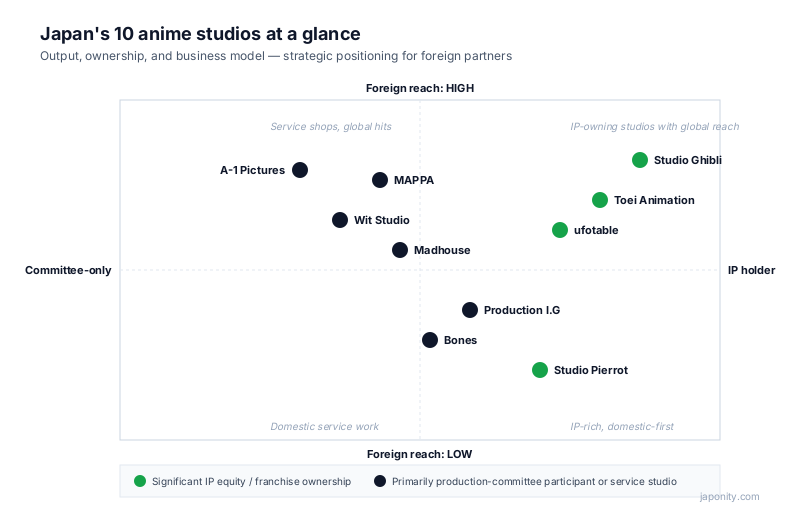

The ten studios at a glance

| Studio | Founded | Signature works | Business model | Foreign partnerships |

|---|---|---|---|---|

| Toei Animation | 1948 | One Piece, Dragon Ball, Sailor Moon | IP holder + committee | Crunchyroll, Netflix, global licensors |

| MAPPA | 2011 | Attack on Titan (final seasons), Jujutsu Kaisen, Chainsaw Man | Committee participant; producing more in-house | Crunchyroll, Sony, Netflix originals |

| ufotable | 2000 | Demon Slayer, Fate/Zero, Fate/stay night UBW | IP holder via Aniplex co-equity | Sony Music / Aniplex, Crunchyroll |

| Wit Studio | 2012 | Attack on Titan (S1–3), Spy×Family, Vinland Saga | Service studio; IG Port subsidiary | Netflix originals, Sony, Twin Engine |

| Studio Ghibli | 1985 | Spirited Away, Princess Mononoke, The Boy and the Heron | IP holder; Nippon TV holding (2023) | GKIDS (US), Wild Bunch (EU), Max (US streaming) |

| A-1 Pictures | 2005 | Sword Art Online, Kaguya-sama, Solo Leveling co-prod | Aniplex (SMEJ) captive studio | Sony Pictures, Crunchyroll, Netflix |

| Madhouse | 1972 | Hunter × Hunter, One-Punch Man S1, Death Note | Committee participant; NTV-affiliated | Netflix, Marvel (One-Punch Man S2 distrib) |

| Bones | 1998 | My Hero Academia, Mob Psycho 100, Fullmetal Alchemist | Committee participant; selective IP equity | Crunchyroll, Funimation legacy library |

| Production I.G | 1987 | Ghost in the Shell, Haikyu!!, Psycho-Pass | Listed (IG Port); IP co-owner on flagship titles | Netflix, Warner Bros., Paramount (GitS film) |

| Studio Pierrot | 1979 | Naruto, Bleach, Tokyo Ghoul, Black Clover | IP holder on Naruto, long-running franchise model | Viz Media, Crunchyroll, Netflix |

Toei Animation

Toei is the closest thing the Japanese anime business has to a blue-chip corporate. Founded in 1948 and listed on the Tokyo Stock Exchange, it sits inside the broader Toei Company film group and operates more like a Hollywood major than a creative atelier. Its catalogue — One Piece, Dragon Ball, Sailor Moon, Digimon, Pretty Cure — is the bedrock of the foreign anime market, and most of these IPs are partly or wholly owned by Toei itself, which is rare. The strategic interest for a foreign partner is twofold: predictable franchise-management practices and an actual public balance sheet you can underwrite. The trade-off is that Toei rarely sells equity in a flagship IP; what is on the table is licensing, co-production and merchandising, not ownership.

MAPPA

MAPPA was founded in 2011 by Masao Maruyama, formerly co-founder of Madhouse, and within a decade became the most-discussed studio in the global anime conversation. Attack on Titan’s final seasons, Jujutsu Kaisen, Chainsaw Man and Hell’s Paradise pushed MAPPA into a category occupied previously only by Toei and Ghibli: brand recognition outside Japan. Historically MAPPA was a committee participant rather than an IP owner, but trade-press reports indicate the studio is steadily taking larger equity stakes in original projects to capture more of the upside. For a foreign broadcaster, the appeal is the contemporary, action-led tone and a willingness to talk directly. The risk, candidly discussed in the trade press, is production-pipeline strain.

ufotable

ufotable is the studio that proved a mid-sized animation house could become a franchise owner. Founded in 2000, it built its reputation on the Fate series before achieving global escape velocity with Demon Slayer, whose theatrical instalment Mugen Train became Japan’s all-time top-grossing film. Critically, ufotable holds significant equity in the Demon Slayer franchise alongside Aniplex and Shueisha — a posture that distinguishes it from most service studios. For a foreign partner, ufotable is therefore not a place to commission work-for-hire; it is a counterparty to negotiate with for premium licences, theatrical windows and high-end merchandise. The studio’s slate is small; access is the constraint.

Wit Studio

Wit Studio was founded in 2012 as a subsidiary of IG Port — the same listed holding company that controls Production I.G — specifically to handle Attack on Titan’s first three seasons. After that landmark, Wit’s identity broadened: Spy×Family in partnership with CloverWorks, Vinland Saga, Ranking of Kings, Bubble for Netflix. Wit operates more as a high-end service studio than a primary IP holder, but its parent IG Port is publicly listed, which gives foreign investors a rare proxy. The studio’s recent slate is notable for the depth of its Netflix and Sony Pictures relationships, making it one of the most accessible Japanese studios for English-language-first commissioning. The economics, however, sit largely with committees and platforms.

Studio Ghibli

Ghibli is the outlier on every axis. Founded in 1985 by Hayao Miyazaki, Isao Takahata and Toshio Suzuki, the studio produces roughly one film per multi-year cycle rather than seasonal TV slates, yet captures a disproportionate share of theatrical and back-catalogue licensing value worldwide. In 2023 Nippon Television Network (NTV) acquired a majority stake, formally bringing Ghibli into the NTV holding structure — a move framed publicly as a succession solution rather than a strategy pivot. For foreign distributors, the practical map is well established: GKIDS holds North American rights, Wild Bunch in much of Europe, and HBO Max (now Max) carries streaming in the US. There is no equity to buy; there are theatrical, streaming, merchandise and theme-park-adjacent licences to negotiate, almost always through NTV-blessed channels.

A-1 Pictures

A-1 Pictures is a wholly owned subsidiary of Aniplex, itself a subsidiary of Sony Music Entertainment (Japan). Founded in 2005 explicitly to handle Aniplex’s growing in-house production needs, A-1 is the closest example in the anime industry of a captive studio inside a global media conglomerate. Sword Art Online, Kaguya-sama: Love Is War, Lycoris Recoil and a co-production role on Solo Leveling sit on its slate. For a foreign partner, A-1’s value is paradoxically not the studio itself but the Aniplex–Sony stack behind it: licensing, music publishing, mobile games (via Aniplex’s affiliates) and theatrical distribution can be assembled inside a single counterparty conversation. This is the most Hollywood-shaped Japanese animation business in the industry.

Madhouse

Founded in 1972 by Masao Maruyama and three other former Mushi Production animators, Madhouse is one of the longest-running studios in Japanese animation and an industry training ground — many top directors and producers, including MAPPA’s founders, came through it. Its catalogue is unusually canonical: Death Note, Monster, Hunter × Hunter (2011), One-Punch Man season one, Trigun, Black Lagoon. Madhouse is a Nippon TV-affiliated entity and typically participates as a member of production committees rather than as an IP owner. For a foreign partner, Madhouse is a strong destination for prestige adaptation work and reliable production quality; it is less promising as a source of equity in original IP.

Bones

Bones was founded in 1998 by former Sunrise staff and built a reputation on technically demanding action animation — Fullmetal Alchemist: Brotherhood, Mob Psycho 100, My Hero Academia, Bungo Stray Dogs. Like most studios in this list, Bones operates primarily as a committee participant rather than a primary IP holder, but it has selectively taken equity in original projects (Carole & Tuesday with Netflix, Witch Hat Atelier in development). For foreign partners, Bones is a credible choice when the brief is high-craft action animation, and the studio’s relationships with Crunchyroll and the legacy Funimation library mean its catalogue is largely already in the North American market. It is a craft-led, not a balance-sheet-led, counterparty.

Production I.G

Production I.G, founded in 1987, is the closest Japanese studio to a publicly investable IP business: it is the operating company beneath the listed holding IG Port, alongside Wit Studio. Ghost in the Shell is the franchise that defines I.G abroad and remains the most exported intellectual property the studio co-owns, with Paramount’s live-action film and continuing Netflix productions paying back into the rights structure. Beyond Ghost in the Shell, Haikyu!! and Psycho-Pass are global revenue drivers. For a foreign investor, IG Port is the rare way to take a public-market position adjacent to anime production; for a foreign distributor, I.G is one of the more sophisticated negotiating counterparties because it routinely thinks in co-production rather than pure licence terms.

Studio Pierrot

Studio Pierrot, founded in 1979, is the studio behind several of the most durable shōnen franchises Japan has exported: Naruto and its sequel Boruto, Bleach, Tokyo Ghoul, Black Clover. Pierrot is privately held but, crucially, it is a significant IP co-owner on Naruto — one of the highest-grossing animation franchises of the past two decades — and runs a long-running franchise model rather than chasing breakouts. For a foreign partner the proposition is straightforward: this is a catalogue business with deep merchandise, game, and live-event licensing pipelines via Viz Media in North America and Crunchyroll for streaming. The studio is less visible in industry press than MAPPA or ufotable, which makes it underrated in deal conversations relative to its actual revenue base.

What it means for a foreign buyer

The strategic geography that emerges from the list is sharper than the standard “top studios” framing suggests. Three patterns matter.

First, only a handful of studios are meaningful IP holders: Toei, Ghibli, ufotable, Production I.G and Studio Pierrot. The rest, including MAPPA and Wit despite their global profile, are primarily committee participants — meaning a foreign buyer who wants ownership economics, not just distribution licences, has a short list of doors to knock on, and most of those doors are now controlled by larger parents (NTV behind Ghibli, Aniplex–Sony behind A-1, IG Port over Production I.G and Wit).

Second, the studios that look most “available” to a foreign commissioner — MAPPA, Wit, Bones, Madhouse — are often the least available as equity counterparties. They produce; they do not sell pieces of themselves.

Third, the cleanest way for a foreign capital allocator to take an anime position today is the listed proxies: Toei Animation Co. on the Tokyo Stock Exchange and IG Port. For licensing-side counterparties — brand managers, theme-park licensors, merchandise buyers, broadcasters — the actual deal flow concentrates around four hubs: Aniplex (Sony), NTV/Ghibli, Toei, and the Crunchyroll/Sony Pictures anime supply chain that touches most of the rest. That, more than any creative ranking, is the operating map.

FAQ

Which is the largest anime studio in Japan?

By revenue and catalogue value Toei Animation is the largest single anime studio in Japan, with the additional distinction of being publicly listed on the Tokyo Stock Exchange. By global cultural footprint Studio Ghibli has comparable weight despite a much smaller output. By recent breakout impact MAPPA and ufotable are the most-discussed studios in the trade press.

Which anime studios actually own their IP?

The clearest IP-holding studios in the top tier are Toei (Dragon Ball, One Piece, Sailor Moon), Studio Ghibli (full Ghibli library, now under NTV holding), ufotable (significant equity in the Demon Slayer franchise alongside Aniplex and Shueisha), Production I.G (co-owner of Ghost in the Shell) and Studio Pierrot (co-owner of Naruto). Most other studios operate as production-committee participants and earn from production fees and limited equity slices rather than from full franchise ownership.

Can a foreign company invest in an anime studio?

Indirectly, yes. Two listed counters give foreign investors meaningful exposure: Toei Animation Co., Ltd. on the Tokyo Stock Exchange and IG Port, the holding company over Production I.G and Wit Studio. Direct equity investment in privately held studios such as MAPPA, ufotable or Pierrot is generally not on offer in the public market, though M&A activity has increased — Ghibli’s 2023 acquisition by Nippon TV being the most prominent recent example.

Which studio made Demon Slayer?

ufotable produced the Demon Slayer: Kimetsu no Yaiba television series and the Mugen Train theatrical film, with Aniplex and Shueisha as co-rights holders. ufotable’s significant equity position in the franchise is what distinguishes it from a typical service studio and explains why it has been able to control the production tempo of the franchise so tightly.

How do anime studios actually make money?

The dominant model is the “production committee” (seisaku iinkai), a special-purpose vehicle in which a publisher, a TV network, a music label, a toy company, an advertising agency and the animation studio each contribute capital and split downstream revenue from broadcast, streaming, merchandise, music and games. Most studios earn a production fee plus a relatively small committee equity slice; only IP-owning studios such as Toei, Ghibli, ufotable, I.G and Pierrot capture meaningful franchise upside.

Foreign brand managers, distributors and investors evaluating Japanese anime partnerships can reach our editorial team via japonity.com/business-matching.

More from Japonity’s Japan Anime Business series

This article is part of a 10-piece editorial cluster on the business of Japanese anime. Read the rest:

- Inside Japan’s Anime Production Committee — How the money and rights really flow inside the joint-venture structure that funds almost every Japanese TV anime.

- Japan’s Anime Export Boom — Why overseas anime sales topped ¥1.7 trillion and overtook domestic for the first time in 2023.

- Licensing Anime IP: A 2026 Foreign Buyer’s Guide — Why Western licensing instincts produce wrong answers in Japan, and the eight-stage flow that actually closes deals.

- The New Geography of Anime Streaming — Crunchyroll, Bilibili, Netflix, Disney+ and others split the world by region, rights and business model.

- Why Akihabara Still Matters — Behind the neon, Tokyo’s Akihabara is a working B2B test market for anime IP — a foreign buyer’s walking tour.

- VTuber Economics — Inside the billion-dollar virtual influencer industry built by Cover (Hololive) and ANYCOLOR (Nijisanji).

- The Anime Merchandise Pipeline — From Tokyo factories to Comic-Con booths — how an anime figure actually travels to a foreign retail shelf.

- Japan’s Trillion-Yen Manga Industry — Inside a publishing business larger than anime — and the four Tokyo houses every foreign publisher should know.

- A Day in the Life of an Anime Animator — Inside the working day of a rank-and-file animator, and the structural reasons wages stay low across the industry.

Sourcing beyond anime? Japonity also runs a Japan Sourcing Hub — a research-grade catalogue of 1,185 verified Japanese food products and 200+ overseas EC stores that already stock them, with HS codes, certifications and supplier MOQs ready for B2B procurement.

Interested in Japanese business opportunities?

Whether you're looking for technology partners, engineering talent, or market insights — we can help connect you with the right Japanese organizations.

Get in Touch →