It is 4:47 a.m. in a low-rise apartment in Nerima, the Tokyo ward that has produced more of the world’s animation than any single neighborhood on earth, and a 24-year-old in-between animator is awake at her desk because the episode ships on Friday. The desk lamp is the only light in the room. The bento from the convenience store is half-eaten. The pencil — actual graphite, on actual paper, for a studio that has not yet finished its digital transition — is in her hand. This is the labor underneath the most successful soft-power export Japan has ever produced. It is also a labor crisis with direct implications for every foreign company that licenses, commissions, or sells Japanese animation — and one that increasingly belongs on the desk of every sourcing manager, ESG officer, and entertainment investor with Japan exposure.

A composite morning in Nerima

What follows is a composite drawn from reporting and from JAniCA and AJA labor surveys, not one individual’s day. Names, addresses, and timings are illustrative. The economics are not.

She wakes at 4:30 a.m. not because she wants to, but because she went to sleep at 1:00 a.m. with eighteen douga (in-between drawings) still owed to a key animator who needs them before the 11:00 a.m. studio handoff. She is paid roughly ¥200 per finished in-between, the per-drawing rate that has barely moved in two decades. On a good day she finishes thirty; on a bad day — a complex action sequence, multiple figures, elaborate hair — fewer than ten.

By 7:00 a.m. she has scanned the morning’s pages and emailed them in. She rides the Seibu Ikebukuro line two stops to a small office above a dry cleaner. The studio is one room with nine desks. Three are occupied by full-time employees on salary; the other six, including hers, are filled by gyōmu itaku contract workers — paid per piece, with no studio health insurance contributions, no overtime protection, no paid leave. Her contract is renewed quarterly. She has been there fourteen months.

Lunch is convenience-store onigiri at the desk. The afternoon is corrections — a key animator has rejected six of her in-betweens for stiff motion and wants them redrawn. There is no extra pay for the redraw. At 11:00 p.m. most of the contract workers leave. She stays until 1:30 a.m. because Friday is in three days and the line producer has been polite but specific.

She earns, in a typical month, somewhere between ¥150,000 and ¥180,000 before tax — a figure she could not live on if her parents did not subsidize her rent. The senior animators tell her the third year is when most people quit.

The numbers behind the scene

The composite above is not literary embellishment. It is a stylized average of what JAniCA — the Japan Animation Creators Association — has documented in periodic labor surveys since 2009, and what AJA reports in its annual Anime Industry Report. The picture is consistent across surveys, and it is bleak at the bottom of the ladder.

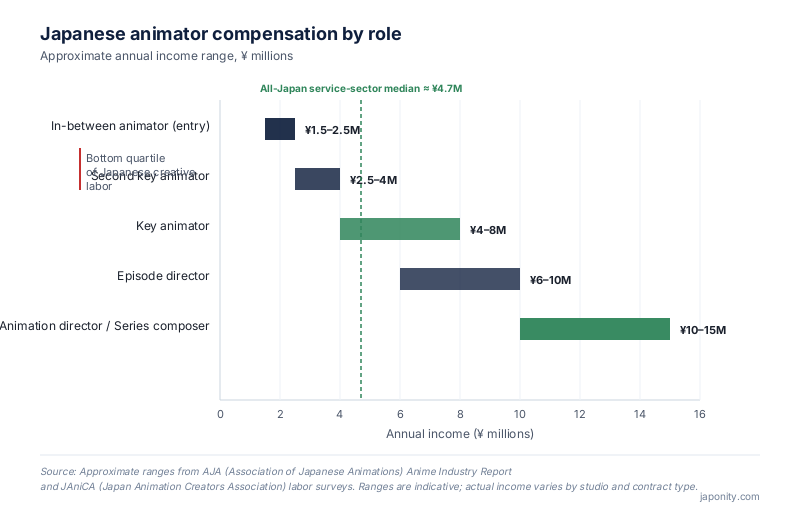

JAniCA’s most-cited 2019 figures put the industry-wide average animator income at roughly ¥4.4 million per year — a number that sounds tolerable until you disaggregate it by role. The average is pulled up by a small population of senior animation directors, character designers, and series composers earning in the double-digit millions. Strip them out and the picture for the bottom two quartiles of the workforce is much harder to defend.

The headline number that has driven nearly every international story about Japanese animation labor — in-between animators earning under ¥2 million per year at entry — is real, and has been real, with marginal year-on-year improvement, for most of the past fifteen years. JAniCA surveys consistently find that the youngest cohort works 50 to 70 hours per week, that “all-nighter” frequency in the run-up to ship dates is normalized, and that overwork-related illness — chronic back pain, RSI, depressive episodes, and in well-publicized cases, suicide — is recognized inside the industry as structural rather than individual.

| Role | Typical annual income (¥) | Notes |

|---|---|---|

| In-between animator (entry, 1–3 yrs) | ¥1.5M – ¥2.5M | Usually piece-rate gyōmu itaku contract; no benefits |

| Second key animator | ¥2.5M – ¥4M | Still typically piece-rate |

| Key animator (genga) | ¥4M – ¥8M | Wide variance; top names earn far more per cut |

| Episode director (enshutsu) | ¥6M – ¥10M | Usually salaried; small population |

| Animation director / Series composer | ¥10M – ¥15M+ | Top of the craft ladder; very small cohort |

Ranges are approximate, drawn from AJA and JAniCA survey data and industry reporting. Studio-by-studio variation is significant; ufotable, Kyoto Animation, and a small number of other IP-holding studios pay materially above these bands.

Set against an all-Japan service-sector median income of roughly ¥4.7 million, the bottom two rows of that table sit firmly in the lowest quartile of Japanese creative labor — and well below the bottom quartile of Japanese full-time employment overall.

Why the wages stay low — a structural answer

It is tempting to read these numbers as a story about exploitative studios. That is not quite right, and getting it wrong matters for foreign partners trying to assess risk. Most Japanese animation studios are not capturing windfall margins and pocketing the difference. The structural answer is much more uncomfortable: studios do not own the work.

Under Japan’s dominant production-committee (seisaku iinkai) system — explained in more depth in our explainer on the production-committee system — a TV anime is typically financed by a consortium of publishers, broadcasters, music labels, toy companies, and distributors. The studio that actually animates the show is a labor contractor inside that structure. It is paid a production fee. It rarely takes meaningful equity in the IP. When the show becomes a global phenomenon — when the merchandise, the games, the streaming rights, the theme park ride, the live-event tour, and the foreign distribution deals start generating multiples of the production budget — that upside flows to the committee members, not to the studio. And not to the animator.

This is the single most important fact about the industry’s labor economics. Until the studio captures equity in the IP it produces, there is no profit-share mechanism through which a hit can translate into materially higher wages at the desk. The studio’s revenue is largely fixed at signing. Its margins are squeezed by deadlines and by the next show in the pipeline. The animator’s piece-rate has nowhere to flow up from.

The talent drain

This structural compression is now meeting a labor market that, for the first time in the industry’s history, has alternatives. Chinese studios — many affiliated with Bilibili, Tencent, or iQiyi, increasingly with substantial IP-financing budgets behind them — have been recruiting mid-career Japanese key animators and animation directors aggressively since the late 2010s. Studios such as Colored Pencil Animation and Studio LAN have made no secret of hiring Japanese talent and paying multiples of Japanese rates for equivalent work.

Korean studios linked to Kakao Entertainment and Naver Webtoon — particularly those building animation pipelines around the global webtoon-IP boom — have followed a similar playbook, sometimes paying senior Japanese genga two to four times the Japanese piece rate for remote contract work. Netflix and other Western platforms have, on selective projects, bid directly for top-tier senior talent. The result is the two-tier outcome economists predict but the Japanese industry has not yet structurally adapted to: the most capable senior animators have outside options; the entry-level in-between animator still has the convenience-store onigiri.

The signals of improvement

It would be wrong to leave the picture there. There are studios doing it differently, and the gap between them and the median is widening — which is itself useful information for any foreign partner choosing a counterparty.

ufotable, the studio behind Demon Slayer: Kimetsu no Yaiba, is the most-cited example. Its participation in the production committee meant the studio captured equity-like upside when the film became, briefly, the highest-grossing Japanese film in history. Tax disclosures suggest the studio’s financial position transformed; reporting on staff compensation, while less transparent, suggests material improvement above the industry baseline.

MAPPA has pursued mixed self-financing on select titles, taking on the producer role and risk — a model that, when the title hits, lets the studio retain upside it would otherwise have signed away. Kyoto Animation has, for two decades, run a salaried-employee model with above-industry pay and on-site training. Smaller studios such as Science SARU and Trigger have experimented with co-production and minority IP stakes that, while not transformative, point in the right direction.

On the policy side, the Agency for Cultural Affairs has funded the Anime Mirai / Project Anime training program since 2010 to subsidize apprenticeship-style training at participating studios. METI has paid intermittent attention to the industry’s labor conditions as a soft-power policy concern. JAniCA itself has become a more vocal advocate. Each of these is incremental. None alone changes the structural picture. Collectively, they signal that labor conditions are now visible enough that they are no longer purely internal.

What a foreign partner should ask before signing

For a streaming platform commissioning a multi-season original, a publisher licensing an adaptation, or an investor underwriting an anime-adjacent fund, labor conditions at the studio counterparty are no longer a soft consideration. They are an ESG signal, a delivery-risk signal, and increasingly a reputational one.

Practical questions worth asking your prospective studio counterparty, before signing:

- What proportion of your production staff are full-time salaried employees versus piece-rate gyōmu itaku contractors? A studio that has migrated a meaningful share of in-between and second-key animators onto salaried contracts with benefits is unusually serious about retention.

- Does the studio take an IP-equity stake in projects it produces, or operate purely on a work-for-hire production fee? Equity-taking studios have a structural mechanism through which hits translate into staff pay.

- What is your studio’s average tenure for in-between and second-key animators? Industry norm is high churn at the bottom; outliers exist.

- Do you operate formal apprenticeship or in-house training programs, including Anime Mirai / Project Anime participation?

- What is your overtime policy and how is it enforced for contract workers? The honest studios will tell you the truth.

- Is the studio willing to disclose, under NDA, aggregate compensation bands by role? Studios with healthier economics are increasingly willing to do this.

None of these questions is rude. They are the same questions a sophisticated buyer would ask of a contract manufacturer in any industry where labor risk has become a board-level topic. The studios that answer confidently are the ones you want as long-term counterparties.

The capacity question

There is a final, harder question lurking underneath all of this, which the industry has not collectively answered: can Japan actually deliver the pipeline it has already sold?

AJA’s Anime Industry Report shows the overall market value crossing ¥3 trillion in recent years, with overseas revenue now the single largest segment. TV series volume, streaming-platform original commissions, the feature-film slate, and late-stage work for foreign-financed projects have all grown faster than the workforce. Studios are turning down work. Episodes are already subcontracted to studios in China, the Philippines, Vietnam, and South Korea — sometimes by Japanese studios that publicly badge the work as Japanese. The pipeline producing the next generation of senior animators starts at the in-between desk in Nerima, and that desk is leaking workers fastest.

If the wages at that desk do not rise, the medium-term capacity of the industry will not rise either, and the global anime boom that the production committees, streamers, and licensors have spent the past decade building risks running into a wall that is made not of demand but of fingers on pencils. That is the labor crisis. That is the business story. And that is why the day in Nerima matters to anyone, anywhere, who is selling Japanese animation to the rest of the world.

Frequently Asked Questions

What does an entry-level anime animator in Japan actually earn?

JAniCA labor surveys and industry reporting consistently put in-between animators (the entry tier) at roughly ¥1.5–2.5 million per year in their first one to three years, typically on piece-rate contracts of around ¥200 per finished in-between drawing. This is well below the all-Japan median income and is the principal driver of high attrition at the bottom of the craft ladder.

Why are anime wages so low when the industry is so successful globally?

The dominant production-committee financing model means that the studio that animates a show is structurally a labor contractor inside a financing consortium. The studio rarely owns equity in the IP it produces, so when a show becomes a global hit, the upside flows to publishers, broadcasters, music labels, and distributors — not to the studio, and not to the animator. Without an IP-equity pathway, hits do not translate into wage growth at the desk.

Are Chinese and Korean studios really hiring Japanese animators away?

Yes, particularly at the senior key-animator and animation-director level. Chinese studios linked to Bilibili, Tencent, and iQiyi have been recruiting Japanese talent since the late 2010s, often at two to four times Japanese piece-rates. Korean studios connected to Kakao Entertainment and Naver Webtoon have followed a similar pattern. The entry tier in Japan is less mobile, but the mid-career and senior tiers increasingly have outside options.

Which Japanese studios are known for treating staff better than average?

The most commonly cited examples are ufotable (which took an equity-like position in Demon Slayer), MAPPA (which has pursued mixed self-financing on select titles), and Kyoto Animation (which has long operated a salaried-employee model with above-industry pay). Science SARU and Trigger are smaller examples of co-production-and-equity experimentation. These are outliers rather than the industry norm.

What should a foreign company commissioning anime ask about labor conditions?

Practical questions include the share of salaried versus piece-rate staff, whether the studio takes IP-equity stakes, average tenure at the in-between and second-key levels, participation in Anime Mirai / Project Anime training programs, overtime policy and enforcement, and willingness to disclose aggregate compensation bands under NDA. Studios with healthier economics typically answer these confidently; studios that deflect are signaling something useful.

Sourcing or commissioning from Japanese animation studios? Japonity helps foreign partners diligence and select Japanese studio counterparties on financial, creative, and labor-condition criteria. Reach out via our business-matching service for a discreet introduction.

More from Japonity’s Japan Anime Business series

This article is part of a 10-piece editorial cluster on the business of Japanese anime. Read the rest:

- Inside Japan’s Anime Production Committee — How the money and rights really flow inside the joint-venture structure that funds almost every Japanese TV anime.

- Japan’s Anime Export Boom — Why overseas anime sales topped ¥1.7 trillion and overtook domestic for the first time in 2023.

- The 10 Anime Studios Behind 80% of Output — A ranked, opinionated business map of the studios that dominate foreign-licensed Japanese animation.

- Licensing Anime IP: A 2026 Foreign Buyer’s Guide — Why Western licensing instincts produce wrong answers in Japan, and the eight-stage flow that actually closes deals.

- The New Geography of Anime Streaming — Crunchyroll, Bilibili, Netflix, Disney+ and others split the world by region, rights and business model.

- Why Akihabara Still Matters — Behind the neon, Tokyo’s Akihabara is a working B2B test market for anime IP — a foreign buyer’s walking tour.

- VTuber Economics — Inside the billion-dollar virtual influencer industry built by Cover (Hololive) and ANYCOLOR (Nijisanji).

- The Anime Merchandise Pipeline — From Tokyo factories to Comic-Con booths — how an anime figure actually travels to a foreign retail shelf.

- Japan’s Trillion-Yen Manga Industry — Inside a publishing business larger than anime — and the four Tokyo houses every foreign publisher should know.

Sourcing beyond anime? Japonity also runs a Japan Sourcing Hub — a research-grade catalogue of 1,185 verified Japanese food products and 200+ overseas EC stores that already stock them, with HS codes, certifications and supplier MOQs ready for B2B procurement.

Interested in Japanese business opportunities?

Whether you're looking for technology partners, engineering talent, or market insights — we can help connect you with the right Japanese organizations.

Get in Touch →