Japan’s manga market — print, digital, and app — is now estimated at over ¥6.9 trillion in recent peak years, making it larger than the country’s anime business by revenue and one of the most valuable intellectual-property pipelines in global media. Yet most foreign rights buyers, librarians, and retailers still treat manga as a category that runs downstream of Tokyo’s anime studios. That gets the causality backwards. The studios animate what the publishers already proved. To understand where the next decade of Japanese content licensing is heading, foreigners need to understand the publishers, the magazines, and the apps that sit on top of the IP — not the screens that come at the end.

The headline numbers

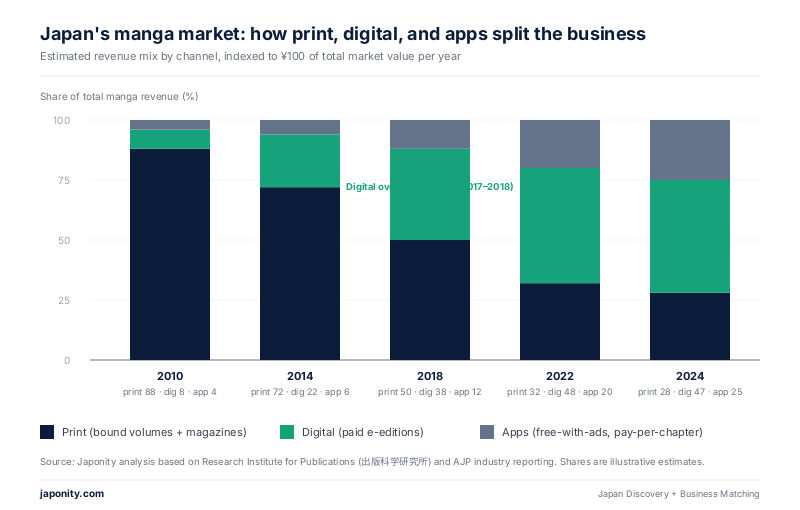

Industry estimates compiled by the Research Institute for Publications (出版科学研究所) and the All Japan Magazine and Book Publisher’s and Editor’s Association (AJP) put the total Japanese manga market — bound print volumes, magazines, paid digital editions, and app-based reading combined — at roughly ¥6.9 trillion across peak post-pandemic years. That figure has held remarkably steady. Manga alone now generates more annual revenue inside Japan than the country’s domestically reported anime production business by a wide margin, before any of the merchandise, games, theme-park, or character-licensing layers that sit on top of the IP.

The composition is what has changed. Print manga peaked in volume sales in the mid-1990s, declined for two decades, and was overtaken by digital revenue around 2017–2018. By the early 2020s digital had moved from roughly a quarter of total manga sales to well over half. Today digital — primarily app-based reading on smartphones — accounts for the majority of the market by yen, with paid print sales stabilizing rather than collapsing, and a third bucket of “free with ads / pay-per-chapter” app revenue growing fastest of all. The story is not print’s death. It is digital’s arrival as the dominant channel while print holds a premium collector role.

The Big Four publishers

The Japanese manga industry is unusually concentrated. Four publishing houses, all headquartered within a few kilometers of each other in central Tokyo, generate the overwhelming majority of the IP that becomes anime, live-action drama, film, mobile games, merchandise, and theme-park attractions. None of them are listed companies in the way Disney or Warner Bros. are. Three are privately held media conglomerates with century-long histories. One — Kadokawa — is publicly traded and structurally different.

| Publisher | Founded | Flagship magazine | Best-known IPs | Ownership |

|---|---|---|---|---|

| Shueisha (集英社) | 1926 | Weekly Shonen Jump | One Piece, Dragon Ball, Naruto, Demon Slayer, My Hero Academia, Jujutsu Kaisen | Private (Hitotsubashi Group) |

| Kodansha (講談社) | 1909 | Weekly Shonen Magazine | Attack on Titan, Fairy Tail, Vinland Saga, Blue Lock, Tokyo Revengers | Private (Otowa family) |

| Shogakukan (小学館) | 1922 | Weekly Shonen Sunday | Detective Conan, Doraemon, Inuyasha, Frieren, Pokémon Adventures | Private (Hitotsubashi Group) |

| Kadokawa (KADOKAWA) | 1945 | Comp Ace, Dengeki Daioh, light-novel imprints | Re:Zero, Sword Art Online, Overlord, KonoSuba, Spice and Wolf | Public (TYO: 9468) |

Shueisha and Shogakukan together form the Hitotsubashi Group, a privately controlled publishing cluster that also owns half of VIZ Media in the United States. Kodansha sits separately under the Otowa family and operates Kodansha USA. Kadokawa, the youngest of the four, is the publicly traded outlier — a roll-up of light-novel imprints, manga magazines, the Niconico video platform, FromSoftware (Elden Ring), and a long list of anime production credits. Foreign buyers approaching Japanese rights for the first time often assume the publishers compete on titles alone. In practice they compete on magazine pipelines, animation committee seats, and overseas joint ventures.

The digital revolution

For most of manga’s history, the magazine was the discovery engine and the bound paperback (tankōbon) was the revenue engine. A reader bought Weekly Shonen Jump for ¥300, read twenty serialized chapters, and then bought the ¥500 collected volumes of their favorite series months later. That cycle is now half-dismantled. Magazine circulation has fallen by roughly two-thirds from its 1995 peak. The discovery layer has migrated almost entirely to apps.

Three platforms dominate. Piccoma, run by Kakao Japan, has been Japan’s highest-grossing comics app for several consecutive years, built on a “wait or pay” model that gives readers one free chapter per series per day and charges for the rest. LINE Manga, operated by LY Corporation (the LINE-Yahoo Japan merger), uses a similar model and rivals Piccoma in monthly active users. Both surface a heavy share of Korean webtoons alongside Japanese manga. Manga Plus, Shueisha’s own free global service launched in 2019, takes a different approach: it gives non-Japanese readers the first and most recent chapters of Shueisha series for free, the same day as Japan, in multiple languages — partly as anti-piracy, partly as a global discovery funnel for the broader VIZ rights business.

What changed economically is not just channel. It is unit economics. A bound tankōbon at ¥500 generates a one-time transaction. An app reader who pays ¥100 per chapter across a 100-chapter series, plus tipping and bundle purchases, can be worth several times more in lifetime revenue. This is why the Big Four publishers tolerate — and quietly profit from — apps that, on the surface, seem to cannibalize their print business.

The Korean webtoons question

The most disruptive competitive force in Japanese manga today is not domestic. It is the Korean webtoon — vertical-scroll, full-color comics designed natively for smartphones, produced under studio systems closer to anime production than to traditional manga editorial. Naver Webtoon (parent of LINE Manga’s Korean side) and Kakao (parent of Piccoma) have spent the past five years pouring webtoon content into the Japanese market, and Japanese readers have responded. Korean studios such as Solo Leveling’s DUBU and Redice Studio have crossed over into mainstream Japanese readership; Solo Leveling itself was animated by Tokyo’s A-1 Pictures and became one of the highest-grossing anime adaptations of 2024–2025.

The Japanese publishers’ response has been pragmatic rather than defensive. Shueisha, Kodansha, and Shogakukan have all launched vertical-scroll color imprints. Kadokawa has invested directly in webtoon production. The format is not replacing manga — black-and-white right-to-left paginated manga remains the dominant form, and many of the highest-grossing series of 2024–2025 are still in that format — but the publishers now treat color vertical-scroll as a parallel product line aimed at smartphone-first readers who do not have a built-in habit of reading pages.

The rights pipeline: how a manga becomes everything else

The single most important fact about Japanese manga, for any foreign rights buyer, is that it is the upstream of nearly every other Japanese content category. The path is well-worn. A manga is serialized in a weekly or monthly magazine. If reader-survey rankings hold up for six months, the bound volume is published. If the bound volume sells past roughly half a million copies, an “anime production committee” (製作委員会) is convened — typically including the publisher, an animation studio, a TV broadcaster, a music label, a toy maker, and one or two streaming or merchandising partners. The committee co-funds the anime, owns the rights collectively, and distributes profits proportionally.

This is why Shueisha appears on the credit lists of dozens of anime that, on the surface, look like they were made by studios. They were made by studios. But the IP, the editorial direction, the merchandise approval, and a substantial cut of the upside flow through the publisher. For foreign streamers, distributors, and licensees, this means the meaningful negotiation almost always begins at the publisher level, not the studio level — and that the Big Four’s overseas arms are the gate.

International rights and the overseas arms

Each major publisher operates an English-language rights and distribution business that has matured significantly over the past decade. VIZ Media, headquartered in San Francisco, is jointly owned by Shueisha and Shogakukan and handles English print, digital, and home-video rights for the Hitotsubashi Group’s biggest series — One Piece, Naruto, Demon Slayer, Detective Conan, and hundreds of others. Kodansha USA publishes English editions of Attack on Titan, Blue Lock, and the rest of Kodansha’s catalog directly. Yen Press, owned by Kadokawa and Hachette Book Group, is the largest English-language light-novel publisher and a growing manga player. Seven Seas Entertainment, independent, has built a strong mid-list niche, particularly in isekai and slice-of-life. Together with smaller players (Tokyopop, Square Enix Manga, Denpa, Vertical), these houses move the substantial majority of officially licensed Japanese manga into the English-speaking world.

North American manga retail sales tracked by Circana BookScan have grown several-fold since 2019 and now represent the largest single category of adult graphic novels in U.S. bookstores by unit volume. Demon Slayer, Jujutsu Kaisen, and Chainsaw Man each repeatedly outsold the top-selling American superhero titles in any given week through 2023–2024. The format that U.S. publishers spent two decades treating as a niche import is now the engine of the graphic-novel shelf.

What it means for foreign rights buyers, retailers, and investors

Three implications follow. First, for foreign publishers and rights buyers: meaningful Japanese-IP deals are concentrated. Four houses control the upstream, and three Western joint ventures (VIZ, Kodansha USA, Yen Press) handle the largest share of the downstream. Cold-approaching a Tokyo editor at a Big Four house is harder than approaching a New York agent; the conventional entry points are Anime NYC, the Tokyo International Book Fair (TIBF), Frankfurt Book Fair’s Asian rights floor, and Bologna for children’s titles. Second, for retailers: manga shelf space is no longer a niche bet, and the unit economics — high frequency of new volume releases, strong series-loyalty, low return rates — make it one of the better-performing categories in trade publishing. Third, for investors: only Kadokawa among the Big Four is directly investable on public markets; exposure to Shueisha and Shogakukan flows through licensees, animation studios (Toho, IG Port), and platform operators (LY Corporation, Kakao).

2026 outlook

Three vectors will shape the next two years. AI-assisted translation is collapsing the cost of bringing mid-list titles to English and other languages. Shueisha and Shogakukan have publicly partnered on machine-translation pilots; smaller publishers are following. The risk is editorial quality; the opportunity is a long tail of mid-list series that were previously uneconomic to license. IP licensing beyond anime and live-action — into mobile games, Hollywood adaptations (One Piece on Netflix, Cowboy Bebop, ongoing Akira and Ghost in the Shell rights deals) — continues to expand the per-title lifetime value of the strongest franchises. Market saturation is the genuine risk: the number of serialized titles being launched annually across the Big Four has grown faster than reader attention, and platform competition with webtoons is squeezing creator economics. The trillion-yen number will hold. The question is which publishers, and which formats, capture the next decade of growth.

FAQ

How big is Japan’s manga industry?

Recent industry estimates from the Research Institute for Publications and AJP put the combined Japanese manga market — print volumes, magazines, paid digital editions, and app-based reading — at roughly ¥6.9 trillion in peak post-pandemic years. Digital now accounts for the majority of revenue, with app-based reading the fastest-growing segment.

When did digital manga overtake print?

Digital manga revenue passed print revenue in Japan around 2017–2018. The crossover was driven primarily by smartphone reading apps — Piccoma, LINE Manga, and the publishers’ own platforms — rather than by e-readers or PC reading. Print sales have since stabilized rather than collapsed, but digital is now the larger channel by yen.

Who are the major Japanese manga publishers?

Four publishers dominate: Shueisha (Weekly Shonen Jump — One Piece, Demon Slayer, Jujutsu Kaisen), Kodansha (Weekly Shonen Magazine — Attack on Titan, Blue Lock), Shogakukan (Weekly Shonen Sunday — Detective Conan, Frieren), and Kadokawa (light novels and manga — Re:Zero, Sword Art Online). The first three are privately held; Kadokawa is publicly traded on the Tokyo Stock Exchange.

How does a manga become an anime?

The standard path runs through the publisher. A serialized manga that performs well in reader rankings and bound-volume sales triggers the formation of an “anime production committee” (製作委員会) — typically including the publisher, an animation studio, a broadcaster, a music label, and toy and streaming partners. The committee co-funds production and collectively owns rights, with the publisher retaining substantial editorial and licensing control.

How do foreign publishers license Japanese manga?

Most English-language manga rights flow through three publisher-affiliated arms: VIZ Media (Shueisha + Shogakukan joint venture), Kodansha USA, and Yen Press (Kadokawa). These houses handle the bulk of officially licensed English editions. Industry trade events such as Anime NYC, the Tokyo International Book Fair, Frankfurt’s Asian rights floor, and Bologna for children’s titles are the conventional starting points for new rights relationships.

Looking to connect with Japanese manga publishers, licensors, or rights agents? Japonity’s business-matching service introduces foreign buyers, retailers, and investors to vetted Japanese partners across publishing, IP licensing, and content distribution.

More from Japonity’s Japan Anime Business series

This article is part of a 10-piece editorial cluster on the business of Japanese anime. Read the rest:

- Inside Japan’s Anime Production Committee — How the money and rights really flow inside the joint-venture structure that funds almost every Japanese TV anime.

- Japan’s Anime Export Boom — Why overseas anime sales topped ¥1.7 trillion and overtook domestic for the first time in 2023.

- The 10 Anime Studios Behind 80% of Output — A ranked, opinionated business map of the studios that dominate foreign-licensed Japanese animation.

- Licensing Anime IP: A 2026 Foreign Buyer’s Guide — Why Western licensing instincts produce wrong answers in Japan, and the eight-stage flow that actually closes deals.

- The New Geography of Anime Streaming — Crunchyroll, Bilibili, Netflix, Disney+ and others split the world by region, rights and business model.

- Why Akihabara Still Matters — Behind the neon, Tokyo’s Akihabara is a working B2B test market for anime IP — a foreign buyer’s walking tour.

- VTuber Economics — Inside the billion-dollar virtual influencer industry built by Cover (Hololive) and ANYCOLOR (Nijisanji).

- The Anime Merchandise Pipeline — From Tokyo factories to Comic-Con booths — how an anime figure actually travels to a foreign retail shelf.

- A Day in the Life of an Anime Animator — Inside the working day of a rank-and-file animator, and the structural reasons wages stay low across the industry.

Sourcing beyond anime? Japonity also runs a Japan Sourcing Hub — a research-grade catalogue of 1,185 verified Japanese food products and 200+ overseas EC stores that already stock them, with HS codes, certifications and supplier MOQs ready for B2B procurement.

Interested in Japanese business opportunities?

Whether you're looking for technology partners, engineering talent, or market insights — we can help connect you with the right Japanese organizations.

Get in Touch →