In April 2021, AT&T sold Crunchyroll to Sony for $1.175 billion. By March 2022, Sony had quietly folded Funimation — its prior anime asset — into the Crunchyroll brand, ending what had been a two-decade rivalry between the two largest licensors of Japanese animation outside Asia. The deal received modest press coverage at the time. In hindsight, it may rank as one of the most consequential vertical-integration moves in global streaming. Sony now owns major anime production studios in Japan (Aniplex, A-1 Pictures), the dominant Western anime distribution platform (Crunchyroll), the world’s number-two music label (Sony Music), and the PlayStation gaming ecosystem where many anime IPs are monetised in adjacent forms. Meanwhile, in China — a market closed to Crunchyroll, Netflix, and Disney+ alike — Bilibili sits on a near-monopoly of legally licensed Japanese anime, with over 300 million monthly active users and an increasingly visible appetite to push outside its home market. The geography of anime streaming is no longer a long tail. It is a five-platform contest with real strategic stakes, and the lines on the map matter more than the average Western viewer realises.

The five-platform landscape today

Crunchyroll (Sony). The dominant Western anime-specialist service, with publicly reported subscribers above 15 million as of late 2024 and growth trajectory that, according to trade press including Variety and The Hollywood Reporter, has continued through 2025. After absorbing Funimation in 2022, Crunchyroll consolidated the simulcast pipeline — the rapid licensed streaming of new anime episodes within hours of their Japanese broadcast — into a single platform. Its strategic moat is not just catalogue but production proximity: Sony’s stake in Japanese studios means Crunchyroll often gets first-look or exclusive Western rights on shows Sony’s own studios produce.

Netflix. The largest streamer overall, with anime treated as a strategic genre rather than core. Netflix’s anime catalogue includes more than 80 originals commissioned or co-produced since 2017, with partnerships with WIT Studio (the team behind Attack on Titan‘s early seasons), Bones, Production I.G., and Studio Colorido (acquired in part via deals in 2020–2022). Netflix’s pitch to consumers is breadth — anime as one tab in a global library — and its commissioning thesis is that high-budget original anime travels exceptionally well across non-Japanese markets.

Bilibili. Founded in 2009 as a Chinese ACG (anime, comics, games) community in the danmaku (scrolling-comment) tradition, Bilibili IPO’d on Nasdaq in 2018 and secondary-listed in Hong Kong in 2021. It holds the lion’s share of legally licensed Japanese anime distribution rights in mainland China and operates an advertising, premium subscription, and live-streaming model layered on a user community. With Crunchyroll, Netflix, and Disney+ effectively absent from mainland China, Bilibili’s competitive set is iQiyi and Tencent Video — both substantially smaller in anime-specific share.

Disney+. The newest serious anime player. Disney inherited Twentieth Century-era Japanese co-production rights through its 2019 Fox acquisition and has built an anime initiative led from Disney+ Asia Pacific, with simulcast deals on titles including Tokyo Revengers seasons, Bleach: Thousand-Year Blood War, and Summer Time Rendering. Disney+’s leverage is its Asian distribution footprint — particularly Disney+ Hotstar across Southeast Asia and India — and its willingness to use anime as a subscriber-acquisition lever in markets where Marvel and Star Wars travel less reliably.

Amazon Prime Video. A regional rather than global anime force. Amazon’s most significant anime investments are in Japan itself, where Prime Video has acquired Japanese-language exclusives, and in Australia and parts of Southeast Asia. Outside those territories, Amazon’s anime offering tends to lag the specialists.

Comparison: the five platforms at a glance

| Platform | Owner | Strategy | Anime library (approx) | Strongest regions | Subscriber price band |

|---|---|---|---|---|---|

| Crunchyroll | Sony | Vertically integrated anime specialist | 1,500+ titles | North America, parts of Europe, Latin America (growing) | $7.99–14.99 / mo |

| Netflix | Netflix Inc. | Anime as premium genre within global SVOD | ~350+ titles (incl. 80+ originals) | Western Europe, MENA, Latin America | $6.99–22.99 / mo |

| Bilibili | Bilibili Inc. | China-domestic ACG community + licensed anime | 3,000+ titles (China catalogue) | Mainland China (near-monopoly) | ~CNY 25 / mo (Premium) |

| Disney+ | The Walt Disney Co. | Anime as subscriber-acquisition lever in Asia | ~120 titles | SE Asia (Hotstar), Japan, parts of Europe | $7.99–13.99 / mo |

| Amazon Prime | Amazon | Regional anime exclusives bundled into Prime | ~200 titles | Japan, Australia, parts of SE Asia | Bundled w/ Prime |

Library counts are estimates assembled from publicly available platform catalogues and trade-press reporting; exact counts vary by territory and shift quarterly as licences enter and exit.

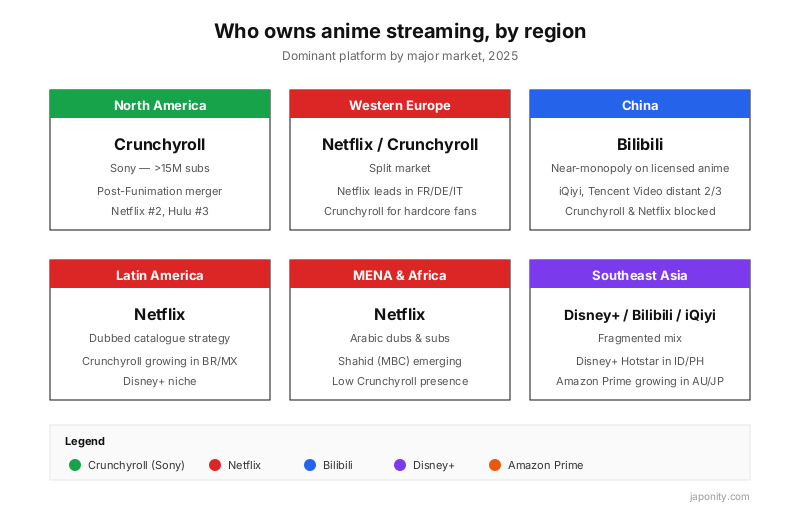

Region by region: who actually wins

North America. Crunchyroll dominates by a wide margin, and the Funimation absorption removed the only meaningful specialist competitor. Netflix is a significant number two, particularly for the broader audience attracted by tentpole originals like Devilman Crybaby, Castlevania, and Pluto. Hulu, which holds a small but loyal anime catalogue in the US, is a distant third. Disney+ has begun adding select anime titles via its tie-up with Disney+ Hotstar’s content pipeline, but the US Disney+ anime presence remains thin.

Western Europe. A genuinely split market. Netflix dominates in France, Germany, Italy, and Spain among general viewers, partly because the platform is already the default SVOD in those territories. Crunchyroll holds the hardcore anime audience and has invested aggressively in dubbing — including major French and German dub initiatives. The UK is closer to the North American pattern, with Crunchyroll the specialist of choice and Netflix the mainstream alternative.

China. Bilibili sits effectively alone. Mainland China’s regulatory environment — the requirement for content licensing through China-domiciled platforms, plus periodic content reviews by the National Radio and Television Administration — has kept Crunchyroll, Netflix, and Disney+ out. iQiyi and Tencent Video offer some licensed anime but neither has built a dedicated ACG community of Bilibili’s scale or stickiness. For Japanese rights holders, this means a single, large counterparty handles essentially all legally licensed China distribution.

Southeast Asia. The most fragmented region. Disney+ Hotstar leads in Indonesia and parts of the Philippines, partly through bundling with telco operators. Bilibili has made a meaningful push into the region via its overseas platform Bstation, particularly in Indonesia, Thailand, and Vietnam, where its free-tier model with advertising fits local payment preferences. iQiyi, Viu, and WeTV are also competitive. Netflix and Crunchyroll are present but not dominant.

MENA and Latin America. Netflix is the default in both regions, largely because of its substantial investment in Arabic and Latin American Spanish/Portuguese dubbing — both pre-existing capabilities it could redirect at anime. Crunchyroll has grown materially in Brazil and Mexico, where the anime fan base is among the most engaged in the world, but Netflix’s penetration advantage gives it the casual viewer. In MENA, Saudi Arabia’s MBC-owned Shahid has been quietly licensing more Japanese animation, but at modest scale.

The Sony / Crunchyroll vertical integration playbook

Sony’s anime position is structurally different from Netflix’s. Netflix is a buyer — it commissions or licenses anime, distributes it, and competes for attention with every other genre in its catalogue. Sony, by contrast, owns assets up and down the value chain: production (Aniplex, A-1 Pictures, and minority stakes elsewhere), publishing-adjacent monetisation (Sony Music Entertainment Japan handles a large share of anime soundtrack and theme-song releases), distribution (Crunchyroll), gaming adaptations (PlayStation Studios and Sony Pictures Television), and theatrical (Aniplex’s wholly owned theatrical-distribution subsidiary in the US, which handled the international release of Demon Slayer: Mugen Train, the highest-grossing Japanese film of all time at its 2020 release).

For the next decade, this vertical integration matters in three ways. First, Sony can run the entire monetisation chain on a single anime IP — Crunchyroll subscription, theatrical, merchandise, soundtrack, gaming tie-in — without leaking margin to external counterparties. Second, the company can use Crunchyroll’s distribution data to inform production decisions at Aniplex, closing a feedback loop Netflix can only partially replicate. Third, when Sony bids for new anime co-production rights, it can offer Japanese committee partners a more integrated deal than any pure distributor.

Where Netflix is investing

Netflix has not surrendered the genre. Quite the opposite: as reported in The Hollywood Reporter, Variety, and Animation Magazine through 2023–2025, Netflix has expanded its slate of original commissions, deepened its WIT Studio partnership, and structured production agreements with Bones, Production I.G., and David Production. Its 2020 partial-acquisition or strategic deal with Studio Colorido (the team behind A Whisker Away) gave it a feature-film anime pipeline. Netflix’s bet, in effect, is that high-budget original anime — particularly anime with feature-film production values — is where the genre’s casual audience growth will come from, and that bet is independent of who wins the simulcast catalogue race.

China: why Bilibili sits alone

For a foreign rights holder, the China question is straightforward in shape and complex in execution. Bilibili has the audience, the platform, and the regulatory standing to license a given anime for mainland distribution. Whether a given show clears China’s content review is a separate question, and historically a non-trivial share of anime — particularly those with violent, explicitly LGBTQ, or politically sensitive content — have either failed review or been edited for it. The point for a rights seller: there is one large counterparty whose interests are largely aligned with monetising Japanese animation in China, but its ability to clear a given title is constrained by factors outside its control. For investors, Bilibili’s anime business sits inside a broader monetisation engine — gaming, livestreaming, advertising — and its anime catalogue is best understood as the user-acquisition wedge for the rest.

What this means for a foreign company

For a media buyer planning a campaign. Geography is everything. A pan-European anime campaign with a single platform deal does not exist — you will be running parallel buys on Crunchyroll and Netflix at minimum. In China, Bilibili is the only meaningful single buy. In Southeast Asia, a multi-platform approach including Disney+ Hotstar and Bilibili’s Bstation is typically required to reach the audience.

For a brand picking a tie-up. If the IP is Aniplex- or A-1 Pictures-produced, you are likely negotiating through Sony’s ecosystem, which means Crunchyroll integration is the natural distribution side. If the IP is a Netflix original, the platform itself is the distribution side, and the brand opportunity tends to be a co-marketing or product-placement deal structured at commission. If the IP is older or in the long tail, multi-platform licensing remains the norm.

For an investor. The global anime streaming opportunity is best disaggregated into three sub-markets with very different competitive dynamics: the Western specialist market (Crunchyroll-dominant, with Netflix as the premium-original challenger), the Chinese domestic market (Bilibili-dominant, with regulatory ceiling), and the rest-of-world general SVOD market (Netflix-dominant, with Disney+ as the Asia-specific challenger). Each has different margin structures, growth ceilings, and exposure to Japanese production-committee dynamics.

FAQ

Is Crunchyroll really bigger than Netflix for anime?

For dedicated anime viewers in North America and parts of Europe, yes. Crunchyroll’s catalogue depth in simulcast, dub coverage, and seasonal anime is meaningfully wider than Netflix’s. For casual viewers who want a few anime titles within a broader SVOD, Netflix is often the more practical choice.

Can a Western company license anime directly to Bilibili?

Yes — Japanese production committees license to Bilibili regularly, typically through the committee’s licensing agent. A Western brand or production company licensing through a co-produced anime title would generally route the China deal through the committee structure, not directly to Bilibili.

How big is the global anime streaming market?

Estimates vary, but trade-press analyses from Variety, The Hollywood Reporter, and industry research firms have put the global anime market — streaming, merchandise, theatrical, and licensing combined — at roughly $30 billion as of recent years, with streaming the fastest-growing segment. Streaming-only revenue is a fraction of that total but the highest-growth sub-segment.

Why doesn’t Disney push harder on anime in the US?

Disney’s US strategy still leads with its core franchises — Marvel, Star Wars, Pixar — and anime is treated more as an Asian acquisition lever than a US-priority genre. The same titles available on Disney+ Asia are not always cleared for Disney+ US, partly because of pre-existing North American licence deals held by Crunchyroll or others.

Will Sony bring Aniplex titles exclusively to Crunchyroll going forward?

Increasingly yes for Western distribution, though Sony has continued selectively licensing to Netflix and other partners where the deal economics favour it. The structural direction is consolidation onto Crunchyroll; the practical pace depends on existing committee agreements and partner economics.

Mapping the partner ecosystem behind a Japanese anime, music, or media tie-up is exactly what we do at Japonity. If you are exploring distribution, brand collaboration, or investment in the anime value chain, start a conversation with us at japonity.com/business-matching.

More from Japonity’s Japan Anime Business series

This article is part of a 10-piece editorial cluster on the business of Japanese anime. Read the rest:

- Inside Japan’s Anime Production Committee — How the money and rights really flow inside the joint-venture structure that funds almost every Japanese TV anime.

- Japan’s Anime Export Boom — Why overseas anime sales topped ¥1.7 trillion and overtook domestic for the first time in 2023.

- The 10 Anime Studios Behind 80% of Output — A ranked, opinionated business map of the studios that dominate foreign-licensed Japanese animation.

- Licensing Anime IP: A 2026 Foreign Buyer’s Guide — Why Western licensing instincts produce wrong answers in Japan, and the eight-stage flow that actually closes deals.

- Why Akihabara Still Matters — Behind the neon, Tokyo’s Akihabara is a working B2B test market for anime IP — a foreign buyer’s walking tour.

- VTuber Economics — Inside the billion-dollar virtual influencer industry built by Cover (Hololive) and ANYCOLOR (Nijisanji).

- The Anime Merchandise Pipeline — From Tokyo factories to Comic-Con booths — how an anime figure actually travels to a foreign retail shelf.

- Japan’s Trillion-Yen Manga Industry — Inside a publishing business larger than anime — and the four Tokyo houses every foreign publisher should know.

- A Day in the Life of an Anime Animator — Inside the working day of a rank-and-file animator, and the structural reasons wages stay low across the industry.

Sourcing beyond anime? Japonity also runs a Japan Sourcing Hub — a research-grade catalogue of 1,185 verified Japanese food products and 200+ overseas EC stores that already stock them, with HS codes, certifications and supplier MOQs ready for B2B procurement.

Interested in Japanese business opportunities?

Whether you're looking for technology partners, engineering talent, or market insights — we can help connect you with the right Japanese organizations.

Get in Touch →