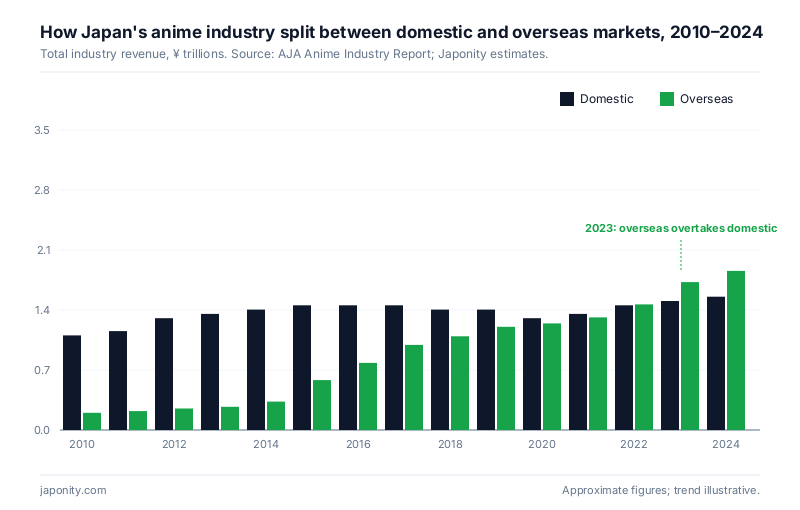

In 2023 — for the first time in the history of Japan’s animation industry — foreign markets out-earned domestic ones. According to the Association of Japanese Animations (AJA) Anime Industry Report, the industry’s total revenue reached roughly ¥3.3 trillion, with overseas sales pushing past ¥1.7 trillion. That crossover is not a one-year quirk: it is the structural punchline of a fifteen-year compounding story that Japan’s own Ministry of Economy, Trade and Industry (METI) has been slow to internalise. For overseas importers, licensors, retailers and investors, the implication is simple. Anime is no longer a cultural curio attached to a domestic business; it is one of Japan’s fastest-growing service exports, and the window to enter on workable terms is narrowing.

The headline numbers, sober and slow

The AJA’s annual report is the canonical industry data set, compiled from production committees, distributors, licensees and platform operators. Its most recent edition pegs the broad industry — production, broadcast, streaming, merchandise, music, theatrical, live events, gaming tie-ins — at approximately ¥3.3 trillion (around US$22 billion at recent exchange rates). Inside that headline, two facts deserve to be lifted out.

First, the overseas component grew from under ¥250 billion in 2010 to over ¥1.7 trillion in 2023 — roughly a sevenfold increase in a span when domestic revenue grew by perhaps 30 to 40 per cent. Second, the crossover year was 2023: foreign sales surpassed domestic sales, and the 2024 figures suggest the gap is widening rather than closing.

METI’s Cool Japan data and JETRO trade statistics, while less granular than AJA’s, corroborate the trend. In METI’s tracking of “content” service exports, animation and related IP have been the single fastest-growing sub-category over the past decade — outpacing music, publishing and game software by a comfortable margin. The implication is that anime is now contributing meaningfully to Japan’s invisible trade balance at precisely the moment its goods trade balance is under structural strain.

What is actually being exported: the four buckets

“Anime exports” is a useful shorthand and a misleading one. The trillion-yen-plus overseas figure aggregates four distinct businesses with different margins, buyers and growth dynamics. Understanding the mix is the first thing a foreign company entering the market needs to do.

| Export bucket | Approx. share of overseas revenue | Primary growth driver |

|---|---|---|

| Streaming & broadcast licensing | ~50–55% | Crunchyroll, Netflix, Disney+, Amazon, regional platforms bidding for simulcast rights |

| Merchandise & character licensing | ~25–30% | Figures, apparel, collectibles, café/pop-up retail in North America and SE Asia |

| Theatrical (cinema box office) | ~10–12% | Tentpole feature releases (Demon Slayer, Jujutsu Kaisen, Suzume, Ghibli reissues) |

| Music, live events & other | ~5–8% | Concert tours, soundtrack streaming, IP licensing into games and theme parks |

Streaming licensing is the engine. The Sony Pictures acquisition of Crunchyroll from AT&T for US$1.175 billion in 2021 was the moment the streaming bucket consolidated into something legible to global capital: a single English-language platform with over 100 million registered users and exclusive simulcast rights on the majority of new seasonal titles. Netflix, for its part, has more than doubled its anime production and licensing budget since 2019, commissioning original series and securing global windows on theatrical releases.

Merchandise is the second engine, and a structurally higher-margin one. Bandai Namco, Good Smile Company and Kotobukiya have moved from export-led distribution to direct retail in North America, with brick-and-mortar pop-ups in Los Angeles, New York and Texas now generating sustained revenue rather than one-off marketing spend.

The geography of demand: not what it was five years ago

The most consequential shift inside the overseas figure is geographic. As recently as 2019, China was the single largest overseas market for Japanese anime by licensing value, driven by Bilibili, iQiyi and Tencent Video competing aggressively for streaming rights. That has changed.

- North America surge. The United States and Canada combined are now the largest single regional market, accounting for an estimated 40–45 per cent of overseas revenue. Crunchyroll’s subscriber base, Netflix’s investment and the maturation of theatrical distribution (Demon Slayer: Mugen Train grossed over ¥40 billion globally, with North America its largest non-Japanese market) have converged into a durable demand base.

- China cooling. Beijing’s tightening of foreign content quotas, the National Radio and Television Administration’s scrutiny of Japanese IP, and a domestic preference for state-supported Chinese animation have compressed the China share from roughly a third of overseas revenue in 2019 to perhaps 15–20 per cent today. Industry estimates suggest the absolute Chinese figure has stagnated or declined modestly even as the global pie grew.

- Southeast Asia and the Middle East rising. Indonesia, the Philippines, Thailand and Vietnam — populous, young, smartphone-native markets — are the fastest-growing regional bloc, though from a low base. The Middle East, particularly Saudi Arabia (where the Public Investment Fund has taken anime-adjacent positions through Savvy Games and Manga Productions) and the UAE, is the surprise of the last 24 months.

- Europe steady. France remains the largest single European market — a structural legacy of Goldorak and Club Dorothée in the 1980s — with Germany, Italy and Spain meaningful but slower-growing.

Why this happened: four structural drivers

The temptation is to attribute the boom to a single hit — Demon Slayer, Attack on Titan, Jujutsu Kaisen. That underweights the structural shifts beneath the hits.

- Streaming consolidation. A decade ago, anime overseas was a long tail of regional licensors, fan-subbing communities and physical disc distribution. Today, three to four global platforms (Crunchyroll, Netflix, Disney+, Amazon) compete for content, which compresses negotiation cycles and raises licence values. Japanese production committees can now sell a single global window rather than negotiating territory by territory.

- IP-owning studios learning to operate. Studios that historically sold rights cheaply to broadcasters are now retaining IP equity through production committee restructuring and direct platform deals. Studio MAPPA’s choice to self-finance season four of Attack on Titan was emblematic; Toho, Aniplex and Kadokawa have built integrated production-to-distribution capability.

- Dub/sub speed-up. Localisation latency has collapsed from months to days. Simulcast subbing is now standard, and major titles ship with dubs in eight to twelve languages within weeks of Japanese broadcast. The customer experience overseas now approximates the domestic one — a precondition for converting casual viewers to paying subscribers.

- Tentpole hit cadence. The industry has produced a globally legible blockbuster roughly every 12 to 18 months since 2019. That is not luck; it is a function of larger budgets, longer production cycles and global marketing coordination through Sony, Toho and Aniplex’s overseas arms.

What this means for a foreign company entering now

The trade data alters the calculus for any overseas firm considering exposure to Japanese animation IP. Five implications are concrete.

- Licensing terms have hardened. The seller-of-last-resort posture that characterised Japanese rights holders into the mid-2010s is gone. Minimum guarantees, output deals and exclusivity premiums are now standard, and inbound enquiries with no comparable transaction track record are routinely declined. Foreign buyers need a credible reference deal — even a small one — to be taken seriously.

- Merchandise is the open lane. Streaming rights are consolidated among a handful of buyers, but physical merchandise, regional theatrical, theme-park experiences, food and beverage tie-ups and apparel collaborations remain fragmented and accessible to mid-sized foreign partners.

- Production committees still gate everything. Most major IP is owned by a production committee (seisaku iinkai) of five to ten Japanese entities — a publisher, a broadcaster, a studio, a music label, a distributor, sometimes an ad agency. Foreign companies that try to negotiate with the studio alone discover, often expensively, that the studio cannot bind the committee. Identifying the committee chair and the rights coordinator is the first work.

- Tokyo presence is no longer optional for serious players. Sony, Netflix and Crunchyroll all expanded Tokyo headcount aggressively post-2021. The deals get done in Roppongi, Shibuya and Iidabashi conference rooms; flying in for AnimeJapan once a year is not enough.

- The yen is doing some of the work. At ¥150-plus to the dollar, Japanese IP looks structurally underpriced to foreign buyers measured in their home currency. That is a tailwind, but it is also a window that will close if monetary policy normalises.

The risks that the headline numbers obscure

A trade-data piece that only narrates upside is suspect. Four risks deserve foreign buyers’ attention.

China policy risk. The Chinese share has compressed but has not gone to zero, and a meaningful reversal — either toward openness or toward an outright ban on new Japanese titles — would move the global market. The base case is continued managed contraction.

Exchange rate risk in reverse. A sharp yen appreciation would compress overseas revenue measured in yen and could make Japanese IP look expensive to dollar- and euro-denominated buyers who locked in deals at weaker yen.

Talent crisis. The animator labour market in Japan is genuinely under strain. Median in-betweener wages remain low by developed-market standards, the workforce is ageing, and key animation outsourcing has shifted to Korea, Vietnam and the Philippines. The industry’s ability to sustain a tentpole-every-18-months cadence depends on resolving this, and the resolution is not in sight.

IP fragmentation. The production committee structure that protects Japanese partners’ downside also slows decision-making and creates the recurring foreign-buyer complaint: “Who actually owns this title and can sign?” Until ownership concentrates — and there is no obvious mechanism to force that — transaction friction will remain a tax on the industry’s overseas growth.

2026–2030 outlook

Industry estimates and METI projections converge on a relatively narrow range. Total industry revenue is likely to reach ¥4 trillion by 2027 and possibly ¥4.5–5 trillion by 2030, with overseas approaching 60 per cent of the total. North America’s share will likely grow further, Southeast Asia will close the gap with Europe, and the Middle East may surprise on the upside if Saudi and Emirati sovereign capital continues to deploy. The question is not whether anime exports keep growing — they will — but who captures the margin. The current answer is: increasingly, the platforms (Sony/Crunchyroll and Netflix) and the IP owners (Toho, Aniplex, Kadokawa, Shueisha), and decreasingly the studios that do the actual animation work. That is a structural imbalance that will, eventually, force a reckoning.

Frequently asked questions

How big is Japan’s anime export market in 2026?

Based on the AJA Anime Industry Report and METI data, overseas anime revenue exceeded ¥1.7 trillion in 2023 and is on a trajectory to surpass ¥2 trillion in 2026. Total industry revenue, including domestic, is approximately ¥3.3–3.5 trillion. Foreign sales now represent more than half of the industry total.

When did overseas anime revenue overtake domestic?

2023, according to the AJA Anime Industry Report. It is the first crossover in the industry’s recorded history and reflects roughly fifteen years of compounding overseas growth alongside relatively flat domestic revenue.

Which countries are the biggest buyers of Japanese anime?

The United States is now the single largest overseas market, followed by China (declining), then a cluster of European markets led by France. Southeast Asian markets — Indonesia, the Philippines, Thailand, Vietnam — are the fastest-growing region, with the Middle East emerging rapidly from a smaller base.

What is the AJA Anime Industry Report?

An annual industry data publication by the Association of Japanese Animations covering production volume, revenue by segment (streaming, merchandise, theatrical, music, live events), overseas sales and employment. It is the most authoritative quantitative source on the Japanese animation industry and is widely cited by METI, JETRO and global analysts.

How can a foreign company enter the Japanese anime business?

The accessible entry points are merchandise and licensing partnerships, regional theatrical and live-event distribution, and brand collaborations. Streaming rights are consolidated among a few global platforms and are difficult for new entrants. A credible reference transaction, a Tokyo presence and an understanding of the production committee structure are the practical prerequisites — and where Japonity’s business-matching desk typically supports overseas buyers.

If your firm is evaluating Japanese anime IP, merchandise rights or licensing partnerships, Japonity’s editorial and business-matching teams introduce qualified overseas buyers to vetted Japanese rights holders. Contact our business-matching desk to begin.

More from Japonity’s Japan Anime Business series

This article is part of a 10-piece editorial cluster on the business of Japanese anime. Read the rest:

- Inside Japan’s Anime Production Committee — How the money and rights really flow inside the joint-venture structure that funds almost every Japanese TV anime.

- The 10 Anime Studios Behind 80% of Output — A ranked, opinionated business map of the studios that dominate foreign-licensed Japanese animation.

- Licensing Anime IP: A 2026 Foreign Buyer’s Guide — Why Western licensing instincts produce wrong answers in Japan, and the eight-stage flow that actually closes deals.

- The New Geography of Anime Streaming — Crunchyroll, Bilibili, Netflix, Disney+ and others split the world by region, rights and business model.

- Why Akihabara Still Matters — Behind the neon, Tokyo’s Akihabara is a working B2B test market for anime IP — a foreign buyer’s walking tour.

- VTuber Economics — Inside the billion-dollar virtual influencer industry built by Cover (Hololive) and ANYCOLOR (Nijisanji).

- The Anime Merchandise Pipeline — From Tokyo factories to Comic-Con booths — how an anime figure actually travels to a foreign retail shelf.

- Japan’s Trillion-Yen Manga Industry — Inside a publishing business larger than anime — and the four Tokyo houses every foreign publisher should know.

- A Day in the Life of an Anime Animator — Inside the working day of a rank-and-file animator, and the structural reasons wages stay low across the industry.

Sourcing beyond anime? Japonity also runs a Japan Sourcing Hub — a research-grade catalogue of 1,185 verified Japanese food products and 200+ overseas EC stores that already stock them, with HS codes, certifications and supplier MOQs ready for B2B procurement.

Interested in Japanese business opportunities?

Whether you're looking for technology partners, engineering talent, or market insights — we can help connect you with the right Japanese organizations.

Get in Touch →